Performance

- Gold returns are predictable, with variance risk premium (VRP) and jump tail risk being key drivers.

- Gold’s expected returns move with stocks and bonds, but realized returns are uncorrelated or negative, especially in crises.

- Gold does not hedge inflation, as both expected and realized gold returns show no strong link to inflation trends.

- Gold’s risk premium behaves differently from its realized returns, challenging its traditional role as a safe-haven asset.

Key Idea

This paper challenges the conventional wisdom about gold as a safe haven and inflation hedge. Instead, it shows that gold’s risk premium is time-varying and predictable based on volatility and jump risk factors. While many believe gold protects against market downturns, the study finds that gold’s expected returns tend to rise with stocks and bonds, contradicting its reputation as a crisis hedge.

Economic Rationale

- Volatility Drives Returns: The variance risk premium (VRP) and jump tail risk predict future gold returns, similar to how they impact equity markets.

- Gold as a Sentiment Asset: Demand for gold increases in turbulent markets, but its expected returns don’t behave as a true hedge.

- No Inflation Protection: Unlike traditional views, gold returns don’t consistently react to inflation, making it unreliable as an inflation hedge.

Practical Applications

- Volatility-Based Gold Strategies: Use variance risk premium (VRP) and jump tail risk as predictors for gold trading models.

- Cross-Market Signals: Watch equity and bond market risk premiums, as gold’s risk premium moves in sync with them.

- Crisis Trading: Short gold during market stress if realized returns follow past trends of negative co-movement with stocks.

- Reassessing Inflation Hedges: Investors looking to hedge inflation should not rely on gold alone, as its inflation link is weak.

How to Do It

Data

- Gold futures and options from NYMEX/COMEX.

- Equity risk premium data from S&P 500.

- Bond risk premium estimates based on forward rates and yield curves.

- Macroeconomic indicators: Inflation, industrial production, and U.S. dollar strength.

Model/Methodology

- Predictive regressions to forecast gold’s excess returns.

- Variance risk premium (VRP) and jump tail risk measures used as main predictors.

- Time-varying co-movement analysis with stocks, bonds, and inflation.

- Rolling-window estimations to test out-of-sample predictability.

Strategy

- Gold Volatility Strategy: Long gold when VRP and jump tail risk signal higher risk premiums.

- Stock-Gold Divergence Play: Monitor expected gold returns vs. realized returns—when they diverge, short-term reversals may occur.

- Bond-Gold Relationship: Short gold when bond risk premium spikes, as gold’s expected return tends to rise alongside bonds.

- Inflation Trade Adjustment: If using gold as an inflation hedge, combine it with assets that have stronger inflation sensitivity, such as commodities tied to energy and agriculture.

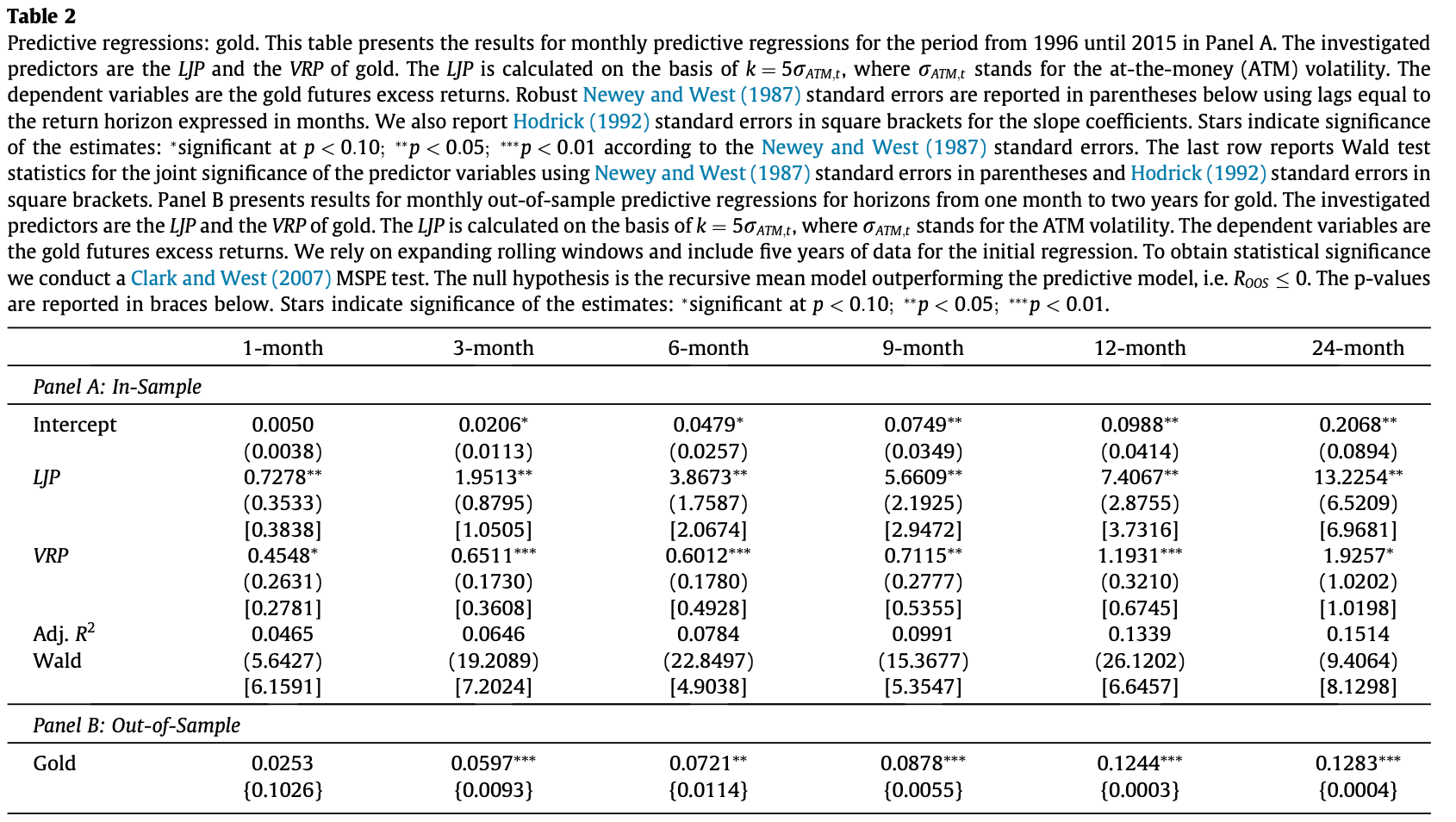

Table or Figure

- Variance risk premium (VRP) and left jump tail risk (LJP) are the strongest predictors of future gold returns.

- Predictability holds both in-sample and out-of-sample, meaning traders can use these signals in real-time.

Paper Details

- Authors: Duc Binh Benno Nguyen, Marcel Prokopczuk, Chardin Wese Simen

- Published: 2019

- Source: Journal of International Money and Finance

- DOI: 10.1016/j.jimonfin.2019.02.011