Performance

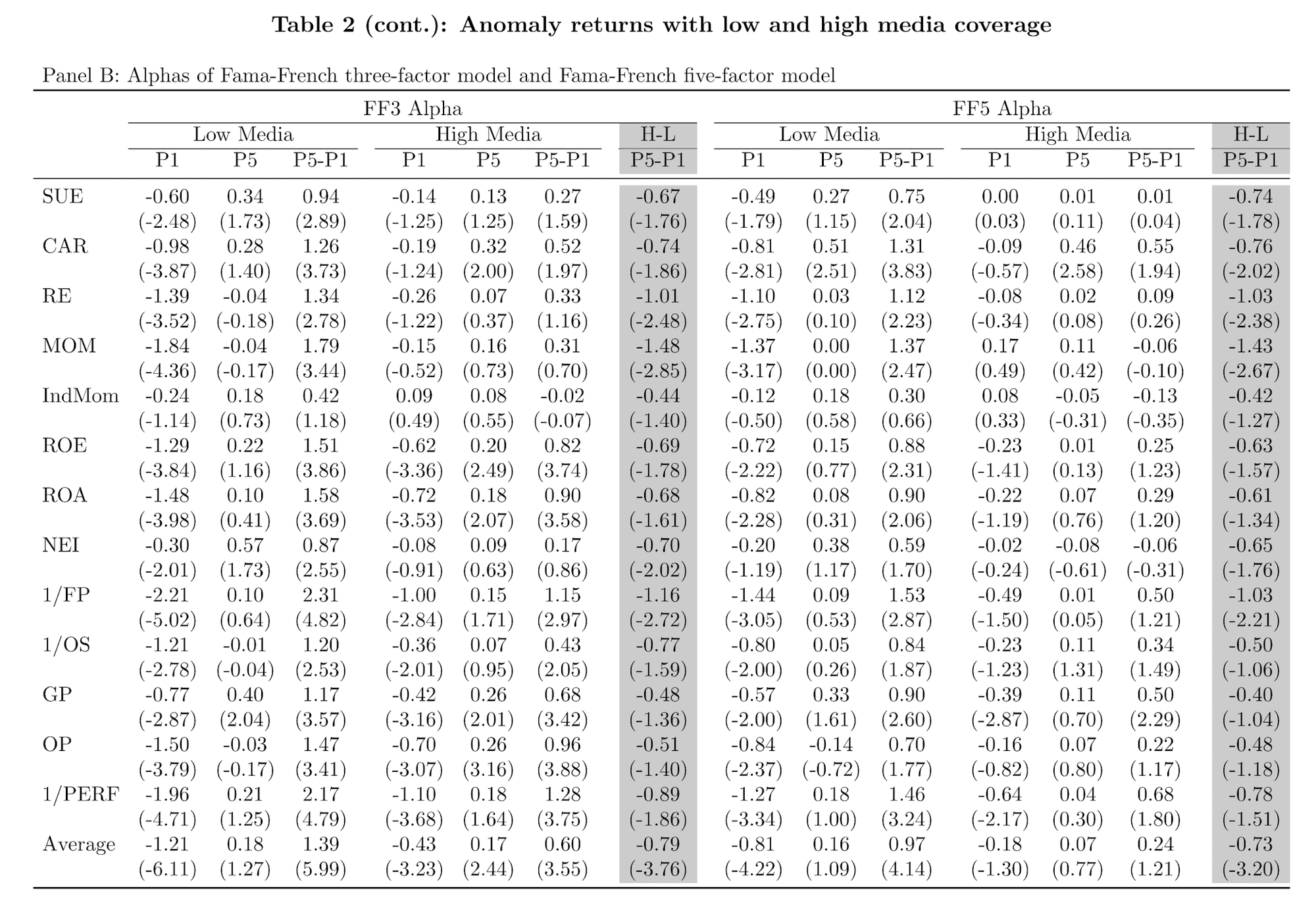

- Average Fama-French Five-Factor Alpha Spread: 0.97% per month (low media coverage) vs. 0.24% per month (high media coverage).

- Most of the alpha spread comes from the short leg of anomalies and stocks with high arbitrage costs.

- Key Anomalies Studied: PEAD, MOM, ROE, PERF, PMU, RMW.

Key Idea

Investor inattention significantly amplifies anomalies in asset pricing. Stocks with low media coverage experience stronger underreaction-related anomalies, resulting in persistent mispricings that generate alpha for traders.

Basically, stocks with low media coverage tend to have stronger anomaly returns, meaning higher alpha and Sharpe ratios for certain trading strategies. However, they also tend to be more expensive to trade due to higher arbitrage costs (e.g., low liquidity, high volatility, short-sale constraints).

Economic Rationale

- Limited attention hypothesis: Investors fail to fully process information for stocks with low media coverage, leading to delayed price adjustments.

- Limits to arbitrage: High arbitrage costs prevent hedge funds from correcting mispricings quickly, making anomalies persist longer.

- Behavioral biases: The interaction of media coverage and investor biases (anchoring, conservatism) reinforces mispricings.

Practical Applications

- Trading Strategy: Focus on anomaly-based factor models where mispricing is more pronounced (e.g., profitability, momentum, PEAD).

- Hedge Fund Strategy: Exploit short leg anomalies in low-attention stocks for high alpha generation.

- Risk Management: Avoid stocks with high arbitrage costs that may trap capital in slow-to-correct anomalies.

How to Do It

Data

- Stock Returns: CRSP

- Firm Accounting Data: Compustat

- Media Coverage Proxy: RavenPack (Dow Jones newswire)

- Investor Attention Proxies: Google search volume, EDGAR downloads, analyst coverage

Model/Methodology

- Double Sorting: First on media coverage, then on anomaly signals (profitability, momentum, earnings surprises).

- Fama-MacBeth Regressions: Controlling for risk factors, size, liquidity, and investor ownership.

- Event Study: Analyzing earnings announcement returns to measure post-announcement corrections.

Strategy

- Sort stocks by media coverage (low vs. high).

- Focus on anomaly signals that exhibit stronger effects in low-coverage stocks (e.g., momentum, post-earnings drift).

- Long underpriced stocks & Short overpriced stocks based on anomaly factor signals.

- Avoid high arbitrage cost stocks that could delay mispricing correction.

Table or Figure

Table 2 – Fama-French Five-Factor Alphas by Media Coverage

- High Media Coverage: Weak anomaly performance

- Low Media Coverage: Strong anomaly performance, particularly in short legs.

How to Use This Information in Trading

1. Pick the Right Anomalies

- Momentum (MOM) – Works extremely well, especially in low media coverage stocks.

- Post-Earnings Drift (PEAD) – Stocks underreact to earnings, and corrections happen slowly.

- Profitability (ROA, ROE, PMU) – Higher profitability stocks tend to outperform more in low attention stocks.

2. Trade in a Long-Short Portfolio

- Long: Stocks with strong anomaly signals in the low media coverage group.

- Short: Stocks with weak anomaly signals in the low media coverage group (if feasible).

3. Control for Trading Costs

- Avoid the most illiquid stocks (lowest volume, highest bid-ask spreads).

- Trade in small size to prevent slippage.

- Use limit orders instead of market orders to reduce costs.

4. Time Your Trades Around Earnings Announcements

- These anomalies perform best when earnings surprises are revealed, correcting mispricings.

Paper Details

Title: Attention and Underreaction-Related Anomalies

Authors: Xin Chen, Wei He, Libin Tao, Jianfeng Yu

Publication Date: September 5, 2021

Source: SSRN

🔗 Read Full Paper