💡 Takeaway:

Once an anomaly is widely known, hedge funds exploit it—lowering returns, changing correlations, and increasing turnover in both long and short legs.

Key Idea: What Is This Paper About?

The paper builds a model to analyze how arbitrageurs respond to new anomaly discoveries. Once an anomaly is published, hedge funds trade to exploit it. This reduces returns, increases correlation with other anomalies (via wealth effects), and reduces correlation between the long and short sides of the anomaly. These effects also generate diversification gains for passive investors.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Wealth-Driven Arbitrage: Arbitrageurs reallocate capital after positive shocks, raising prices of longs and dropping shorts.

- Limits to Arbitrage: Arbitrageurs only respond once a discovery is credible/public (e.g., post-publication).

- Risk vs Mispricing: Both types of anomalies (risk-based or behavioral) show the same post-discovery behavior.

- Diversification Externality: Arbitrage changes intra-portfolio correlations, unintentionally benefiting market-wide portfolios.

📌 Why It Matters:

Alpha is fragile. Once known, anomalies are absorbed by sophisticated capital and decay—so performance depends on your timing.

Data, Model, and Strategy Implementation

Data Used

- Anomalies: 99 well-known anomalies from CRSP/Compustat/IBES

- Returns: Decile portfolios for each anomaly (D1–D10)

- Discovery Proxy: Paper publication date (or working paper if unpublished)

- Trading Data: 13F hedge fund holdings, short interest (post-2000)

- Period: 1963–2015 (returns), 1986–2015 (hedge fund AUM)

Model / Methodology

- Compare "pre" and "post" discovery using rolling 5-year windows

- Track changes in:

- Long-short anomaly return

- Correlation (D1 vs D10)

- Excess volatility of D1+D10 over market

- Test interaction with hedge fund AUM volatility

- Use citation-weighted regressions to proxy anomaly “attention”

Trading Strategy (Implications, not directly prescribed)

- Before Discovery: Traditional anomaly trading may yield higher alpha

- After Discovery:

- Expect lower returns

- Use anomaly correlation change as signal of arbitrage crowding

- Monitor hedge fund AUM and flows as potential timing input

- Exploit turnover/friction in short legs more carefully

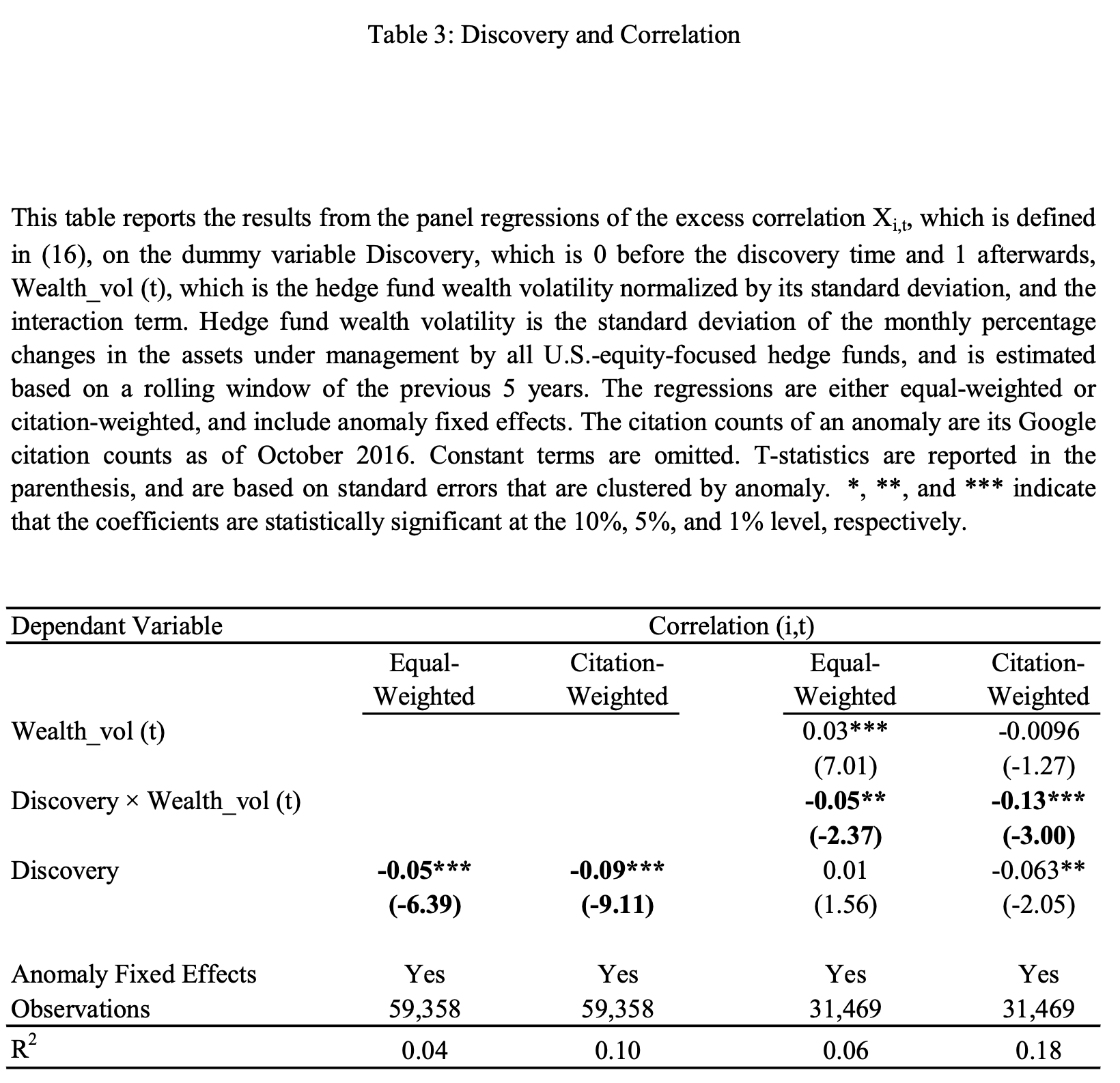

Key Table or Figure from the Paper

📌 Explanation:

- Post-discovery, correlation between long and short legs drops by 5% (equal-weighted), and 9% (citation-weighted).

- Stronger effect when hedge fund wealth volatility is high

- Reflects arbitrageurs dynamically reallocating capital across anomalies

Final Thought

💡 Alpha dies not with a crash—but with discovery and arbitrage. 🚀

Paper Details (For Further Reading)

- Title: Anomaly Discovery and Arbitrage Trading

- Authors: Xi Dong, Qi Liu, Lei Lu, Bo Sun, Hongjun Yan

- Publication Year: 2018

- Journal/Source: Working Paper

- Link: https://sites.google.com/site/hongjunyanhomepage/