💡 Takeaway:

Arbitrage capital erodes anomaly profits in the US. Outside the US, anomalies remain robust and profitable due to limits to arbitrage and market segmentation.

Key Idea: What Is This Paper About?

The paper studies 241 published anomalies across 39 countries. It shows that anomaly returns in the US decline sharply after publication, consistent with arbitrage trading. However, this pattern is not observed internationally—where anomalies persist. This suggests that most anomalies are due to mispricing, not data mining, and that global market segmentation shields these inefficiencies.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limits to Arbitrage: Higher costs, short-sale restrictions, and lower capital intensity outside the US reduce arbitrage.

- Market Segmentation: Regulatory, structural, and information barriers prevent anomaly exploitation in global markets.

- Behavioral Biases: Mispricing persists where arbitrage pressure is low—especially in illiquid and smaller stocks.

📌 Why It Matters:

Anomalies are real and often reflect inefficiencies—not statistical flukes. But their survival depends on arbitrage conditions and market access.

Data, Model, and Strategy Implementation

Data Used

- Period: 1980–2015

- Markets: 39 countries (including all MSCI developed/emerging markets)

- Anomalies: 241 (based on 161 peer-reviewed papers)

- Data Sources: CRSP (US), Datastream (global), Compustat & Worldscope (fundamentals), I/B/E/S (analyst forecasts)

Model / Methodology

- Define three return periods per anomaly:

- In-sample (pre-end of original study)

- Post-sample (after end of study, pre-publication)

- Post-publication (after journal release)

- Create monthly long-short portfolios (top vs bottom quintile)

- Compare alpha decay across countries and weighting schemes (equal vs value)

- Control for firm size, risk factors, time trends, and publication timing

Trading Strategy (Global Arbitrage Perspective)

- Pre-Publication (US and global): Traditional factor strategies work

- Post-Publication (US): Expect lower returns—focus on newer or less-known anomalies

- Post-Publication (Global):

- Exploit persistence in global anomalies

- Target markets with higher arbitrage barriers (e.g., short-sale constraints, low institutional ownership)

- Prefer small-cap, illiquid names where mispricing is harder to arbitrage

- Risk Management: Monitor anomaly decay by region and timing

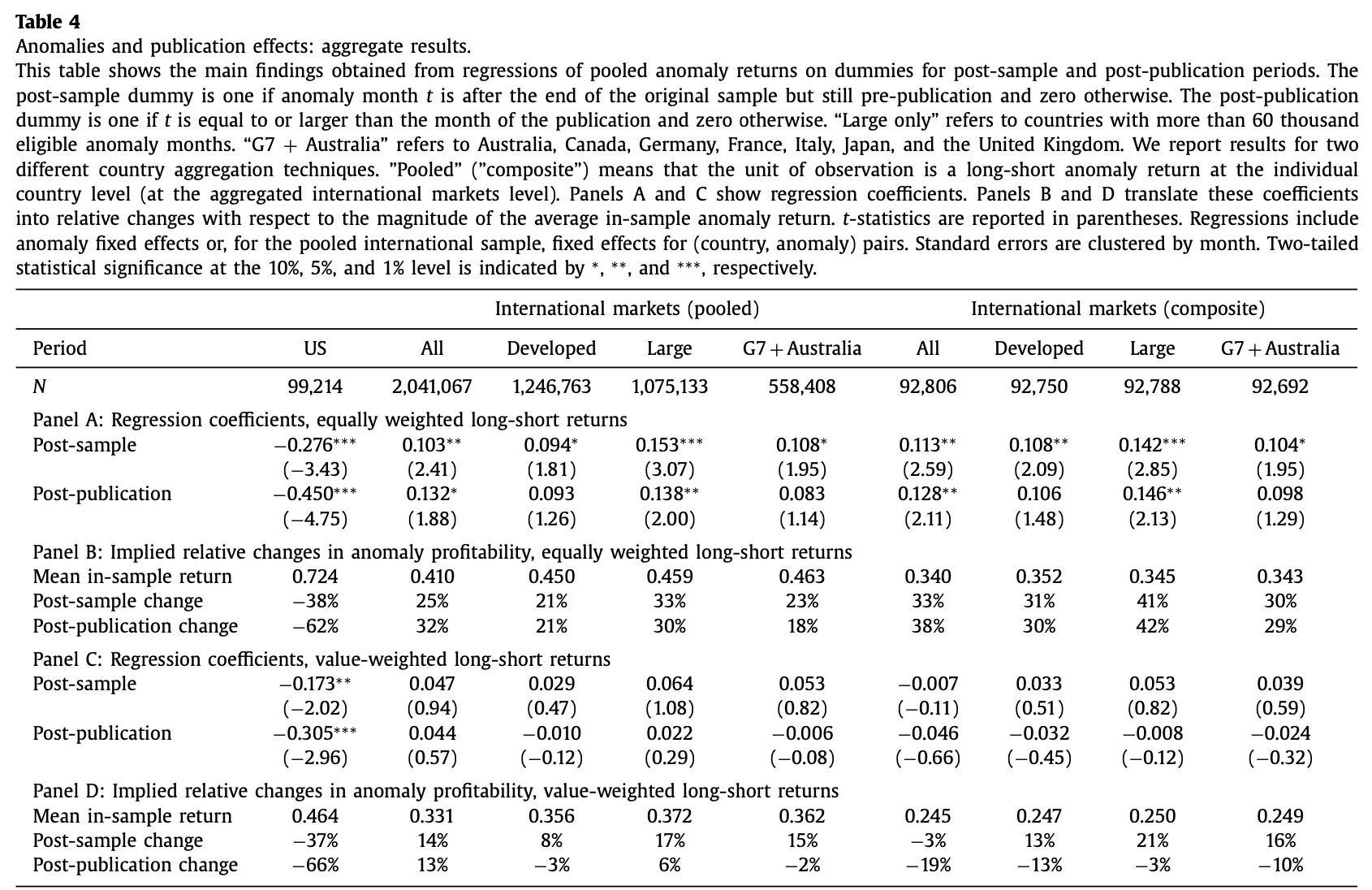

Key Table or Figure from the Paper

📌 Explanation:

- US anomaly returns drop by 62% (equal-weighted) and 66% (value-weighted) post-publication

- In contrast, anomalies in global markets show no consistent decline post-publication

- Strong alpha persistence in countries like Canada, Germany, UK, and Australia

- Evidence supports that mispricing, not p-hacking, drives many anomalies

Final Thought

💡 Anomalies die in the US—abroad, they live on. Arbitrage doesn’t cross borders easily.

🚀

Paper Details (For Further Reading)

- Title: Anomalies Across the Globe: Once Public, No Longer Existent?

- Authors: Heiko Jacobs, Sebastian Müller

- Publication Year: 2019

- Journal/Source: Journal of Financial Economics

- Link: https://doi.org/10.1016/j.jfineco.2019.06.004