💡 Takeaway:

ChatGPT captures commodity sentiment better than BERT, BoW, or macroeconomic variables—offering robust, predictive signals for commodity futures returns.

Key Idea: What Is This Paper About?

The paper constructs a Commodity News Ratio Index (CNRI) by analyzing 2.5M news articles using ChatGPT. Each article is scored based on whether ChatGPT believes it signals a price increase or decrease. These sentiment signals are aggregated into a commodity-level CNRI and distilled using Partial Least Squares (PLS) to forecast commodity futures index excess returns.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Investor Sentiment: Media sentiment influences commodity markets, especially when driven by global narratives.

- LLMs Extract Informational Signals: ChatGPT outperforms classical NLP (BoW, BERT) by capturing deeper semantics and context.

- Slow News Diffusion: Commodities are less covered in financial media, allowing sentiment to diffuse slowly into prices.

- Predictive Link to Macro: CNRI also predicts GDP, IPI, CFNAI, and PPI—suggesting macroeconomic underpinnings.

📌 Why It Matters:

This approach provides forward-looking, interpretable, and systematic sentiment-driven signals using LLMs—extending NLP-based forecasting to commodities.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Text Corpus: 2.6M articles (1946–2022) from 9 major newspapers

- Commodities: 18 (e.g., crude oil, gold, soybeans, zinc)

- Returns: Monthly commodity futures index excess returns (Levine et al. 2018)

Model / Methodology

- Step 1: Use ChatGPT to classify articles as “GOING UP”, “GOING DOWN”, or “UNKNOWN”

- Step 2: Compute a Commodity News Ratio (CNR) = (Good − Bad) / Total articles (past 3 months)

- Step 3: Use PLS to form the ChatGPT-based CNRI from 18 CNRs

- Step 4: Forecast commodity index returns using CNRI

- Comparison Models: BERT-based CNRI, BoW-based CNRI, macroeconomic indicators, business cycle controls

Trading Strategy (Investor Application)

- Signal: Use CNRI to forecast next 1–12 months of commodity index returns

- Portfolio Construction:

- Allocate between commodity futures and T-bills

- Use CNRI forecasts in mean-variance optimization

- Volatility estimated using 12-month rolling GSCI standard deviation

- Performance:

- Highest Sharpe: 0.407 (3-month horizon)

- Highest CER: 5.86% (1-month horizon)

- Robust across macro states (recessions, backwardation, inflation down)

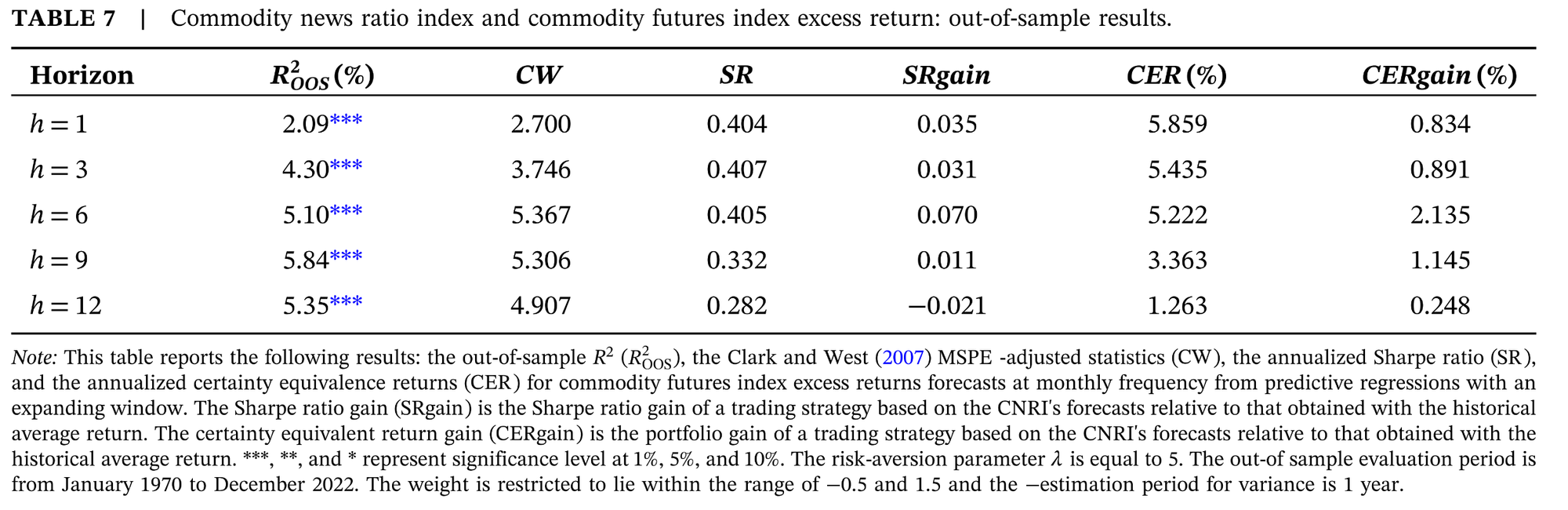

Key Table or Figure from the Paper

📊 Reference: [Table 7] – Out-of-Sample Forecasting and Portfolio Performance

📌 Explanation:

- Shows the CNRI achieves out-of-sample R² from 2.09% to 5.84%

- Sharpe Ratios exceed benchmark across all horizons

- CER gains peak at 2.1%–2.2% over 6–9 month horizons

- CNRI outperforms both economic indicators and BERT-based sentiment

Final Thought

💡 ChatGPT decodes commodity headlines into portfolio alpha—NLP for futures trading is here. 🚀

Paper Details (For Further Reading)

- Title: ChatGPT and Commodity Return

- Authors: Shen Gao, Shijie Wang, Yuanzhi Wang, Qunzi Zhang

- Publication Year: 2025

- Journal/Source: Journal of Futures Markets

- Link: https://doi.org/10.1002/fut.22568