💡 Takeaway:

Analysts systematically overestimate returns for stocks flagged as overvalued by anomalies—and underestimate anomaly-longs. Their return forecasts and recommendations often go in the opposite direction of anomaly signals.

Key Idea: What Is This Paper About?

The paper investigates how sell-side analyst recommendations and price targets align (or conflict) with cross-sectional anomaly signals. It finds that analyst actionables—return forecasts and ratings—tend to contradict anomalies. Analysts are too bullish on anomaly-shorts (overvalued stocks) and insufficiently positive on anomaly-longs (undervalued stocks), thereby contributing to market mispricing.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Analyst Incentives: Analysts may favor glamour stocks due to career concerns or investment banking ties.

- Behavioral Biases: Analysts may overreact to recent firm momentum or growth narratives.

- Slow Incorporation of Public Data: Analysts revise their targets slowly—even when anomalies provide early signals.

📌 Why It Matters:

If analyst forecasts misalign with anomaly-based signals, it opens a persistent opportunity for contrarian long-short strategies to exploit mispricing and inefficiencies.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Anomalies: 125 cross-sectional return anomalies (e.g., value, momentum, accruals)

- Analyst Data: IBES (1994–2017 for recs, 1999–2017 for targets)

- Sample Size: 670,000+ firm-months (forecasts), 930,000+ (recommendations)

- Return Forecasts: Based on 12-month median price targets

Model / Methodology

- Net Anomaly Score: Difference between # of long and short anomaly signals per stock

- Regression Tests: Return forecasts and recommendation levels regressed on Net score

- Forecast Errors: Measured as (Forecasted Return – Realized Return)

- Time Trend: Interaction of anomaly signals with time to assess learning/improvement

Trading Strategy (Derived from Results)

- Signal Generation:

- Long stocks with high Net (anomaly longs)

- Short stocks with low Net (anomaly shorts)

- Contrarian Filter: Fade analyst optimism when it's strongest for anomaly-shorts

- Time Horizon: 12-month holding, rebalance monthly

- Alpha Boost: Add anomaly-forecast disagreement filter to traditional anomaly trades

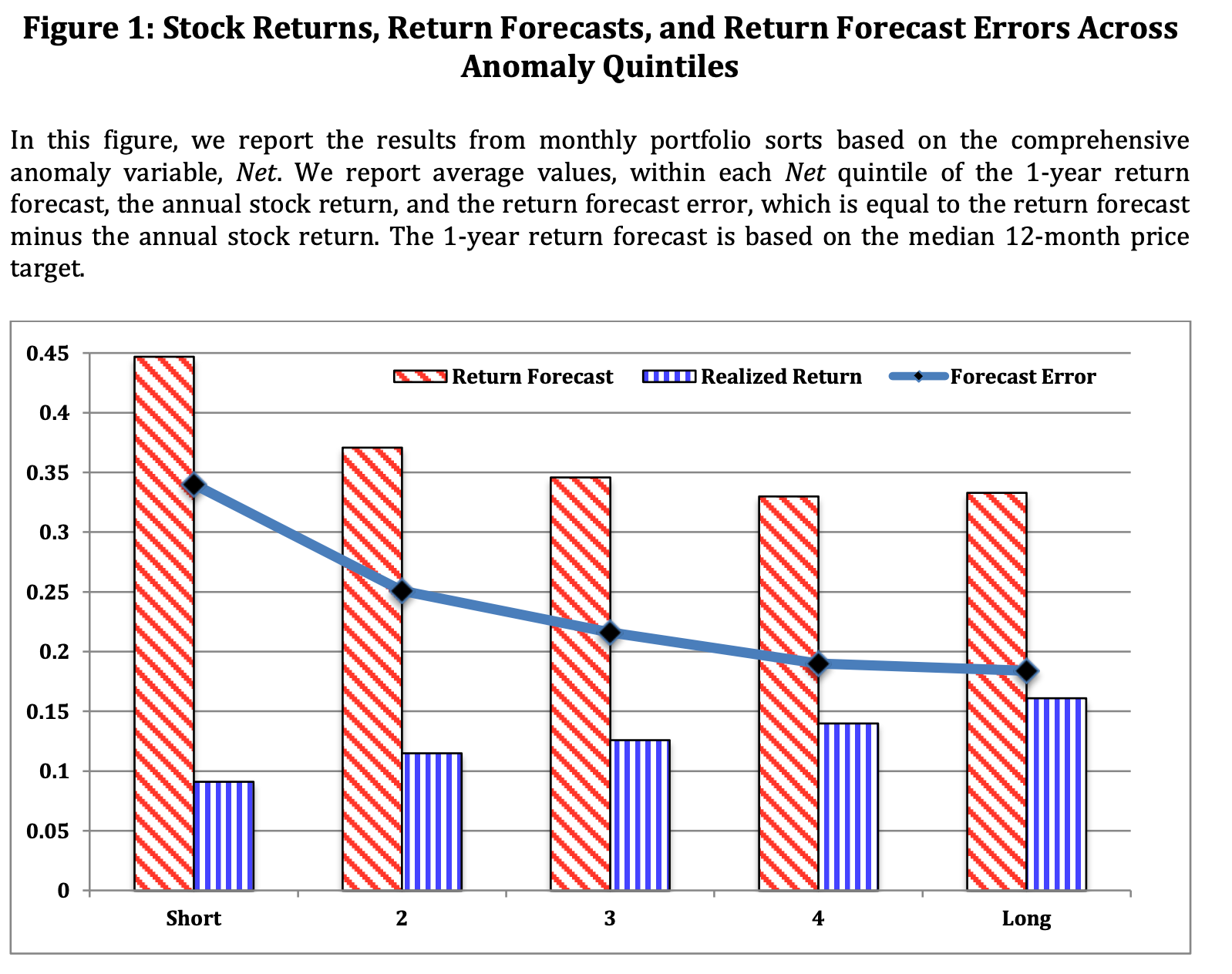

Key Table or Figure from the Paper

📌 Explanation:

- Forecasted returns are highest for stocks anomalies say to short.

- Actual returns are highest for stocks anomalies say to buy.

- Forecast error is twice as high for anomaly-shorts vs anomaly-longs.

- Confirms analysts consistently overestimate the wrong stocks.

Final Thought

💡 When analysts hype the wrong stocks, anomalies offer the better signal. 🚀

Paper Details (For Further Reading)

- Title: Analysts and Anomalies

- Authors: Joseph Engelberg, R. David McLean, Jeffrey Pontiff

- Publication Year: 2019

- Journal/Source: Forthcoming, Journal of Accounting and Economics

- Link: https://ssrn.com/abstract=2939174