💡 Takeaway:

Stocks with greater exposure to positive foreign industry news earn significantly higher returns. The alpha survives after controlling for size, value, momentum, volatility, and industry effects.

Key Idea: What Is This Paper About?

This paper shows that multinational firms’ stock prices do not promptly reflect foreign news from the industries they operate in. By combining geographic sales data with foreign industry returns, they create a predictive signal—Foreign_Info—which forecasts stock returns globally. The effect is strongest where investor attention is low and markets are segmented.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limited Attention: Investors neglect foreign data, especially in less-followed firms.

- Information Frictions: Language barriers, media coverage, and reporting lags delay reaction to foreign shocks.

- Market Segmentation: Local biases slow cross-border arbitrage.

- Delayed Incorporation: Foreign signals diffuse gradually into stock prices over 1–3 months.

📌 Why It Matters:

This paper provides direct evidence of slow information diffusion across borders, creating a global mispricing opportunity in otherwise efficient markets.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Markets: 22 developed countries (2001–2013)

- Firm Data: Sales geography (Worldscope, Compustat), returns (CRSP, Datastream)

- Industry Returns: ICB Supersector by country

- Attention Proxies: Analyst coverage, institutional ownership, Google Trends

Model / Methodology

- Foreign_Info: Sales-weighted foreign industry returns (excluding home market)

- Portfolio Sorts: Quintile & tercile sorts by Foreign_Info

- Risk Adjustment: Carhart 4-factor & Fama-French 5-factor (global versions)

- Regression Controls: Size, value, momentum, idiosyncratic volatility, turnover, industry momentum

Trading Strategy (Foreign Info Long-Short)

- Signal Generation:

- Compute Foreign_Info using sales breakdown and foreign industry returns

- Rank stocks monthly based on Foreign_Info

- Portfolio Construction:

- Long: Top quintile (most positive foreign news)

- Short: Bottom quintile

- Value-weighted, monthly rebalanced

- Enhancement:

- Focus on firms with low attention (small-cap, few analysts)

- Avoid firms with 100% domestic sales

- Use in combination with momentum or earnings news

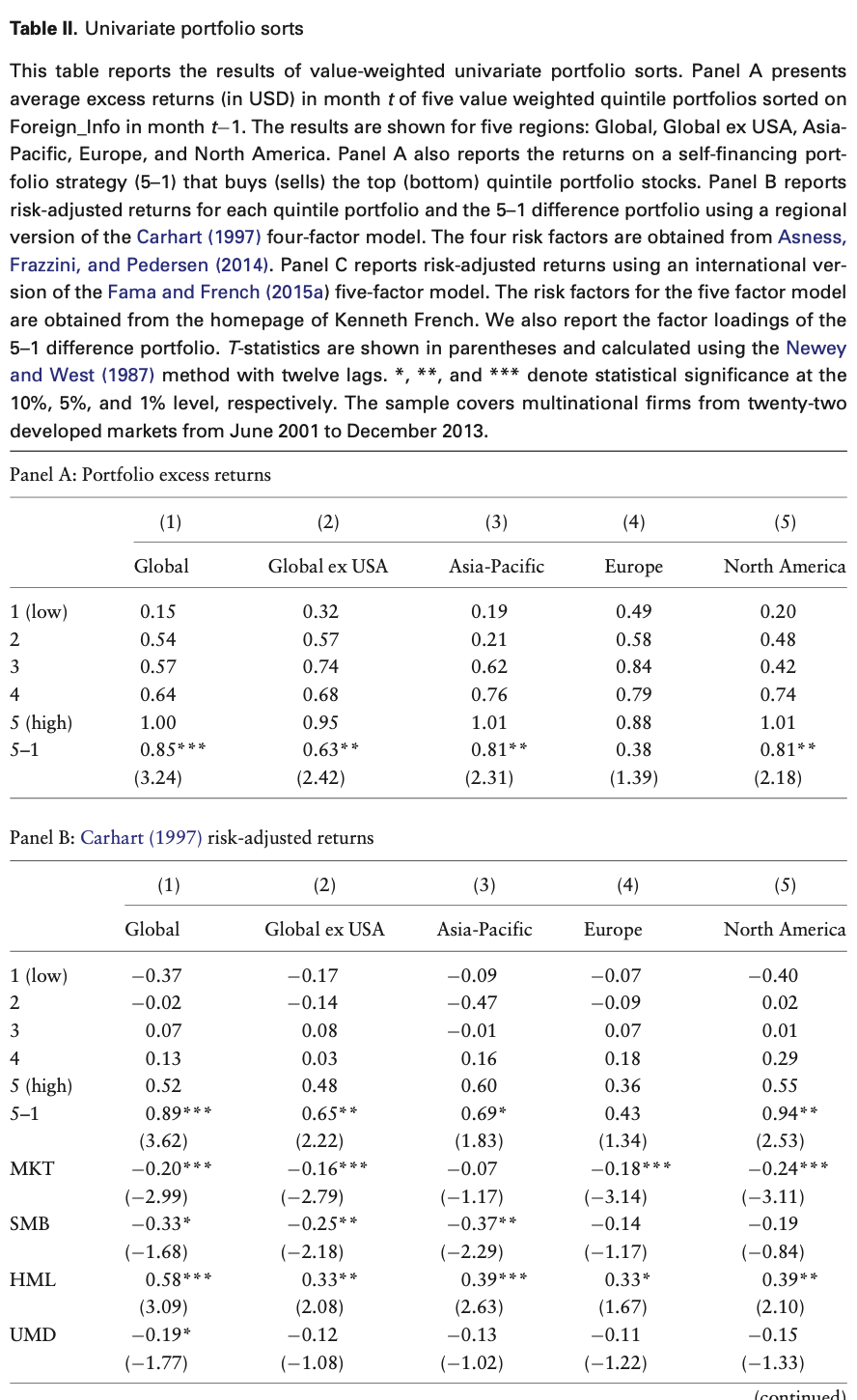

Key Table or Figure from the Paper

📌 Explanation:

- Firms with high Foreign_Info earn 1.00%/month; low Foreign_Info firms earn 0.15%.

- The 5–1 long-short portfolio earns 0.85%/month (t = 3.24), or 10.2%/year.

- Alpha persists even when controlling for size, value, momentum, and other firm traits.

Final Thought

💡 The market pays attention to local news—but forgets the rest of the world. That’s where the alpha is. 🌍🚀

Paper Details (For Further Reading)

- Title: Does Foreign Information Predict the Returns of Multinational Firms Worldwide?

- Authors: Christian Finke, Florian Weigert

- Publication Year: 2017

- Journal/Source: Review of Finance

- Link: https://doi.org/10.1093/rof/rfw070