Performance

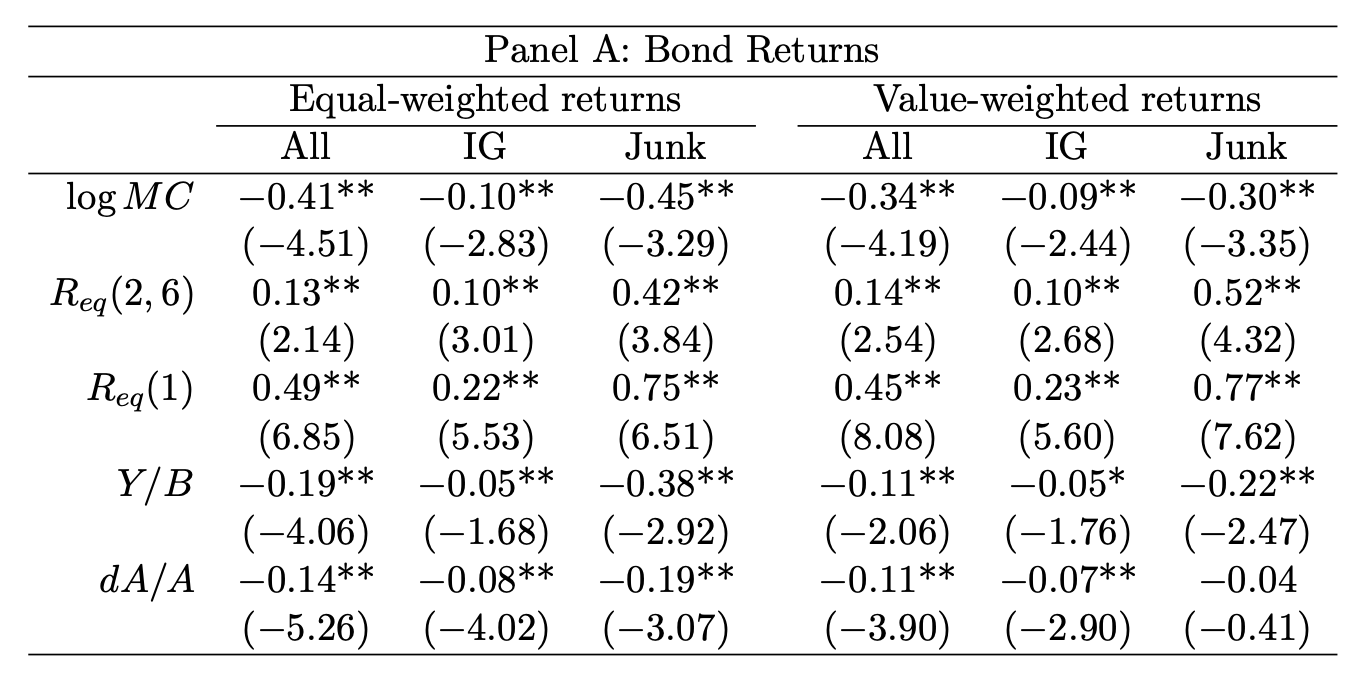

- Equity return predictors such as market capitalization, profitability, and asset growth significantly forecast corporate bond returns.

- Momentum and size factors show stronger predictability in junk bonds than investment-grade bonds.

- The lead-lag effect from equity to bond markets is significant, with one-month lagged stock returns predicting bond returns.

Key Idea

This paper explores whether equity market anomalies translate to corporate bond returns and finds commonalities, particularly in size, profitability, asset growth, and momentum. Bonds tend to be efficiently priced within transaction cost bounds, and equity returns provide leading signals for bond returns.

Economic Rationale

- Risk-Based Explanation: Firms with higher asset growth and profitability are seen as less risky, leading to lower bond returns.

- Stock Market Leadership: Stocks aggregate information faster than bonds, leading to a predictive relationship.

- Institutional Efficiency: Corporate bonds are mostly held by institutions, making them less prone to behavioral biases than equities.

Practical Applications

- Cross-Asset Trading Strategies: Use lagged stock returns to predict bond movements.

- Credit Market Insights: Bond traders can leverage equity signals for risk assessment.

- Factor Investing in Bonds: Adapt traditional equity factor models for bond markets.

How to Do It

Data

- Corporate bond returns from Lehman Brothers Fixed Income Database, TRACE, Mergent FISD, and Datastream (1973-2014).

- Equity return predictors from CRSP and Compustat.

Model/Methodology

- Fama-MacBeth regressions to assess the impact of equity anomalies on bond returns.

- Long-short portfolio analysis using factor-based sorting.

- Transaction cost adjustments to test for arbitrage opportunities.

Strategy

- Momentum Effect: Go long on bonds of firms with high past equity returns and short on bonds of firms with low past equity returns.

- Size Factor: Short large-cap firms' bonds and long small-cap firms' bonds.

- Profitability & Asset Growth: Avoid bonds from high-profitability, high-growth firms, as they offer lower returns.

Table or Figure

(Table 7 from the paper ): Long-short portfolio returns sorted by equity return predictors.

- Momentum (5-month lagged stock returns) yields significant bond return predictability.

- Size and profitability have opposite signs for equities and bonds, highlighting risk-based pricing.

Paper Details

- Authors: Tarun Chordia, Amit Goyal, Yoshio Nozawa, Avanidhar Subrahmanyam, Qing Tong

- Published: May 2016

- Source: Working paper, various academic institutions