📈 Performance

- A strategy that selects stocks based on their historical same-calendar-month returns earns an average return of 13% per year (1963–2011).

- A metastrategy that takes long and short positions on 15 anomalies based on historical same-calendar-month premiums earns 1.88% per month (t-value = 6.43).

- Adding a seasonality factor to a portfolio of market, size, value, and momentum increases the Sharpe ratio from 1.04 to 1.67.

💡 Key Idea

Return seasonalities exist across stocks, factors, commodities, and international markets. Stocks that performed well in a specific month tend to do so again in the future. These seasonalities overwhelm unconditional expected return differences and are intertwined with other return anomalies.

📊 Economic Rationale

- Return seasonalities aggregate across systematic factors like size, value, and industry.

- Market-wide seasonality in risk premiums translates into cross-sectional seasonal effects.

- Anomalies such as accruals and equity issuances exhibit strong seasonal variation.

- The evidence does not support macroeconomic risk explanations.

🛠 Practical Applications

- Factor Investing: Enhance factor portfolios by integrating seasonality signals.

- Timing Strategies: Adjust portfolio exposures based on seasonal anomaly strengths.

- Hedge Funds & Asset Managers: Use seasonality-based stock selection and factor tilts.

- Commodity & FX Trading: Leverage cross-sectional seasonal effects beyond equities.

🚀 How to Do It

Data

- Monthly stock returns from NYSE, AMEX, NASDAQ (1963–2011).

- Fama-French factor returns.

- International stock indices and commodity futures.

Model/Methodology

- Fama-MacBeth cross-sectional regressions to analyze seasonal return patterns.

- Portfolio sorts: Long-short portfolios based on historical same-calendar-month returns.

- Factor decomposition to determine the role of size, value, and industry exposures.

- Sharpe ratio maximization with seasonality factors.

Strategy

- Sort stocks by their historical same-calendar-month return over the past 20 years.

- Go long on the top-decile stocks and short the bottom-decile stocks.

- Hold positions for one month and rebalance at the start of each month.

- Repeat across different asset classes (equities, commodities, FX, indices).

📊 Table or Figure

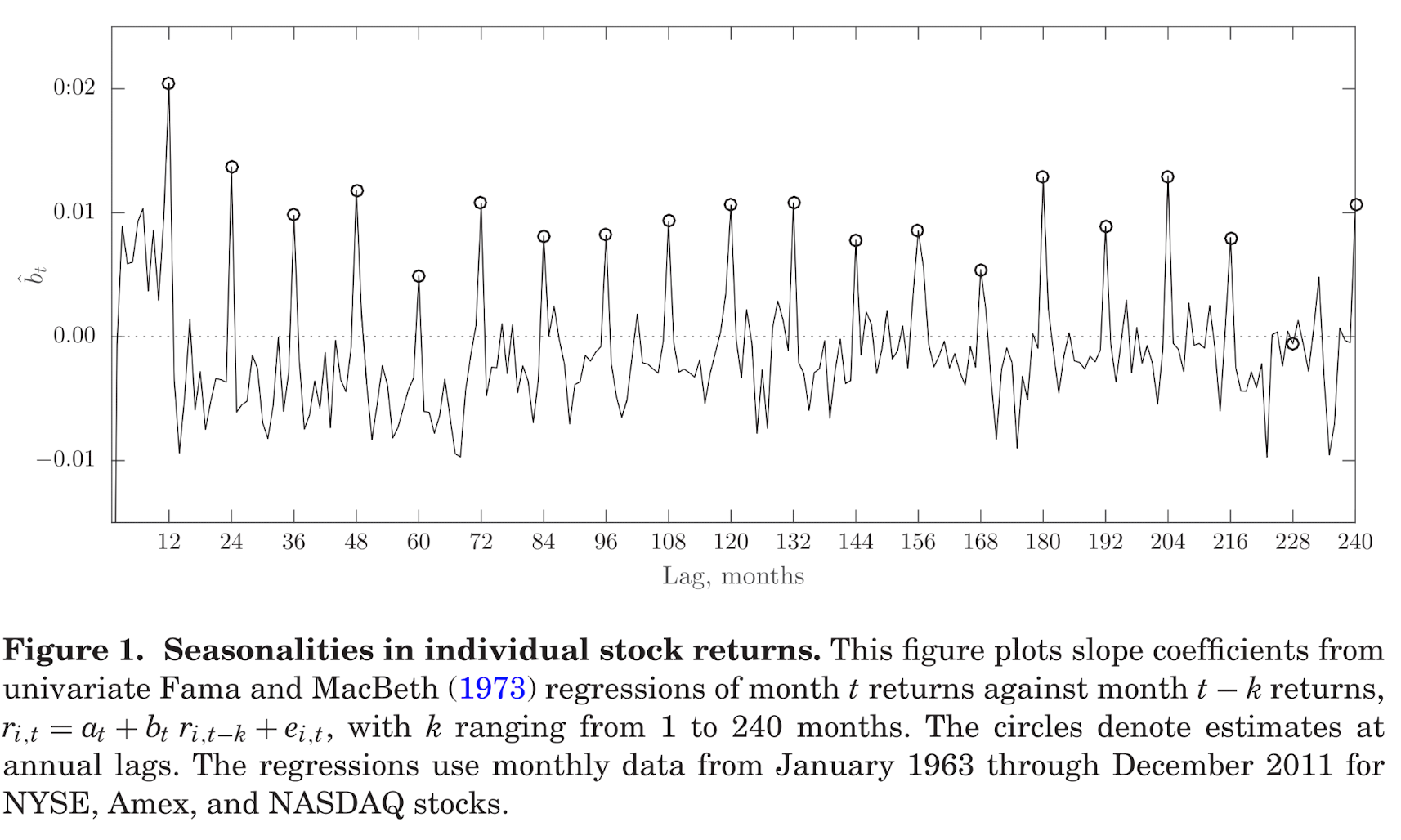

📌 Key Evidence: Figure 1 shows slope coefficients from cross-sectional regressions of monthly stock returns against past returns at different lags, revealing persistent annual return patterns.

📜 Paper Details

- Authors: Matti Keloharju, Juhani T. Linnainmaa, and Peter Nyberg

- Published in: The Journal of Finance, August 2016

- DOI: 10.1111/jofi.12398

More detail ...

🔨 Constructing the Seasonality Factor

- Sort stocks into portfolios based on their historical same-calendar-month returns over the past 20 years.

- Go Long: Stocks in the top percentile of historical same-month returns.

- Go Short: Stocks in the bottom percentile.

- Compute the return spread between the long and short portfolios.

- The return spread forms the seasonality factor (HML-Seasonality).

🚀 Building a Strategy Using Seasonality in Anomalies

The paper shows that anomalies exhibit strong seasonal variation. A meta-strategy that rotates anomalies based on their historical same-calendar-month performance earns 1.88% per month (t-value = 6.43). This suggests that combining anomaly factors with seasonality can be profitable.

How to Construct the Strategy

- Select Anomalies: Use common factor anomalies (e.g., momentum, value, accruals, equity issuance).

- Compute Seasonal Signals: For each anomaly, calculate average performance in the same calendar month over the past 20 years.

- Rank Anomalies: Identify the top 3 best-performing anomalies and the worst 3 based on same-month returns.

- Go Long/Short: Construct a long-short portfolio, buying the top anomalies and shorting the worst.

- Monthly Rebalancing: Adjust holdings at the beginning of each month based on updated seasonal performance.