Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Anomaly returns:

- +50% on news days

- +6.3× higher on earnings days

- Forecast error predictability: Analysts too pessimistic (long) and too optimistic (short)

- Sharpe Improvement: Implied by concentrated anomaly alpha on news days

💡 Takeaway:

Anomaly profits spike when firm-specific news is released—suggesting they’re driven by mispricing corrected at information arrival, not risk or noise.

Key Idea: What Is This Paper About?

The paper investigates 97 known stock return anomalies and finds that their returns are significantly higher on days when firm-specific news (earnings or headlines) is released. This supports the idea that anomalies are driven by investor biases—since price corrections align with news timing. The authors rule out risk and data mining explanations through several robustness checks.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Biased Expectations: Investors over- or underreact to certain stock characteristics; anomalies reflect these biases.

- Price Correction via News: When firm-specific news arrives, prices adjust as investors revise beliefs.

- Limited Arbitrage: Small-cap stocks, with higher mispricing and higher frictions, show stronger effects.

📌 Why It Matters:

If anomalies are strongest when new info arrives, they likely stem from mistaken expectations—not risk premia. This supports behavioral finance over traditional asset pricing.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Anomalies: 97 strategies from McLean & Pontiff (2016)

- News: Dow Jones + WSJ headlines (1979–2013)

- Earnings: Compustat (adjusted to match timing via volume spikes)

- Returns & Fundamentals: CRSP, Compustat, IBES

Model / Methodology

- Define "Net" = number of long - short anomaly memberships

- Daily panel regressions: returns ~ Net × (Earnings Day / News Day)

- Control for market, volume, momentum, and macro announcements

- Use analyst forecast errors to test for belief biases

Trading Strategy (Conceptual Guidance)

- Signal: Go long (short) high (low) Net stocks on news/earnings days

- Execution: Monthly rebalanced long-short portfolio

- Enhancement: Tilt more aggressively around scheduled firm events (earnings), especially in small-cap stocks

- Risk Management: Anomaly effects are more persistent on event days than off-event

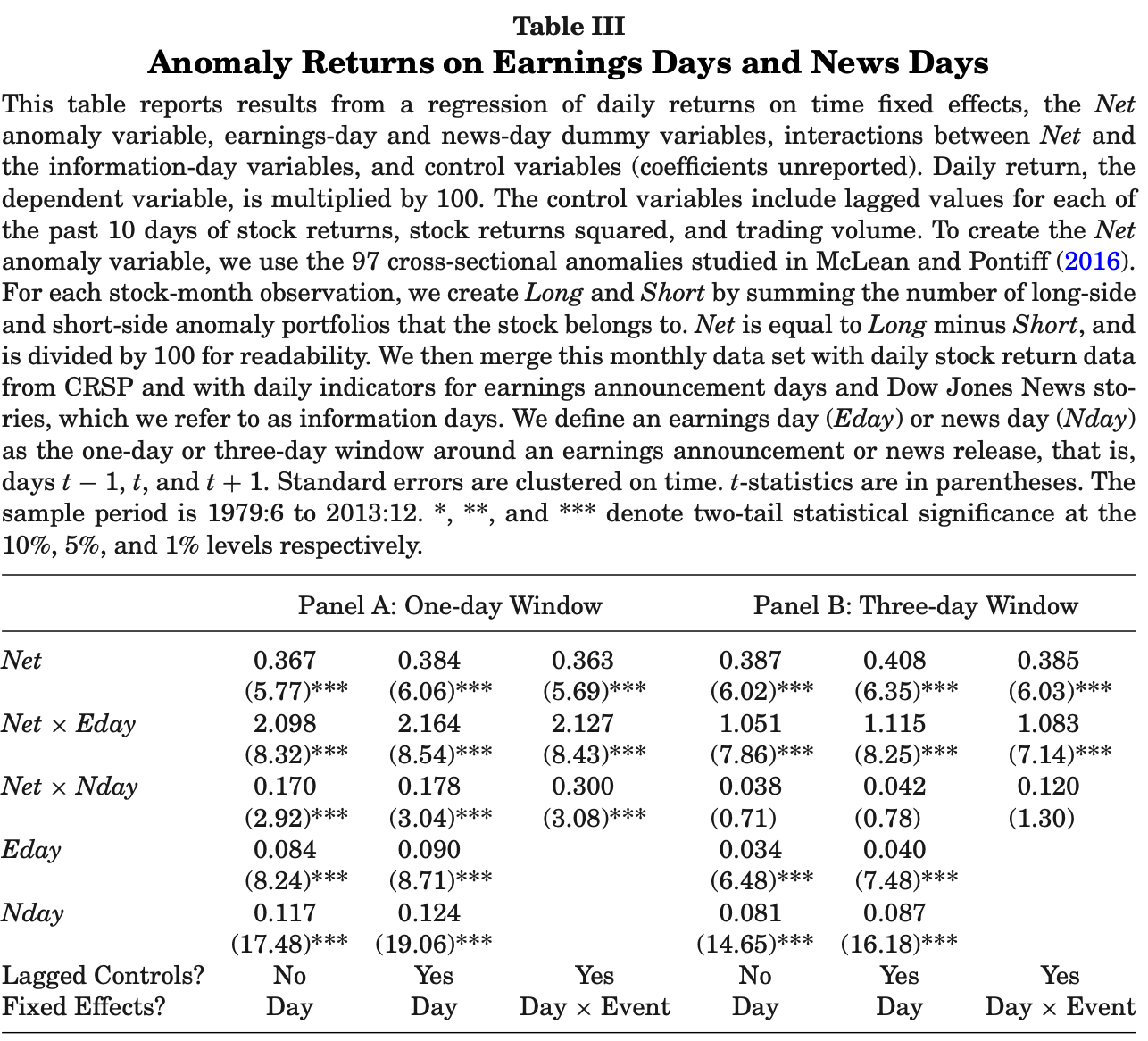

Key Table or Figure from the Paper

📌 Explanation:

- Net × Earnings: Coefficient = 2.164 → 6.3× higher anomaly return vs normal days

- Net × News: Coefficient = 0.178 → ~50% boost on regular news days

- Shows anomaly alpha concentrates on event days—supporting a mispricing correction hypothesis

Final Thought

💡 Anomalies aren't always working—just when the truth shows up. 🚀

Paper Details (For Further Reading)

- Title: Anomalies and News

- Authors: Joseph Engelberg, R. David McLean, Jeffrey Pontiff

- Publication Year: 2018

- Journal/Source: The Journal of Finance

- Link: https://doi.org/10.1111/jofi.12718