📊 Performance

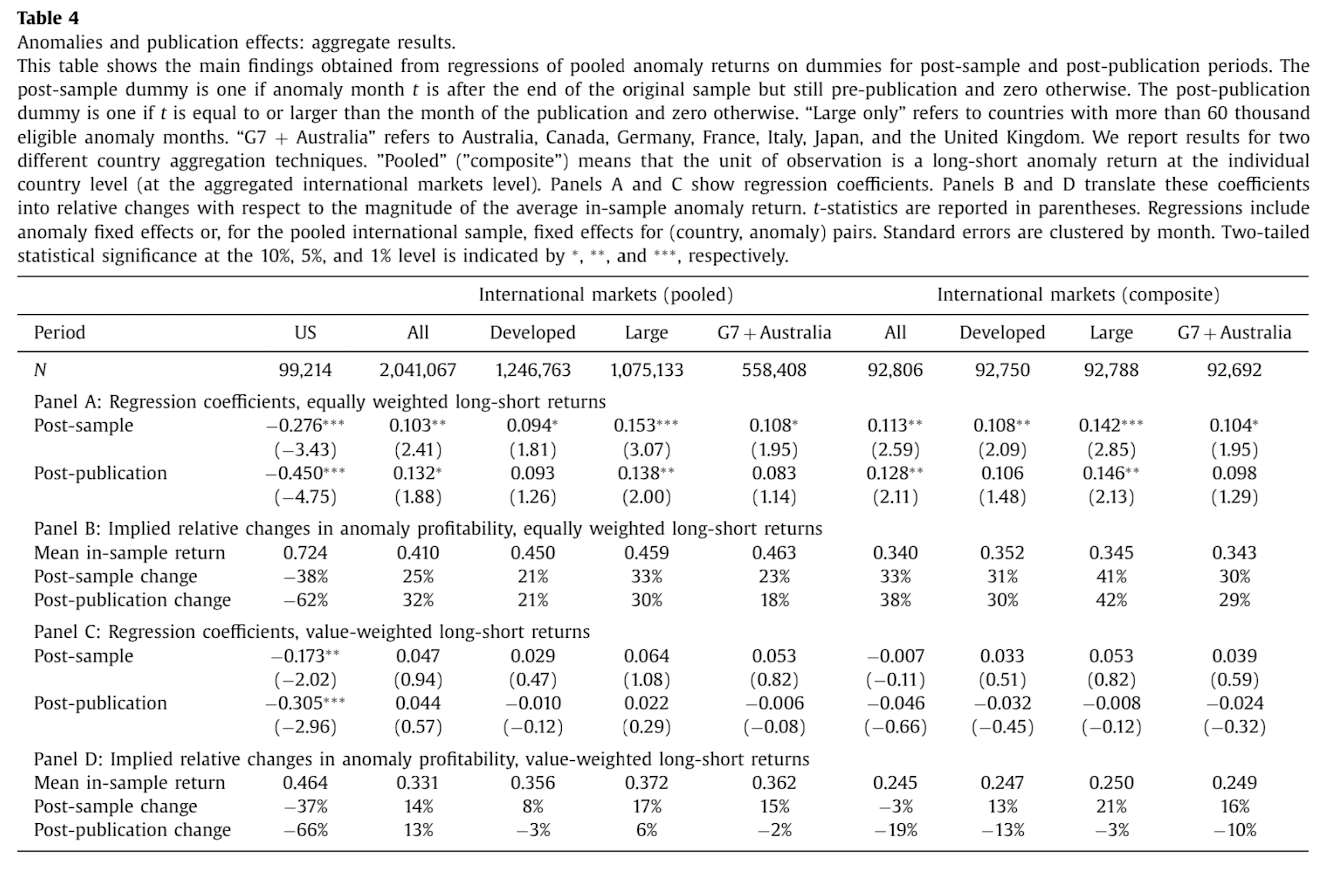

- US anomalies experience a 62% decline in profitability post-publication.

- Global anomalies do not show significant post-publication declines.

- In-sample returns are similar across developed markets, but post-publication declines occur only in the US.

💡 Key Idea

The paper analyzes 241 anomalies across 39 global stock markets and finds that only US anomalies significantly decline post-publication, suggesting arbitrageurs efficiently exploit mispricings in the US but face barriers elsewhere.

📖 Economic Rationale

- Efficient Markets Hypothesis (EMH): Once anomalies become public knowledge, rational arbitrageurs eliminate them through trading.

- Limits to Arbitrage: Institutional and regulatory barriers prevent global arbitrageurs from fully exploiting anomalies outside the US.

- Market Segmentation: Local constraints create fragmented markets where anomalies persist internationally.

⚡ Practical Applications

- Hedge funds & quant traders should focus on international anomalies, as they persist longer.

- Academic alpha strategies may degrade post-publication, requiring adaptation.

- Traders should consider market structure differences when designing global strategies.

🛠 How to Do It

🔢 Data

- CRSP (US) & Datastream (International) for stock market data.

- Compustat & Worldscope for accounting data.

- IBES for analyst forecasts.

📈 Model/Methodology

- Meta-analysis of 241 anomalies from peer-reviewed papers.

- Long-short portfolio construction: Top 20% (long) vs. bottom 20% (short).

- Comparison of in-sample, post-sample, and post-publication anomaly returns.

- Regression analysis: Tests whether anomalies decay after publication.

📊 Strategy

- Avoid US anomalies post-publication due to rapid arbitrage.

- Target international anomalies with limited arbitrage activity.

- Focus on anomalies in markets with high transaction costs & short-selling restrictions.

📌 Key Figure: Post-Publication Anomaly Decline

- Findings:

- The US market experiences a statistically significant 62% drop in long-short anomaly returns post-publication.

- No consistent post-publication decline is observed in international markets (G7 + Australia and pooled global markets).

- This suggests that arbitrageurs in the US rapidly eliminate anomalies, whereas international barriers prevent full arbitrage exploitation.

📄 Paper Details

Authors: Heiko Jacobs & Sebastian Müller

Journal: Journal of Financial Economics

Year: 2019

🔗 DOI: 10.1016/j.jfineco.2019.06.004