Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Annual Sharpe Ratio (Bitcoin): 2.30

- Annual Return (Bitcoin): 404.9%

- Volatility (Bitcoin): 176.1%

💡 Takeaway:

Bitcoin had explosive historical returns and very low correlation with other asset classes. Adding just 3–6% Bitcoin improved Sharpe and Sortino ratios significantly—though it worsened tail risk.

Key Idea: What Is This Paper About?

Using data from 2010–2013, the paper tests whether Bitcoin improves portfolio performance. Despite its extreme volatility, Bitcoin’s low correlation with both traditional and alternative assets yields significant diversification benefits. Even small allocations enhance risk-adjusted returns.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Modern Portfolio Theory (MPT): Assets with low correlation improve the efficient frontier.

- Crisis Hedging & Positive Skew: Bitcoin’s positively skewed returns and low co-movement with global assets give it hedge-like characteristics.

- Inflation Hedge Narrative: Like gold, Bitcoin’s fixed supply can attract investors during macro stress.

📌 Why It Matters:

Bitcoin may offer return drivers distinct from traditional risk premia. This challenges the idea that crypto is only speculative and opens the door to crypto inclusion in strategic asset allocation.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Source: BitcoinCharts (BTC/USD), Datastream (asset indices)

- Period: 23 July 2010 – 27 December 2013

- Assets Covered: BTC, stocks (dev/emg), bonds (gov/corp/infl), commodities (gold, oil), hedge funds, real estate

Model / Methodology

- Descriptive Stats: Volatility, Sharpe, Sortino, skew, kurtosis

- Spanning Tests: Huberman-Kandel (1987), Ferson et al. (1993)

- Efficient Frontier Analysis: Compared BTC-included vs BTC-excluded portfolios

- Portfolio Optimization: Volatility targets at 6% and 12%

Trading Strategy (Derived from Findings)

- Signal Generation: Not based on alpha signals, but portfolio construction logic

- Implementation Ideas:

- Add 1–5% BTC to multi-asset portfolios

- Rebalance quarterly

- Use BTC ETFs or custodial products to reduce operational risk

- Risk Management: Adjust for tail risk using downside measures or capped exposure

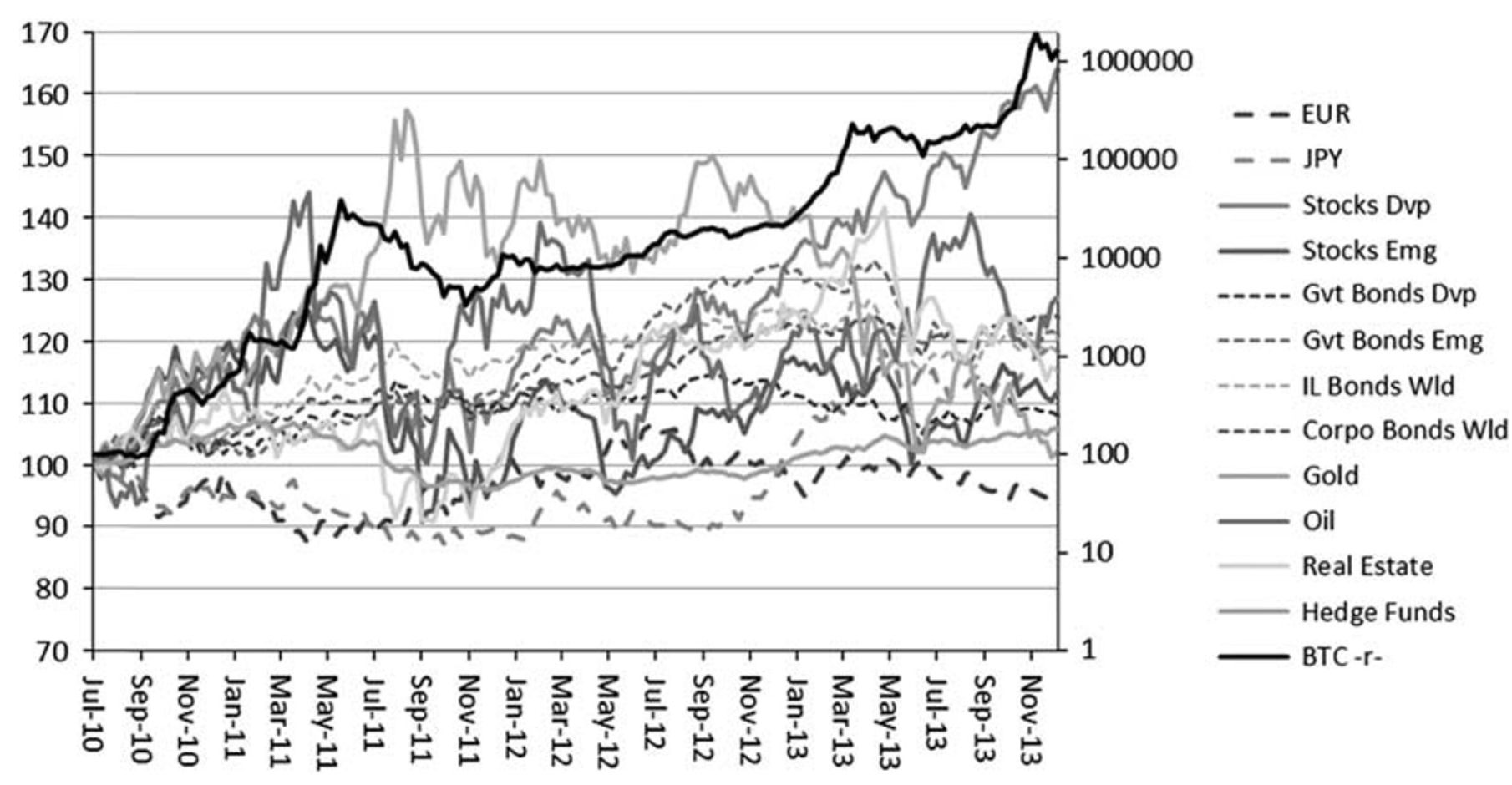

Key Table or Figure from the Paper

📌 Explanation:

- The figure compares cumulative performance (in USD) of Bitcoin against 12 other traditional and alternative assets from July 2010 to December 2013.

- Bitcoin's line (right axis, logarithmic scale) clearly stands out, showing explosive growth compared to all other assets (left axis).

- While traditional assets like stocks, bonds, gold, and real estate moved gradually, BTC surged exponentially—despite multiple crashes—highlighting its extreme return potential and volatility.

- This visual sets the stage for Bitcoin’s role as a high-return, uncorrelated asset that can impact a portfolio's overall performance even with a small allocation.

Final Thought

💡 Bitcoin’s volatility is its curse—but also its greatest gift to portfolio diversification. 🚀

Paper Details (For Further Reading)

- Title: Virtual currency, tangible return: Portfolio diversification with bitcoin

- Authors: Marie Brière, Kim Oosterlinck, Ariane Szafarz

- Publication Year: 2015

- Journal/Source: Journal of Asset Management

- Link: https://doi.org/10.1057/jam.2015.5