📊 Performance

- The risk premium in Treasury bonds varies more frequently than business cycles.

- A new factor ("cycle factor") explains excess bond returns better than traditional forward rate models.

- The model outperforms Cochrane-Piazzesi’s single-factor return predictor in and out of sample.

💡 Key Idea

The paper introduces a "cycle factor" to decompose Treasury yields into inflation expectations and a risk-premium component. This approach enhances return forecasting and outperforms traditional models that rely solely on forward rates.

📚 Economic Rationale

Most term-structure models focus on level, slope, and curvature. The authors instead emphasize economic drivers:

- Expected Inflation (trend inflation).

- Real Short Rate (business-cycle component).

- Risk Premium (new "cycle factor").

By isolating these components, they show that bond risk premia move at a higher frequency than previously thought.

🚀 Practical Applications

- Improved Bond Return Forecasting – A better predictor of excess bond returns across maturities.

- More Accurate Risk Premium Estimation – Reduces sensitivity to measurement errors in yield data.

- Better Asset Allocation – Helps investors time exposure to Treasury bond risk premia more effectively.

🛠️ How to Do It

Data

- US Treasury yield curve data (1971–2011).

- Inflation expectations from survey and historical CPI data.

- Forward rates & excess bond returns.

Model/Methodology

- Decomposes yields into trend inflation, real short rate, and risk premium.

- Constructs a "cycle factor" to predict excess returns.

- Controls for inflation expectations to separate risk premia from interest rate movements.

Strategy

- Use the cycle factor to time bond allocations – Capture periods of high risk premia.

- Avoid relying only on forward rates – They contain excess noise and do not fully explain returns.

- Monitor real-rate cycles – These provide key signals for bond risk premia shifts.

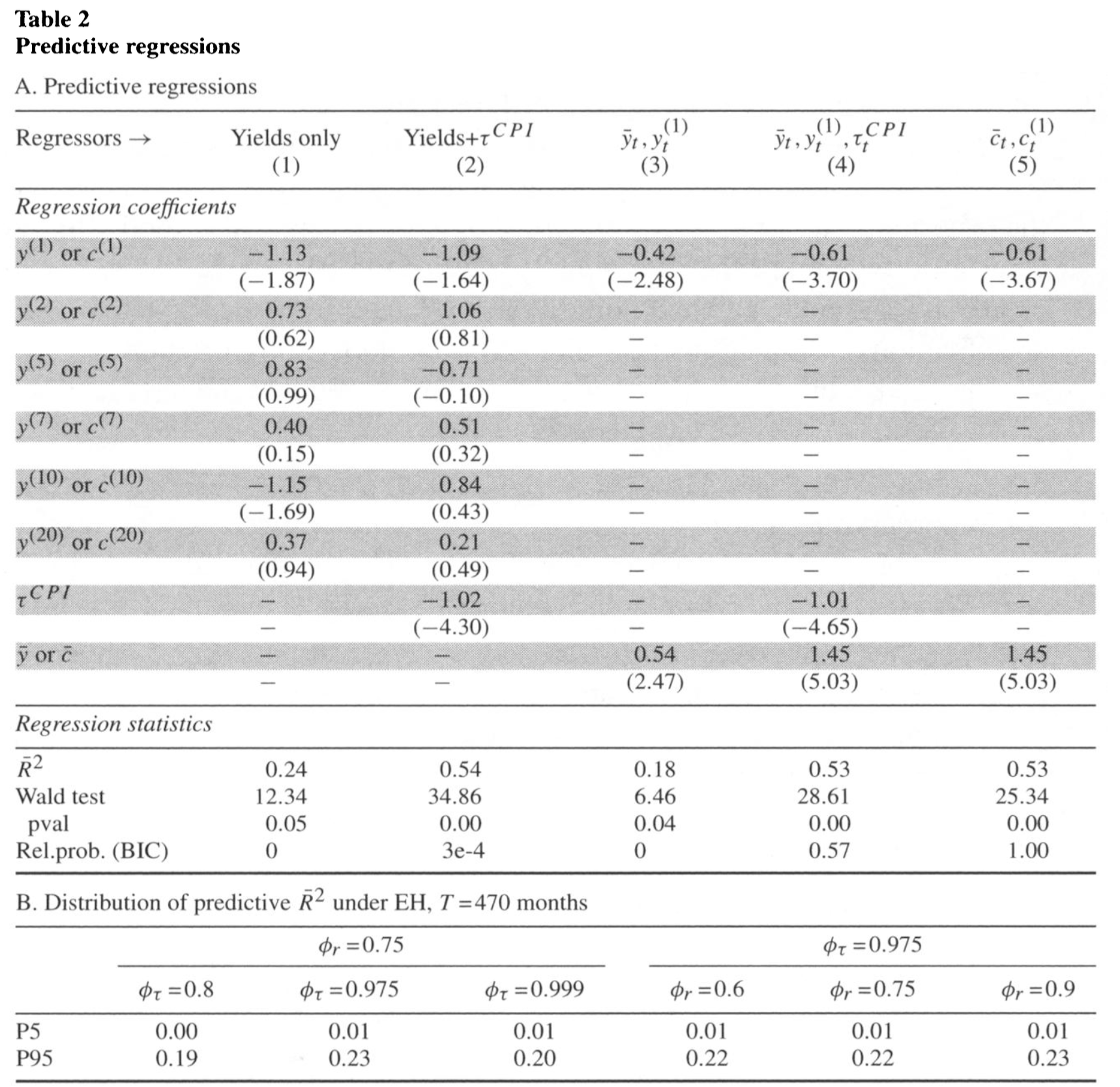

📊 Table or Figure

📌 The cycle factor outperforms forward rate models in predicting excess Treasury bond returns out of sample, improving return forecasts by 10-30%.

📄 Paper Details

- Authors: Anna Cieslak & Pavol Povala

- Journal: The Review of Financial Studies (2015)

- DOI: 10.1093/rfs/hhv032