Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Monthly Out-of-Sample R² (NN3): 0.40% (stocks), up to 1.80% (portfolios)

- Annualized Sharpe Ratio (Long-Short Decile, NN3):

- Equal-Weight: 2.45

- Value-Weight: 1.35

- S&P 500 Market Timing Sharpe (NN3): 0.77 vs. 0.51 (Buy & Hold)

- Predictive Accuracy: Robust across 30,000 stocks and 60 years

💡 Takeaway:

Nonlinear ML methods, especially neural networks, dramatically outperform standard asset pricing models in return prediction and investment performance.

Key Idea: What Is This Paper About?

This paper systematically compares traditional and machine learning models for forecasting stock returns using over 900 predictors. It finds that ML methods—particularly trees and neural networks—capture complex nonlinear and interaction effects that standard models miss. These models generate higher Sharpe ratios, more accurate predictions, and more meaningful risk premium measures.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Nonlinear Risk Structures: Risk premia reflect complex nonlinear and interactive effects, which ML models can detect.

- Variable Selection & Regularization: Lasso, ridge, and ensemble trees reduce overfitting in high-dim setups.

- Behavioral Pricing: ML picks up mispricing not modeled in standard linear risk-return frameworks.

- Model Averaging via Ensembles: Reduces prediction variance and improves robustness.

📌 Why It Matters:

ML tools allow asset pricing models to go beyond static factor structures and account for real-world complexity and massive predictor sets.

Data, Model, and Strategy Implementation

Data Used

- Period: 1957–2016

- Stocks: ~30,000 US equities

- Covariates: 94 firm-level variables × 8 macro indicators + 74 industry dummies = 920+ signals

- Returns: Monthly (main), annual (robustness)

Model / Methodology

- Linear Models: OLS, Lasso, Ridge, Elastic Net

- Dimension Reduction: PCR, PLS

- Trees: Random Forest, Gradient Boosted Trees

- Neural Nets: Feedforward NNs (1–5 layers), ReLU activation

- Tuning: Validation set optimization, Huber loss used in many models

- Out-of-Sample Evaluation: R², Sharpe Ratio, Diebold-Mariano test

Trading Strategy (Machine Learning Portfolio)

- Signal: Sort stocks by predicted return

- Portfolio Construction:

- Long top decile, short bottom decile (monthly)

- Equal-weighted and value-weighted versions

- Sharpe Ratio (NN3):

- Equal-Weight: 2.45

- Value-Weight: 1.35

- Market Timing:

- NN3 predicts S&P 500 with 1.80% R², Sharpe up to 0.77

- Useful for overlay macro risk hedging

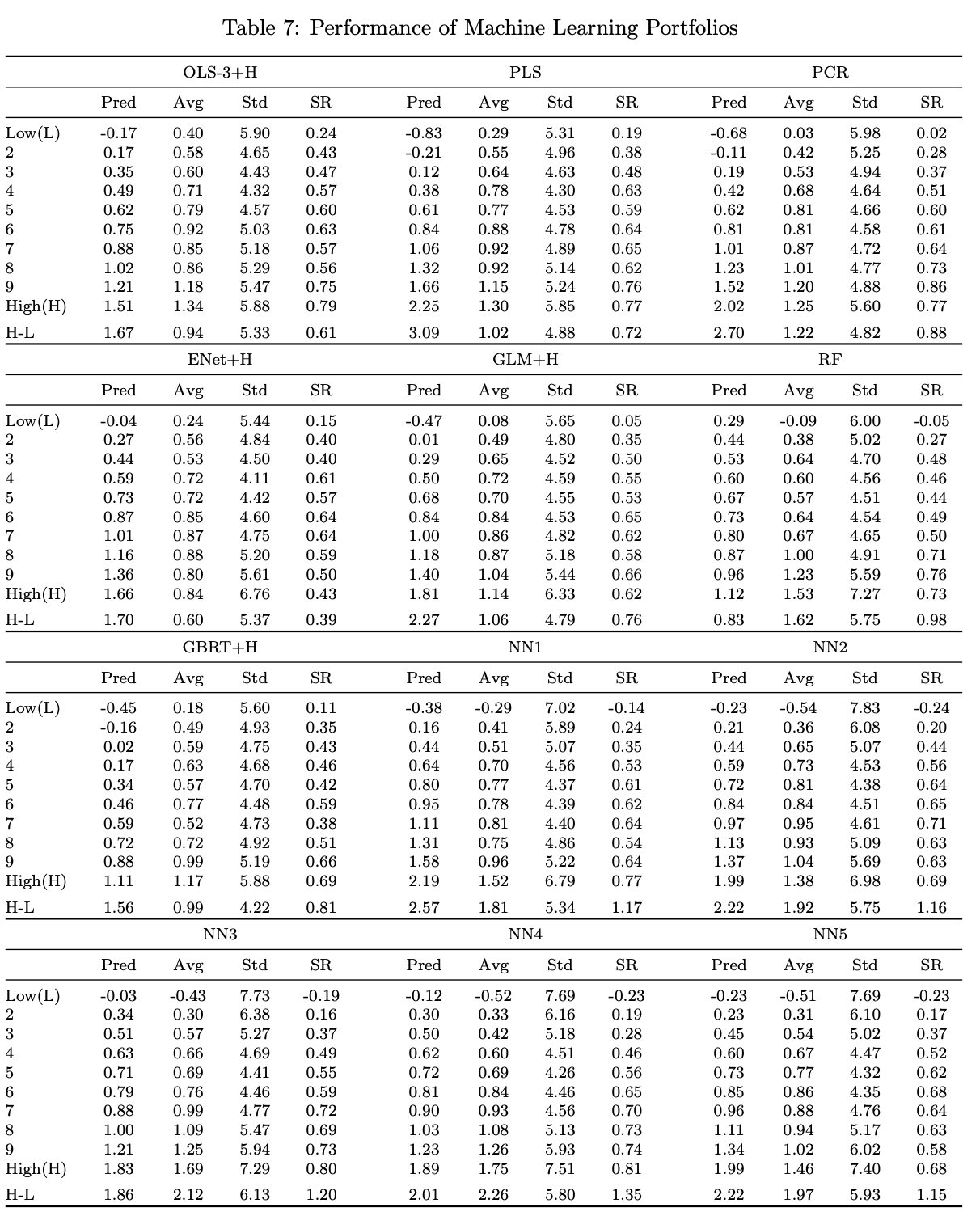

Key Table or Figure from the Paper

📊 Reference: [Table 7] – Machine Learning Long-Short Portfolio Performance

📌 Explanation:

- Long-short decile portfolios built from model predictions

- NN3 and NN4 outperform all other models

- NN3 (equal-weighted): 2.45 Sharpe

- Linear models like OLS and PCA lag significantly

- Confirms that ML provides alpha even under real-world constraints

Final Thought

💡 Machine learning isn't just better forecasting—it's better investing. 🧠📈

Paper Details (For Further Reading)

- Title: Empirical Asset Pricing via Machine Learning

- Authors: Shihao Gu, Bryan Kelly, Dacheng Xiu

- Publication Year: 2019

- Journal/Source: SSRN Working Paper

- Link: https://ssrn.com/abstract=3335536