💡 Takeaway:

Underreaction-related anomalies earn higher alpha among low media coverage stocks, especially from the overpriced short side. Media attention suppresses anomaly returns by reducing mispricing.

Key Idea: What Is This Paper About?

This study explores why many prominent return anomalies (e.g., momentum, ROE, earnings surprises) are stronger among firms with low media coverage. Using media attention as a proxy for investor awareness, the authors show that limited attention leads to underreaction, and that short-sale constraints prevent arbitrage correction—especially for overpriced stocks. This drives stronger anomaly returns among “ignored” firms.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limited Attention: Investors don’t fully process firm-specific news for less-covered firms.

- Underreaction: Price adjustments to good/bad news are slow, creating predictable returns.

- Limits to Arbitrage: Short-sale constraints prevent correcting overpricing on the short side.

- Behavioral Biases: Inattention leads to expectation errors by both investors and analysts.

📌 Why It Matters:

Many anomalies are more profitable because they exploit systematic expectation errors. When attention is low, mispricing lasts longer, especially among hard-to-arbitrage stocks.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Time Period: 2000–2018

- Assets: US equities (CRSP + Compustat + RavenPack)

- Attention Proxy: Monthly Dow Jones news count (log-transformed)

- Anomalies Studied:

- PEAD, MOM, ROE, PERF, PMU, RMW

- Additional: SUE, RE, IndMom, ROA, NEI, FP, OS

Model / Methodology

- Double Sorts: Stocks grouped by media coverage and anomaly signal

- Fama-MacBeth Regressions: Control for firm size, beta, liquidity, ownership, and interaction terms

- Event Study: Earnings announcement surprise differences (CAR and SUE) across coverage levels

- Arbitrage Cost Proxies: Idiosyncratic volatility, illiquidity, institutional ownership, bid-ask spreads

Trading Strategy (Based on Results)

- Signal: Focus on underreaction anomalies in low media coverage stocks

- Execution:

- Long: Undervalued firms with strong fundamentals or momentum

- Short: Overvalued firms with bad signals and low coverage

- Enhancement:

- Filter stocks with high arbitrage cost (illiquidity, high idio-vol, low institutional ownership)

- Rebalance monthly; earnings announcement periods are key windows

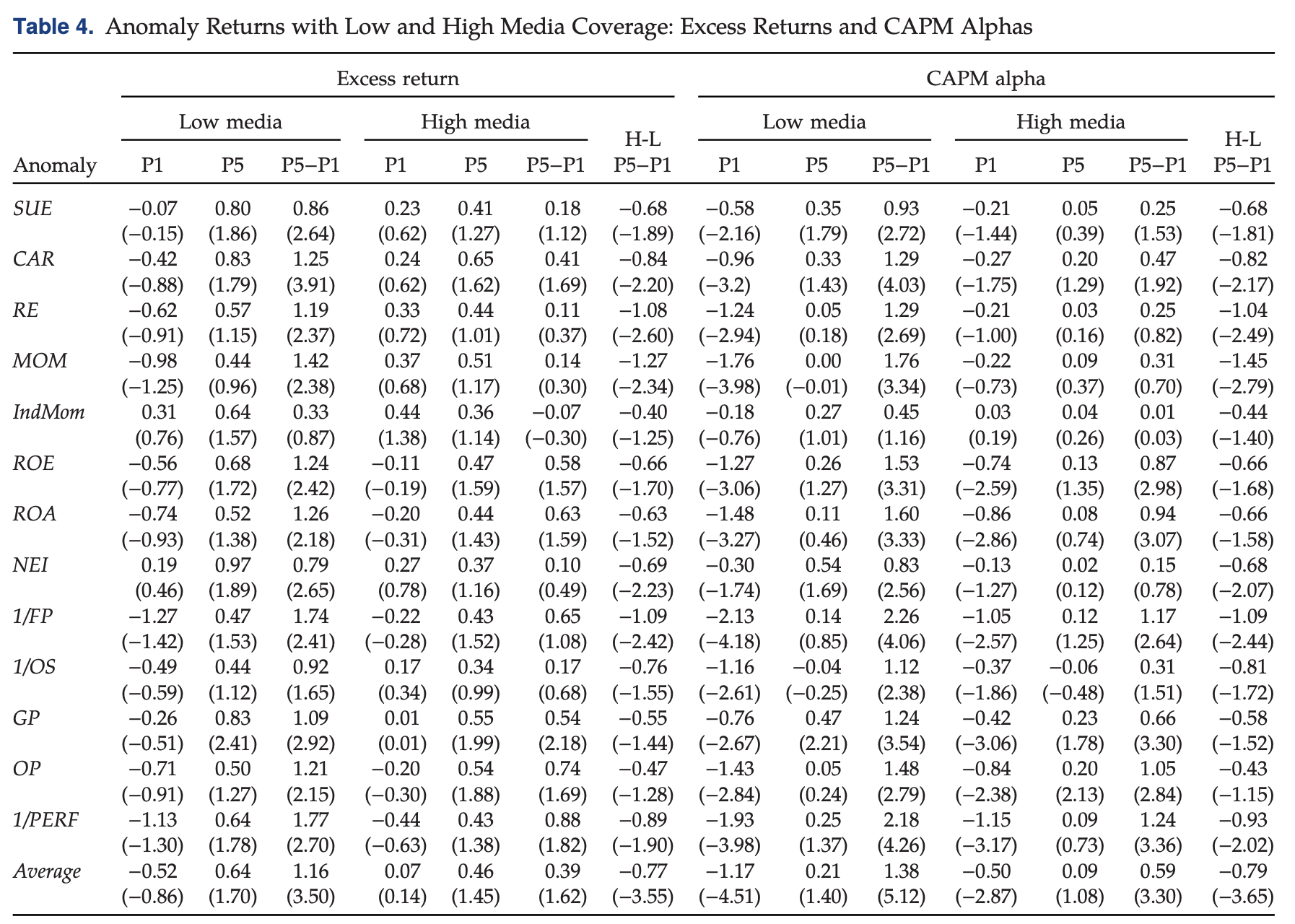

Key Table or Figure from the Paper

📌 Explanation:

- FF5 Alpha spread: 0.97%/month for low media firms vs 0.24% for high media

- Most alpha comes from short leg of anomalies (e.g., −1.21%)

- Confirms investor inattention drives underreaction, and media attention moderates it

Final Thought

💡 Anomalies aren’t dead—they’re just hiding where no one’s paying attention. 🚀

Paper Details (For Further Reading)

- Title: Attention and Underreaction-Related Anomalies

- Authors: Xin Chen, Wei He, Libin Tao, Jianfeng Yu

- Publication Year: 2023

- Journal/Source: Management Science

- Link: https://doi.org/10.1287/mnsc.2022.4332