The study highlights that during financial crises, hedge funds and commodity index traders (CITs) tend to liquidate positions as market volatility (measured by VIX) rises. This leads to price declines and increases the burden on commercial hedgers. Understanding these flows can help traders anticipate price movements.

💡 Key Idea

In normal times, financial traders provide liquidity to hedgers in commodity markets. However, in times of market stress, financial traders exit, forcing commercial hedgers to absorb more risk. This "risk convection" from distressed financial traders to commercial hedgers drives market dislocations.

📖 Economic Rationale

The study aligns with theories on liquidity constraints (Kyle & Xiong, 2001) and financial distress (Brunnermeier & Pedersen, 2009). During crises, financial institutions face margin calls and funding constraints, leading to fire sales of commodity futures. Meanwhile, commercial hedgers, who would usually be net short, are forced to take the other side of these trades.

⚡ Practical Applications

- Crisis Trading: If volatility spikes (VIX rises), expect hedge funds and CITs to reduce long positions in commodity futures, causing prices to drop.

- Liquidity Analysis: Monitor commercial hedgers’ behavior—if they are forced to take the long side, it may indicate distressed selling by financial players.

- Event-Driven Strategies: Use financial stress indicators (CDS spreads, margin conditions) to predict commodity price movements.

🔧 How to Do It

📑 Data

- Source: Commodity Futures Trading Commission (CFTC) Large Trader Reporting System

- Metrics: VIX, CDS spreads, net positions of financial traders vs. commercial hedgers

📈 Model & Methodology

- Event-Driven Framework: Track changes in financial traders' net positions in response to VIX spikes.

- Regression Analysis: Test the sensitivity of CITs, hedge funds, and commercial hedgers' positions to volatility shocks.

- Cross-Sectional Analysis: Distressed financial traders (higher CDS spreads) show stronger selling pressure.

🎯 Trading Strategy

- Identify Stress Events – Use VIX and CDS spreads to detect financial distress.

- Monitor Positioning Shifts – If financial traders unwind positions, anticipate price declines.

- Trade the Dislocation – Go short on commodities where financial traders are exiting.

- Look for Rebalancing Opportunities – As commercial hedgers absorb risk, anticipate stabilization and potential mean reversion.

📊 Table or Figure

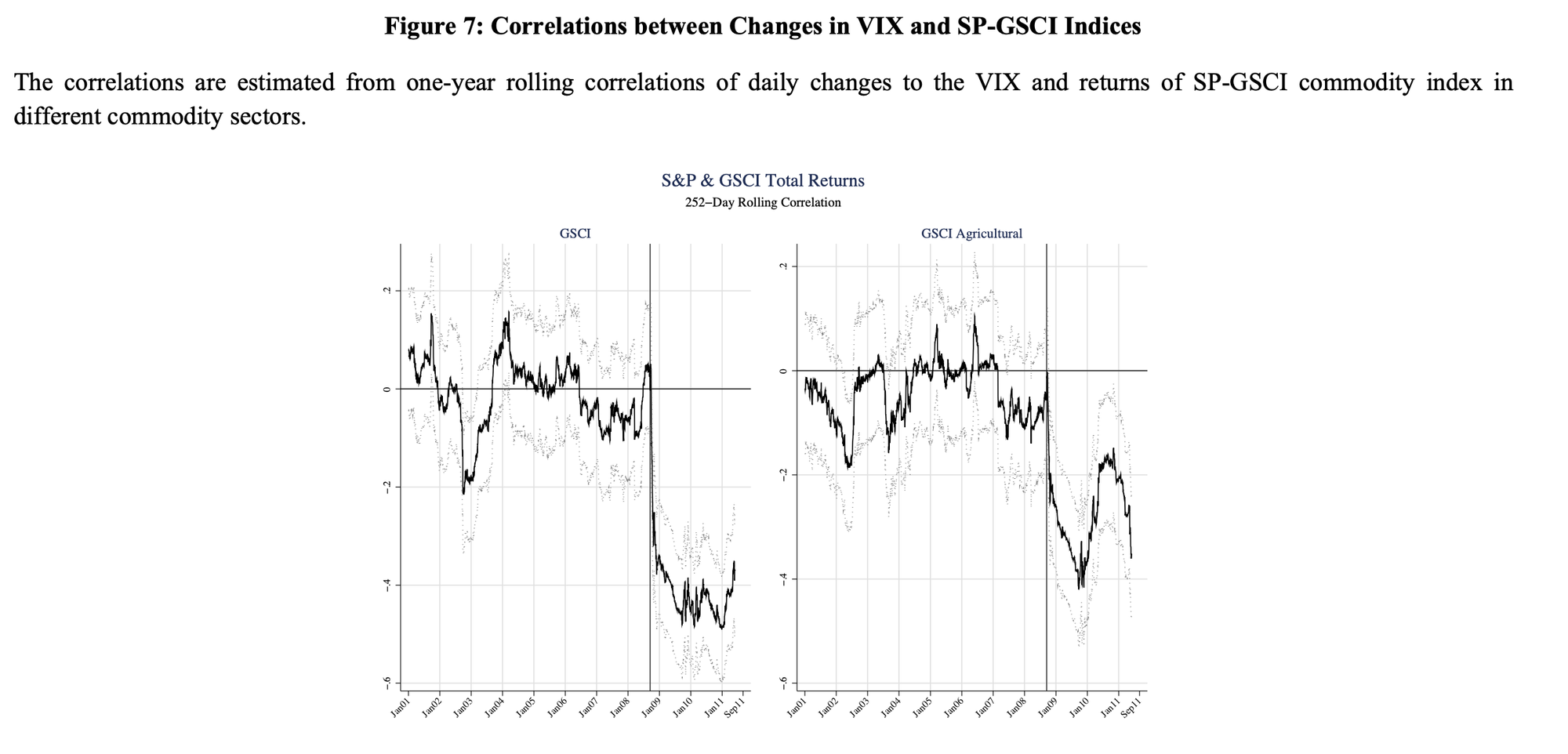

The figure illustrates the correlation between commodity prices and the VIX. It shows that after the 2008 financial crisis, commodity prices moved inversely with the VIX, confirming that financial traders were offloading positions while commercial hedgers absorbed risk.

📄 Paper Details

Authors: Ing-Haw Cheng, Andrei Kirilenko, and Wei Xiong

Title: "Convective Risk Flows in Commodity Futures Markets"

Source: NBER Working Paper No. 17921

Year: 2012