Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

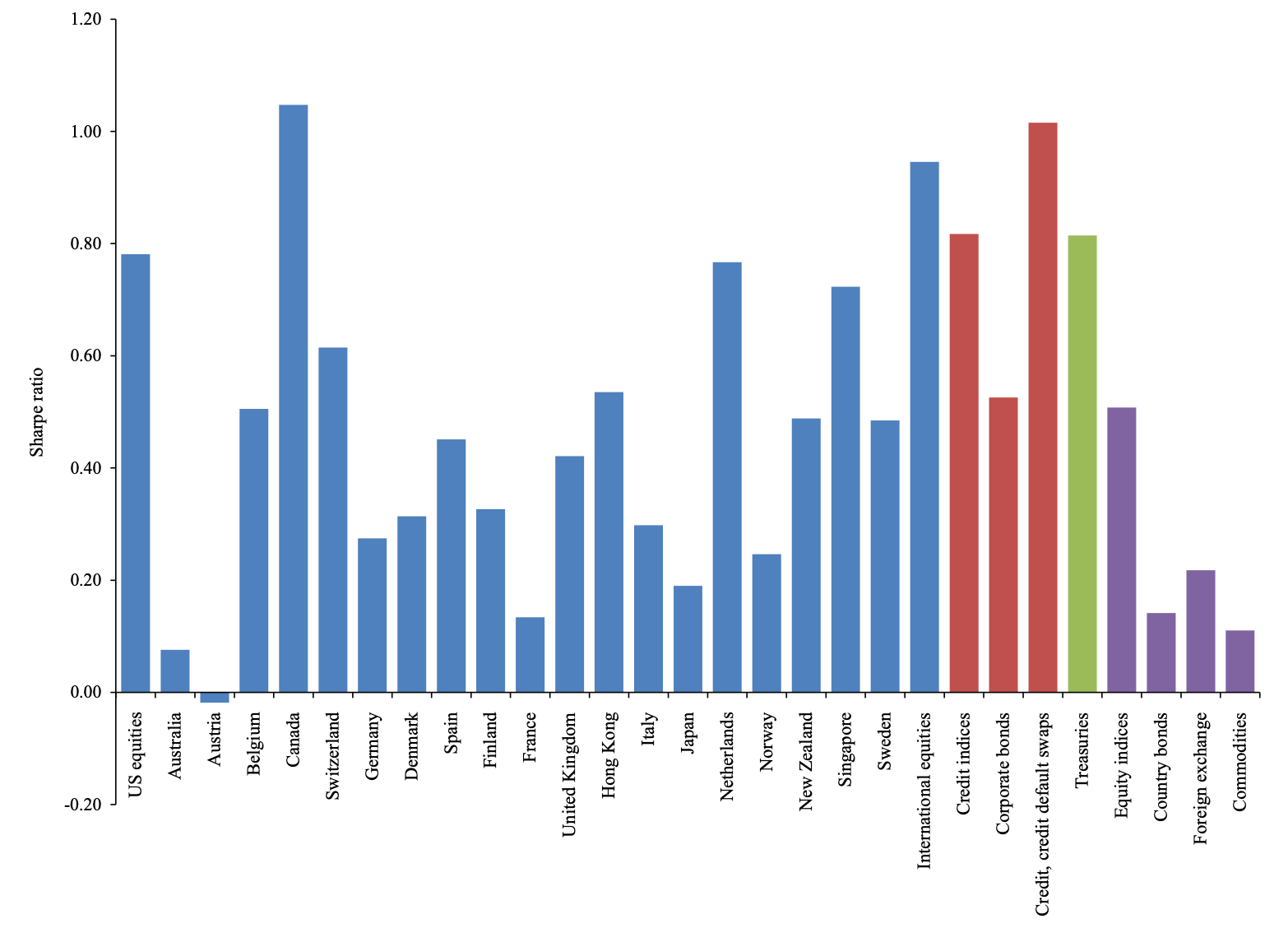

- US Stocks Sharpe Ratio (BAB Factor): 0.78

- Treasury BAB Sharpe Ratio: 0.81

- Corporate Credit BAB Sharpe Ratio: 0.82

- Alpha: Significant in 18 of 19 developed equity markets

💡 Takeaway:

Betting against beta delivers strong, positive, and consistent returns across time, countries, and asset classes—outperforming traditional equity factors like value and momentum.

Key Idea: What Is This Paper About?

The paper explains why low-beta assets outperform on a risk-adjusted basis. Investors who can’t use leverage are forced to chase high-beta assets for higher expected returns, pushing their prices up and expected returns down. In contrast, low-beta assets are underpriced. A market-neutral portfolio that goes long low-beta assets (leveraged) and shorts high-beta assets earns high returns.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Leverage Constraints: Investors unable to borrow overweight risky (high-beta) assets instead of leveraging safer ones.

- Flattened Security Market Line: When many agents are constrained, the CAPM becomes too flat—high-beta assets have lower alpha.

- Funding Liquidity Risk: When liquidity tightens, the BAB strategy suffers short-term losses but earns higher returns afterward.

- Market Clearing Mechanism: Unconstrained investors arbitrage by leveraging low-beta assets and shorting overpriced high-beta ones.

📌 Why It Matters:

It challenges the classic CAPM and redefines the role of leverage and risk-taking in asset pricing. The results reshape portfolio construction and performance attribution.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Asset Classes: US & international equities, Treasuries, corporate bonds, credit indices, FX, commodities

- Period: US equities from 1926, global from 1980s, others vary (1950s–2012)

- Sources: CRSP, MSCI, Xpressfeed, Barclays Bond Hub, AQR internal data

Model / Methodology

- Key Model Feature: Multiple investor types with different leverage constraints and risk aversion

- BAB Construction:

- Sort assets by beta

- Go long low-beta assets (leveraged to beta=1)

- Short high-beta assets (de-leveraged to beta=1)

- Result: Market-neutral portfolio capturing the beta anomaly

Trading Strategy (BAB Factor)

- Signal Generation: Use historical rolling beta to sort assets

- Portfolio Construction:

- Long side: leverage low-beta assets

- Short side: de-leverage high-beta assets

- Rebalancing: Monthly

- Risk Targeting: Equal beta exposure long and short, volatility-scaled

Key Table or Figure from the Paper

📌 Explanation:

- Plots annualized Sharpe ratios of BAB strategies across stocks, bonds, credit, FX, and commodities

- Almost all asset classes show positive Sharpe ratios, with US stocks and Treasuries exceeding 0.80

- Highlights the consistency and robustness of the BAB effect across global markets and asset types

Final Thought

💡 You don’t need to take more risk to earn more—you just need to bet against beta. 🚀

Paper Details (For Further Reading)

- Title: Betting Against Beta

- Authors: Andrea Frazzini, Lasse Heje Pedersen

- Publication Year: 2014

- Journal/Source: Journal of Financial Economics

- Link: https://doi.org/10.1016/j.jfineco.2013.10.005