Performance

- Basis-momentum is the strongest predictor of commodity returns, outperforming traditional factors like basis and momentum.

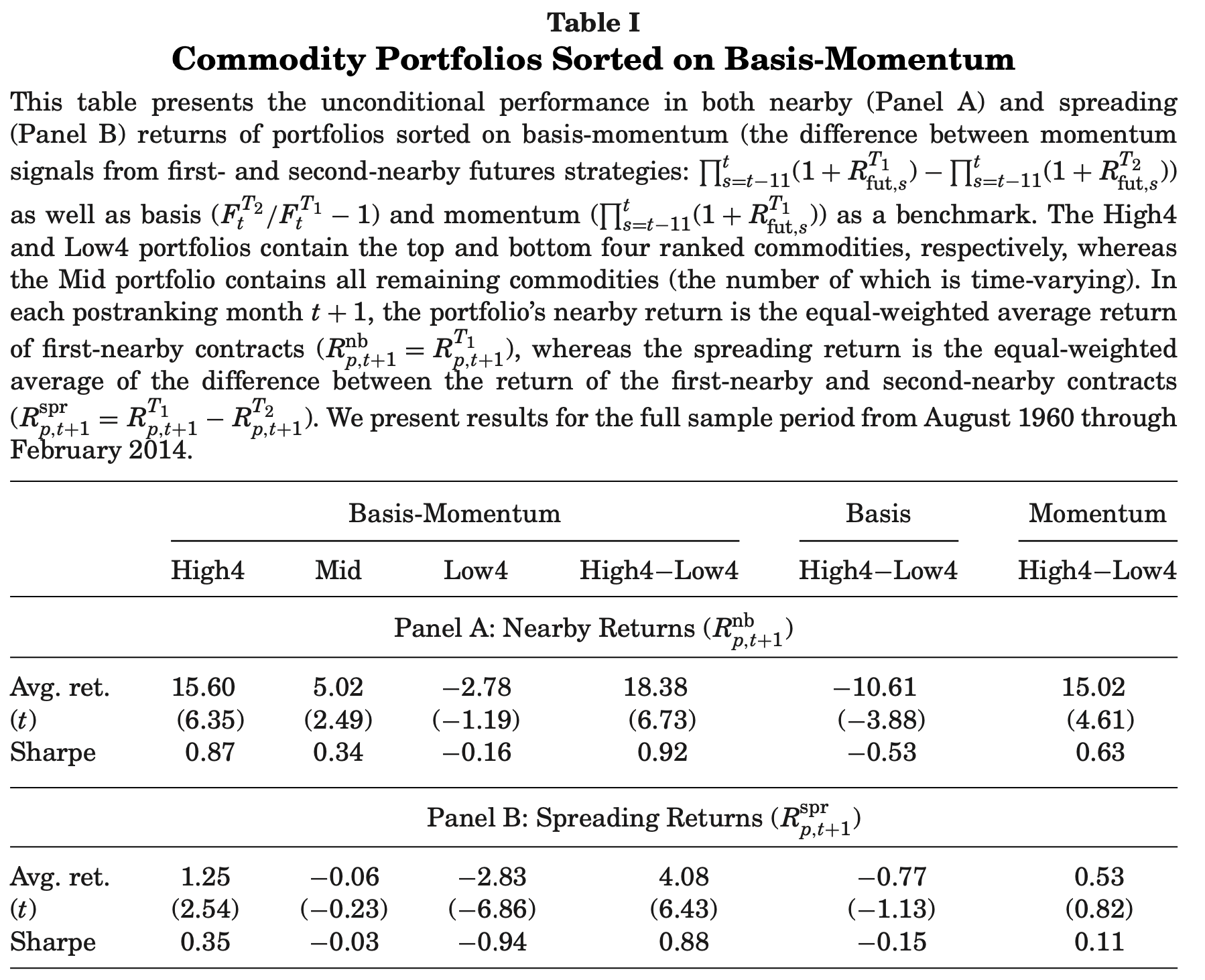

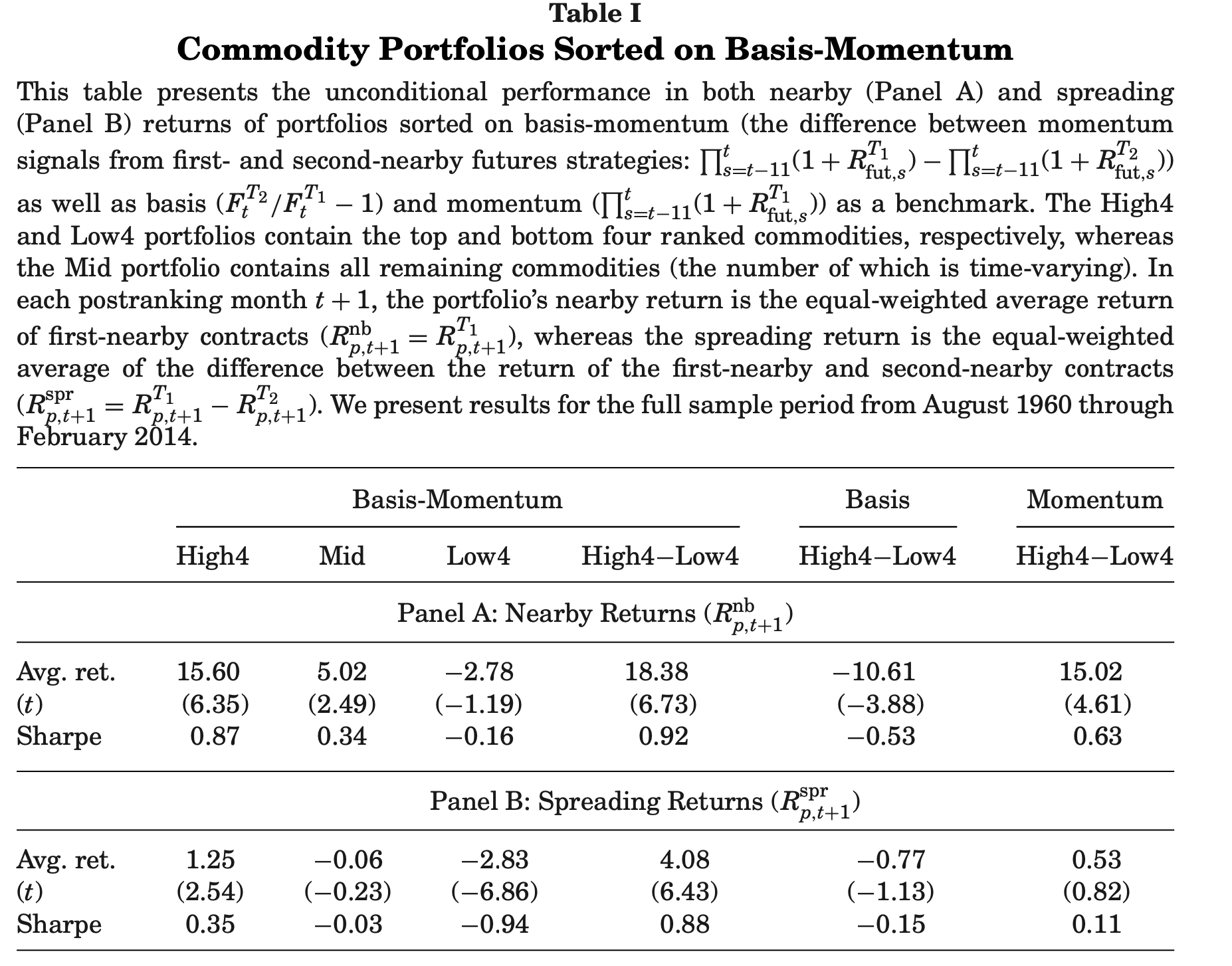

- A long-short strategy based on basis-momentum earns an 18.38% annualized return with a Sharpe ratio of 0.9.

- The strategy captures both spot and term premiums, making it effective across different contract maturities.

- Returns are higher in times of market stress, suggesting it benefits from liquidity provision and volatility risk premia.

Key Idea

This paper introduces basis-momentum, a predictor based on the slope and curvature of the futures curve. It explains commodity returns better than traditional basis and momentum signals. The strategy exploits changes in futures curves caused by speculator positioning and liquidity constraints, which impact commodity pricing dynamics.

Economic Rationale

- Market Imbalances: Basis-momentum arises when speculators and intermediaries struggle to clear the market, leading to return predictability.

- Liquidity & Volatility Effects: Returns are higher when volatility spikes, supporting the idea that basis-momentum compensates for liquidity provision risks.

