Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Monthly Alpha (Risk Factors section): 1.88% (t = 2.76)

- Annualized Return (Nonchangers – Changers): ~22%

- Value-weighted L/S Portfolio Return: Up to 58 bps/month (t = 3.59)

💡 Takeaway:

Firms that significantly change the wording in their 10-Ks underperform systematically, and the market doesn’t react at announcement—only later, as the information slowly gets priced in.

Key Idea: What Is This Paper About?

The authors document that firms making noticeable textual changes in their annual reports (“changers”) experience significantly lower stock returns than firms that don’t (“nonchangers”). These changes often relate to risk disclosures, litigation, or management discussion. Yet, investors overlook these signals, creating large and tradable return differences.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Investor Inattention: Investors rarely compare year-over-year 10-Ks, especially textual differences.

- Information Processing Limits: As 10-Ks grow longer and more complex, investors miss subtle but meaningful changes.

- Behavioral Bias: Without cues like "compared to last year," investors fail to detect content drift.

📌 Why It Matters:

These predictable price drifts challenge the assumption of informational efficiency and reveal exploitable inefficiencies using public data.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- 10-Ks and 10-Qs: SEC EDGAR (1995–2014)

- Metrics Extracted: Document similarity (Cosine, Jaccard, MinEdit, Simple)

- Additional Data: CRSP, Compustat, I/B/E/S, EDGAR download logs

Model / Methodology

- Compute textual similarity between current and prior year 10-Ks using NLP techniques

- Classify firms into quintiles based on similarity scores

- Build long-short portfolios:

- Long Q5 (nonchangers: high similarity)

- Short Q1 (changers: low similarity)

- Test performance using Fama-French 3- and 5-factor alphas

Trading Strategy (Built from Insights)

- Signal Generation:

- After 10-K filing, compute document similarity

- Go long firms with little change (Q5), short those with major changes (Q1)

- Portfolio Construction:

- Value-weighted

- Monthly rebalancing; each firm held for 3 months

- Focus Sections:

- Risk Factors

- MD&A

- Legal Proceedings

- Optional Enhancement:

- Filter for filings lacking investor attention (no comparative phrases or low multi-year downloads)

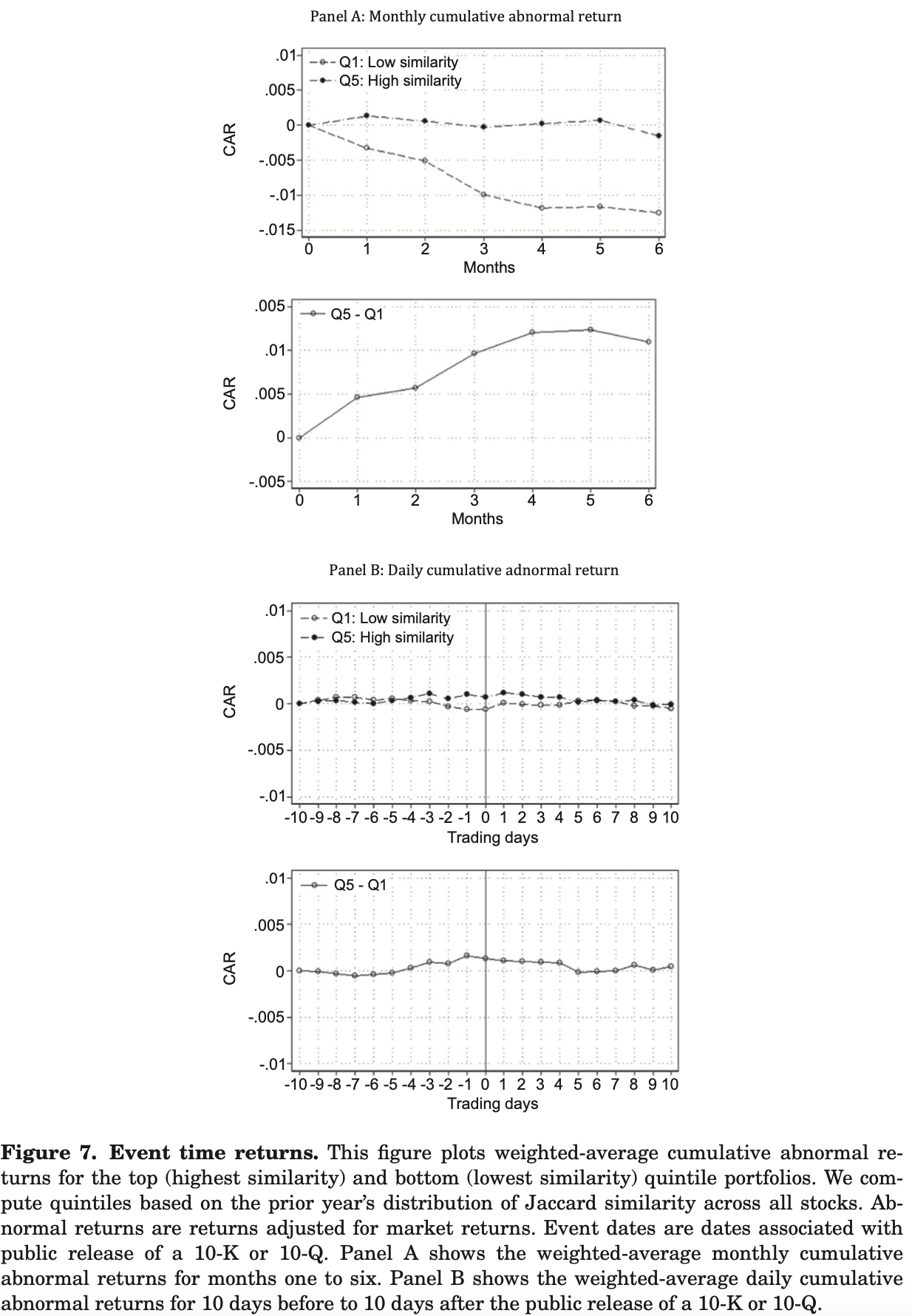

Key Table or Figure from the Paper

📌 Explanation:

- Panel A shows that firms with low similarity 10-Ks (i.e., major changes) underperform over the six months following the filing, while nonchangers outperform.

- Panel B reveals no return reaction at the announcement date, meaning markets don’t price in the news immediately.

- This delayed response implies investor inattention, making the alpha predictable and exploitable.

Final Thought

💡 10-K changes are free alpha—but only if you’re the one actually reading them. 🚀

Paper Details (For Further Reading)

- Title: Lazy Prices

- Authors: Lauren Cohen, Christopher Malloy, Quoc Nguyen

- Publication Year: 2020

- Journal/Source: Journal of Finance

- Link: https://doi.org/10.1111/jofi.12885