💡 Takeaway:

Macroeconomic uncertainty is a priced risk factor in the corporate bond market. Bonds that lose value when uncertainty spikes carry higher future returns.

Key Idea: What Is This Paper About?

The paper investigates how bonds respond to changes in macroeconomic uncertainty. It defines a bond-level beta to economic uncertainty (βUNC) and shows that bonds with negative βUNC—those that perform poorly in uncertain times—earn higher average returns. This premium is not explained by standard risk factors or bond characteristics.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- ICAPM (Merton, 1973): Investors require compensation for assets that perform poorly when investment opportunities deteriorate.

- Downside Risk and Hedging Demand: Bonds with negative βUNC (bond-level beta to economic uncertainty) are poor hedges; they lose value when uncertainty rises.

- Credit and Liquidity Risk Amplification: Uncertainty spikes often coincide with tightening credit and bond illiquidity.

📌 Why It Matters:

This premium is distinct from known bond risk premia (e.g., default, term, liquidity). It captures investor aversion to macro uncertainty and helps price bonds more accurately—especially during crises.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Corporate Bond Returns: TRACE + Mergent FISD (2002–2017)

- Macroeconomic Uncertainty Index: Jurado et al. (2015)

- Risk Factors: Fama-French, Carhart, Bai et al. bond factors

- Controls: Credit rating, maturity, size, liquidity, past returns

Model / Methodology

- βUNC Estimation: 36-month rolling regression of excess bond returns on change in uncertainty index

- Portfolio Sorting: Bonds ranked by βUNC into quintiles

- Alpha Models:

- 5-Factor (stocks), 4-Factor (bonds), 9-Factor (combined), 11-Factor (with liquidity, momentum)

- Fama-MacBeth Regressions: Test βUNC with controls and competing risk measures

Trading Strategy (Built from Insights)

- Signal Generation:

- Go long bonds with lowest βUNC (most exposed to uncertainty)

- Avoid bonds with positive βUNC (safe during uncertainty spikes)

- Portfolio Formation:

- Monthly rebalancing into βUNC-sorted quintiles

- Risk Management:

- Filter out recently downgraded bonds or monitor credit transitions

- Integrate βUNC as a factor in multi-asset risk models

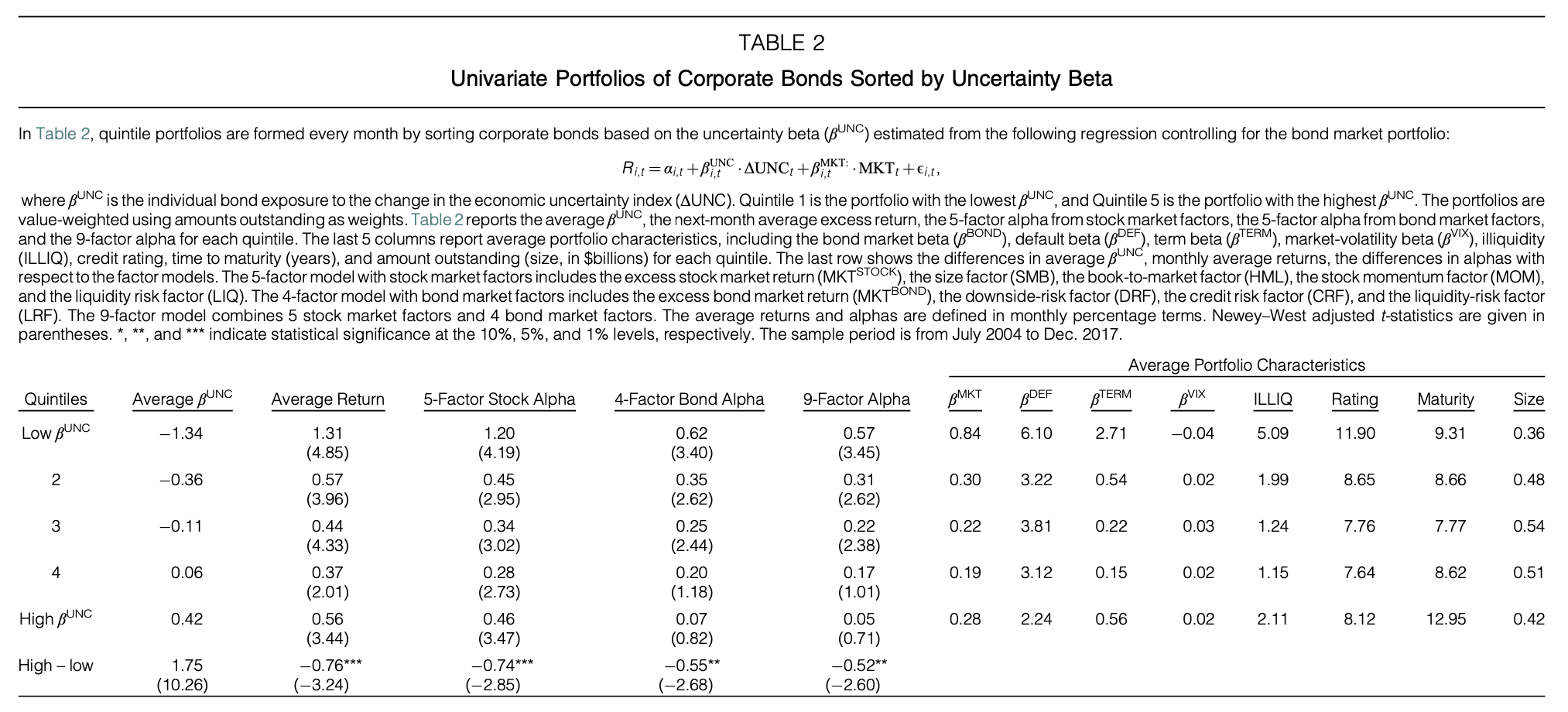

Key Table or Figure from the Paper

📌 Explanation:

- Shows a strong monotonic return spread between bonds with low and high βUNC (bond-level beta to economic uncertainty)

- Monthly return spread: 0.76% (t-stat: –3.24)

- Even after controlling for 9 factors, the alpha spread remains significant (–0.52%)

- The effect is stronger for downgraded and high-yield bonds

Final Thought

💡 Macroeconomic uncertainty isn’t just noise—it reshapes bond risk premia and pricing. 🚀

Paper Details (For Further Reading)

- Title: The Macroeconomic Uncertainty Premium in the Corporate Bond Market

- Authors: Turan G. Bali, Avanidhar Subrahmanyam, Quan Wen

- Publication Year: 2021

- Journal/Source: Journal of Financial and Quantitative Analysis

- Link: https://doi.org/10.1017/S0022109020000538