- Beyond Storage & Hedging: Unlike traditional commodity pricing models (e.g., storage and hedging pressure), basis-momentum also predicts returns in financial assets like currencies, stocks, and bonds, suggesting a broader risk premium effect.

Understanding the Futures Curve

The futures curve represents the prices of a commodity's futures contracts over different expiration dates. It can have different shapes:

- Contango (upward slope): Farther-out contracts are more expensive than near-term contracts.

- Backwardation (downward slope): Farther-out contracts are cheaper than near-term contracts.

Step 1: Define the Key Components

- Momentum (M) – Measures the past performance (returns) of a futures contract over the last 12 months.

- Basis (B) – Measures the difference between the futures price and the spot price (or between two futures contracts with different maturities).

- Curvature – Measures the steepness of the futures curve at different points.

Step 2: Compute Basis-Momentum

Basis-Momentum (BM) is calculated by comparing momentum at different points on the futures curve:

Basis-Momentum formula:

$$ BM_t = M_t^{\text{nearby}} - M_t^{\text{second-nearby}} $$

Where:

- ( M_t^{\text{nearby}} ) = Momentum of the first-nearby futures contract (closest to expiration).

- ( M_t^{\text{second-nearby}} ) = Momentum of the second-nearby futures contract (next closest to expiration).

Alternative Formulation Using Log Returns

The formula can also be expressed using log returns:

Alternative Basis-Momentum formula:

$$ BM_t = \sum_{s=t-11}^{t} r_s^{\text{nearby}} - \sum_{s=t-11}^{t} r_s^{\text{second-nearby}} $$

where ( r_s ) represents the return of the contract at time ( s ).

Step 3: Interpretation

- High Basis-Momentum → The near-term contract is gaining more momentum than the second-nearby contract.

- Signal: Prices are rising quickly, suggesting strong short-term demand.

- Trading strategy: Go long (buy) high basis-momentum commodities.

- Low Basis-Momentum → The near-term contract has lower momentum than the second-nearby contract.

- Signal: Prices are stagnating or falling, indicating weaker demand.

- Trading strategy: Go short (sell) low basis-momentum commodities.

Why It Works?

- Market Imbalances: Basis-momentum captures supply-demand imbalances that traditional indicators miss.

- Liquidity & Volatility: Returns on basis-momentum tend to increase when markets are volatile, benefiting from speculator activity.

- Beyond Commodities: The concept applies to currencies, stocks, and bonds, showing it captures a broad risk premium effect.

Practical Applications

- Basis-Momentum Strategy: Go long commodities with high basis-momentum and short those with low basis-momentum.

- Volatility-Timed Trading: Increase exposure during high-volatility periods, as basis-momentum returns rise when markets are stressed.

- Cross-Asset Trading: Apply the concept to currencies, stock indices, and bonds, where similar momentum patterns exist.

- Sector-Based Allocation: Since sectoral commonality doesn’t explain basis-momentum, traders can diversify across commodities without losing the effect.

How to Do It

Data

- Commodity futures price data from 1959-2014 (21-32 commodities).

- Futures curve characteristics: Slope, curvature, and momentum differences between first and second-nearby contracts.

- Trader positioning data: Speculator and hedger positions from CFTC Commitment of Traders (COT) reports.

Model/Methodology

- Sorting-based long-short portfolios: Top 4 vs. bottom 4 basis-momentum commodities.

- Regression-based return prediction: Testing basis-momentum against traditional basis and momentum factors.

- Factor modeling: Basis-momentum tested in asset pricing models alongside risk premia factors.

- Robustness tests: Results hold across different time periods, commodity sectors, and trader positioning regimes.

Strategy

- Momentum-Based Trading: Buy commodities where basis-momentum is high and short those where it’s low.

- Market-Stress Advantage: Increase exposure when volatility spikes, as returns on basis-momentum tend to rise.

- Multi-Maturity Arbitrage: Exploit spreads between nearby and farther-out contracts using the basis-momentum signal.

- Cross-Asset Adaptation: Apply to currencies, bonds, and stock indices, as the effect is not limited to commodities.

Table or Figure

- Annualized return of 18.38% with a Sharpe ratio of 0.9.

- Outperforms traditional basis and momentum factors in predicting both nearby and spreading returns.

- Robust across time periods and different commodity types.

Paper Details

- Authors: Martijn Boons & Melissa Porras Prado

- Published: 2019

- Source: Journal of Finance

- DOI: 10.1111/jofi.12738