💡 Takeaway:

Factor timing leads to meaningful gains, doubling utility compared to static factor investing and outperforming pure market timing strategies.

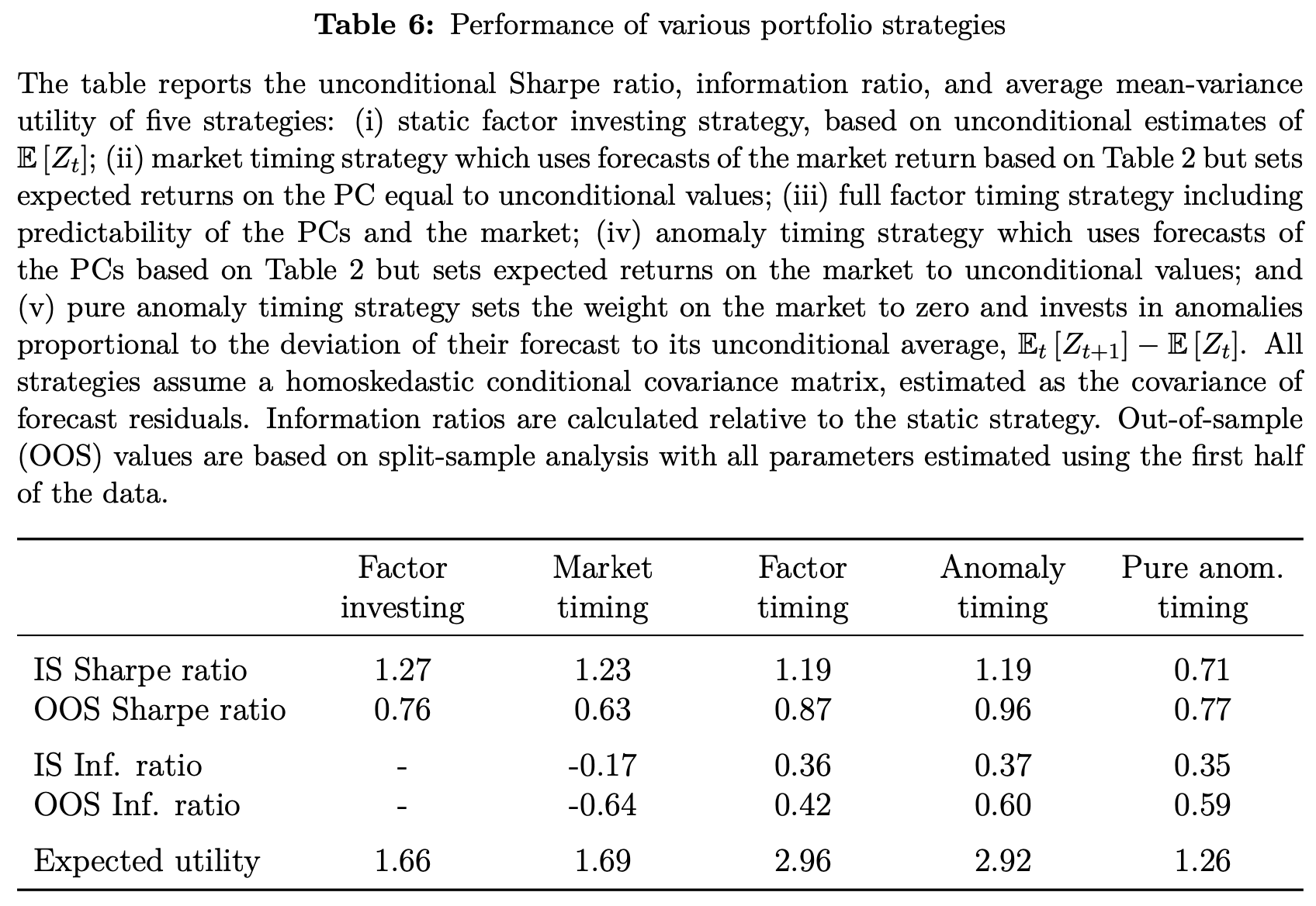

Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Sharpe Ratio (Out-of-Sample):

- Static Factor Investing: 0.76

- Full Factor Timing: 0.87

- Pure Anomaly Timing: 0.77

- Monthly Alpha (Composite Mood Beta Portfolios): Up to 2.37%

- SDF Variance: Increases from 1.67 (static) to 2.96 (timing)

Key Idea: What Is This Paper About?

This paper introduces a method for timing equity factor exposures using valuation ratios (like book-to-market) to predict future returns of principal components (PCs) of anomaly portfolios. By forecasting only the most important factors (top 5 PCs), they reduce noise and avoid overfitting. The resulting portfolio strategy earns superior risk-adjusted returns and reveals that the true stochastic discount factor (SDF) is more volatile and dynamic than previously thought.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Time-Varying Risk Premia: Expected returns on equity factors change over time with macro cycles and investor preferences.

- No Near-Arbitrage Principle: Without excessive Sharpe ratios, only dominant components (large PCs) of factor returns should be predictable.

- Dimensionality Reduction (PCA): Predicting a few key PCs avoids noise and identifies common sources of factor return dynamics.

📌 Why It Matters:

These findings challenge traditional asset pricing models, suggesting that multiple, time-varying sources of risk premia drive returns, not a single market factor.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Assets: 50 equity anomaly portfolios (e.g., value, size, momentum)

- Time Period: 1974–2017

- Source: CRSP, COMPUSTAT

- Predictors: Portfolio-level book-to-market ratios

Model / Methodology

- Use Principal Components Analysis (PCA) to reduce 50 anomalies to top 5 PCs

- Forecast each PC using its own valuation ratio (bm)

- Use out-of-sample (OOS) validation and placebo tests to ensure robustness

- Construct Stochastic Discount Factor (SDF) from predicted PC returns

Trading Strategy

- Signal Generation:

- Predict top 5 PC returns monthly using each PC’s valuation ratio

- Portfolio Construction:

- Long-short strategy: Overweight PCs with higher expected returns

- Include or exclude market exposure depending on version (pure anomaly vs. full timing)

- Rebalancing: Monthly (robust to lower frequencies like quarterly/annual)

Key Table or Figure from the Paper

📌 Explanation:

- Shows performance of five portfolio variants (static, market timing, factor timing, anomaly timing, pure anomaly timing)

- Full factor timing portfolio earns the highest Sharpe (0.87 OOS) and expected utility

- Timing only anomalies yields 0.77 OOS Sharpe—higher than market timing (0.63)

Final Thought

💡 You don’t need to time the market. Timing factor exposures can deliver stronger and more consistent alpha. 🚀

Paper Details (For Further Reading)

- Title: Factor Timing

- Authors: Valentin Haddad, Serhiy Kozak, Shrihari Santosh

- Publication Year: 2020

- Journal/Source: NBER Working Paper No. 26708

- Link: https://www.nber.org/papers/w26708