💡 Takeaway:

Insiders don’t try to mask their trades. They demand liquidity and move prices quickly, with the first few trades in a sequence triggering most of the market reaction.

Key Idea: What Is This Paper About?

The paper examines how insiders trade—using unique intraday data from the Toronto Stock Exchange that flags every insider trade. Contrary to recent theory, insiders focus on trading early (return timing), not hiding their trades (liquidity timing). As a result, their trades are easily detectable, and prices adjust within minutes.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Kyle (1985): Insiders should split trades and hide in noise—but don’t.

- Holden & Subrahmanyam (1992): Competing insiders act quickly, making detection easier.

- Limited Attention/Skill: Many insiders use unsophisticated brokers or trade through basic online accounts.

📌 Why It Matters:

Challenges theories that suggest insiders can stay undetected by timing liquidity. Shows the market responds to their order flow immediately, making insider detection measurable and policy-relevant.

Data, Model, and Strategy Implementation

Data Used

- Exchange: Toronto Stock Exchange (TSX)

- Period: Oct 2004 – Dec 2006

- Unique Feature: Insider status flagged on every trade/order

- Granularity: Intraday (centisecond-level)

Model / Methodology

- Track insider trades vs market impact (price impact, spread)

- Compare sequences of insider trades to identify execution strategy

- Measure reaction speed: quote changes, order imbalance, price impact

- Proxy for informedness: abnormal returns post-trade

Trading Strategy (Informed by Insights)

This paper does not offer a direct trading strategy, but it informs these ideas:

- Mimicking Opportunity: Piggyback early on insider trade sequences (first 1–5 trades show the strongest price impact).

- Order Flow Detection: Use real-time flow to detect abnormal trade sizes and patterns.

- Intraday Timing Filter: Focus on high-volume spikes with increasing order imbalance and deteriorating execution quality—likely insider-driven.

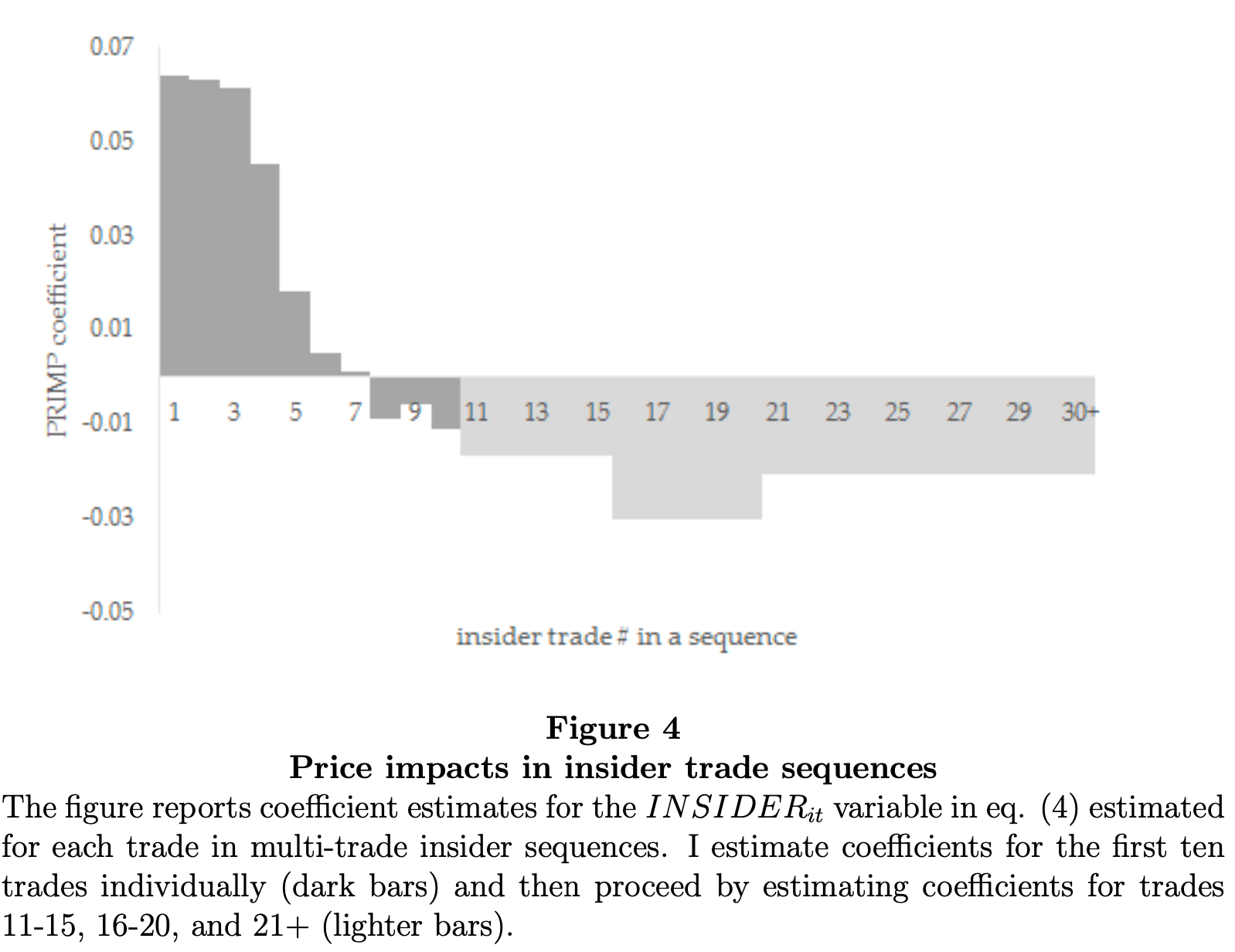

Key Table or Figure from the Paper

📌 Explanation:

- Shows that the first 1–5 insider trades have the highest price impact.

- Later trades have smaller or even negative impacts, as the market adjusts.

- Suggests that insiders front-load their information, creating early alpha (and poor execution later).

Final Thought

💡 Insiders may know the story—but their trading tells the market faster than they think. 🚀

Paper Details (For Further Reading)

- Title: Insider Trading Under the Microscope

- Author: Andriy Shkilko

- Publication Year: 2019

- Journal/Source: Wilfrid Laurier University Working Paper

- Link: https://www.wlu.ca/academics/faculties/lazaridis-school-of-business-and-economics/research/working-paper-series/assets/resources/insider-trading-under-the-microscope.pdf