💡 Takeaway:

The GAN-based SDF model dominates benchmarks across every asset pricing metric—explaining more return variation, capturing more pricing anomalies, and generating higher Sharpe ratios with lower risk.

Key Performance Metrics

- Out-of-Sample Annual Sharpe Ratio: 2.6 (GAN) vs. 0.8 (FF5), 1.7 (linear GAN), 1.5 (FFN)

- Explained Return Variation (Individual Stocks): 8%

- Cross-Sectional R²: 23%

- Explained Variation on Anomaly Portfolios: >90% on all 46 decile sorts

- Robust to Size Restrictions: Sharpe Ratio = 1.4 on top 1,500 stocks

Key Idea: What Is This Paper About?

The paper estimates the stochastic discount factor (SDF) for all U.S. equities using a deep learning asset pricing model. It combines three neural network architectures:

- A feedforward network to model non-linear interactions,

- An LSTM to extract macroeconomic hidden states,

- A GAN to select the most informative pricing moments.

By embedding no-arbitrage constraints into the training, the model avoids overfitting and delivers strong pricing performance both in- and out-of-sample.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- No-Arbitrage Pricing: SDF is estimated via conditional moment constraints across all assets.

- Machine Learning as General GMM: GAN selects the most mispriced portfolios for moment enforcement.

- Heterogeneous Risk Premia: Risk loadings (βs) vary non-linearly with characteristics and macroeconomic states.

- Time-Varying Dynamics: LSTMs learn economic regimes (booms/recessions) from macro data instead of using lagged variables or differences.

📌 Why It Matters:

This approach integrates machine learning into asset pricing without discarding economic structure, offering interpretable, testable, and practically useful models.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Returns: Monthly stock returns from CRSP (1967–2016)

- Characteristics: 46 firm-specific predictors

- Macro Data: 178 time series from FRED, Compustat, and Welch-Goyal

- Assets: 10,000+ stocks, 46 anomaly portfolios

Model / Methodology

- SDF Estimation:

- GAN solves a minimax game: minimize pricing errors across all stocks vs. maximize pricing failure across conditions

- Architecture:

- Feedforward Network (SDF weights ω)

- LSTM (macroeconomic hidden states)

- GAN (moment condition selection)

- Comparison Benchmarks:

- FFN (simple deep learner), EN (elastic net), LS (linear special case), FF3 and FF5

Trading Strategy (From SDF Output)

- Signal Generation:

- Use GAN-estimated risk loadings (β) to sort stocks

- Long high-β (high SDF exposure), short low-β

- Portfolio:

- Mean-variance efficient SDF portfolio

- Rebalance monthly

- Risk Metrics:

- Max drawdown, turnover, max loss compared across models

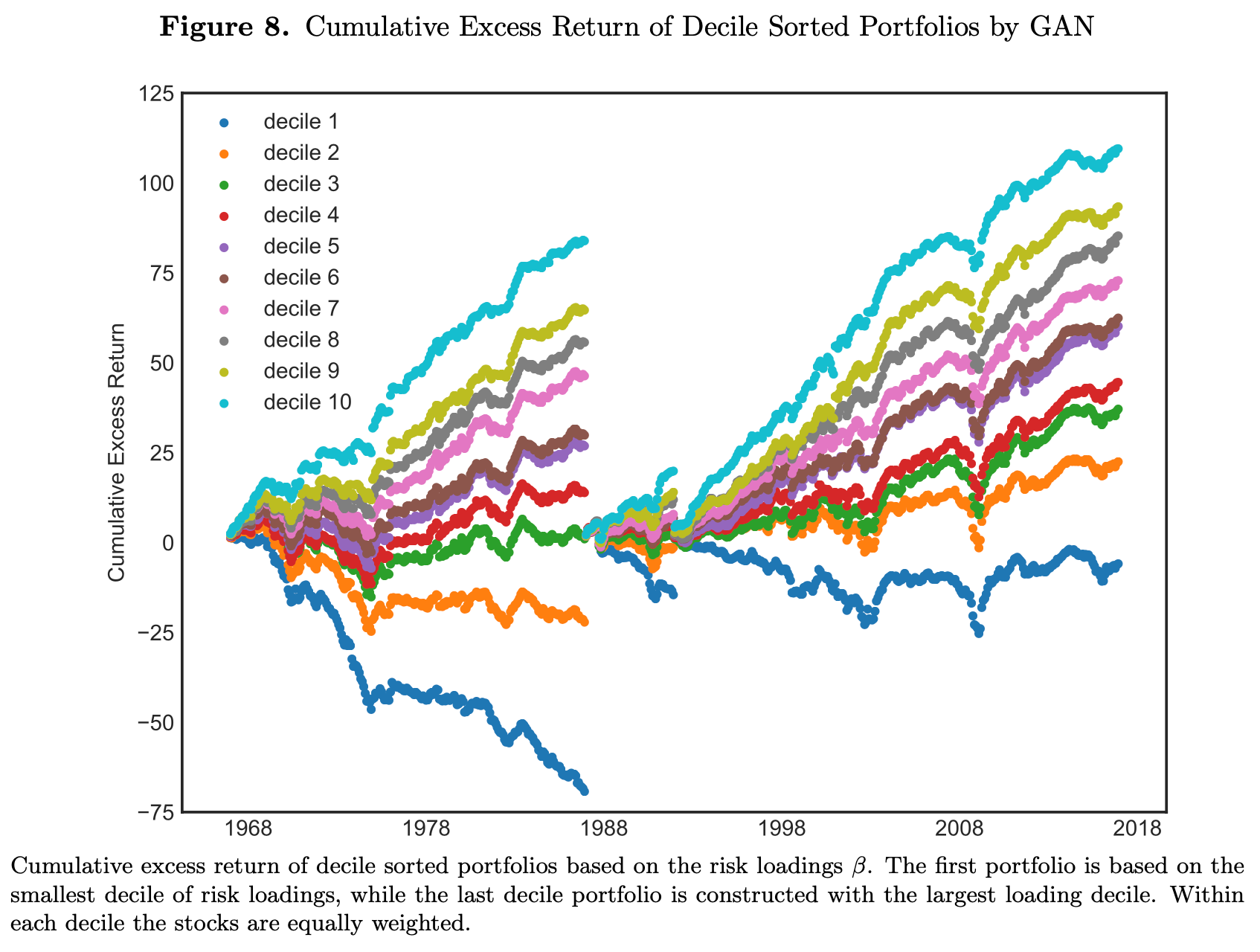

Key Table or Figure from the Paper

📊 Reference: [Figure 8] – Cumulative Return of β-Sorted Portfolios (Test Sample)

📌 Explanation:

- Stocks sorted by GAN-estimated β loadings produce monotonic return patterns.

- Top decile outperforms bottom decile by 48% per year.

- None of the Fama-French factors explain the return spread—GRS test strongly rejects.

- This validates that the GAN model captures systematic pricing risks.

Final Thought

💡 Deep learning with economic discipline solves asset pricing better than ever before. 🧠📈

Paper Details (For Further Reading)

- Title: Deep Learning in Asset Pricing

- Authors: Luyang Chen, Markus Pelger, Jason Zhu

- Publication Year: 2019

- Journal/Source: SSRN Working Paper

- Link: https://ssrn.com/abstract=3350138