💡 Takeaway:

Low-risk anomalies earn strong returns because they exploit mispricing caused by ignoring skewness—especially among firms with high downside risk.

Key Idea: What Is This Paper About?

The authors argue that low-risk anomalies—where low-beta or low-vol stocks outperform—are not true anomalies. CAPM fails because it ignores return skewness, especially from credit risk. High beta/volatility stocks have more negative skew, meaning they have crash risk. Once skew is included in models, these anomalies disappear.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Skewness Preferences: Investors dislike negative skew (downside crash risk), so they demand higher returns.

- CAPM Misspecification: CAPM overestimates expected returns for firms with high downside risk because it ignores skew.

- Default Risk Link: Negative skew is often tied to credit risk—firms at risk of default.

- Options Pricing Evidence: Put options are priced more expensively on these firms—investors are paying for downside protection.

📌 Why It Matters:

This reframes low-risk anomalies from “puzzles” into skew risk premia. The anomalies exist not because of arbitrage constraints or behavioral errors—but because traditional models miss part of the risk.

Data, Model, and Strategy Implementation

Data Used

- Firms: 4,967 US stocks

- Period: Jan 1996 – Aug 2014

- Sources: CRSP, Compustat, OptionMetrics

- Skew Measure: Based on OTM options (calls vs puts)

- Other Metrics: CAPM beta, idio vol (FF3 & CAPM), ex-ante variance

Model / Methodology

- Sort portfolios:

- By ex-ante skew (from options)

- By beta, volatility, or variance

- Double Sorts:

- Evaluate low-risk strategies across skew portfolios

- Skew Risk Premium (SRP):

- Difference between realized and implied skew

- Factor Models:

- FF3 and FF4 regressions used to compute alphas

Trading Strategy (Based on Skew/Beta Interaction)

- Long: Low beta stocks with highly negative skew

- Short: High beta stocks with highly negative skew

- Alternative: Long high-skew (less crash-prone), short low-skew (crash-prone)

- Rebalancing: Monthly

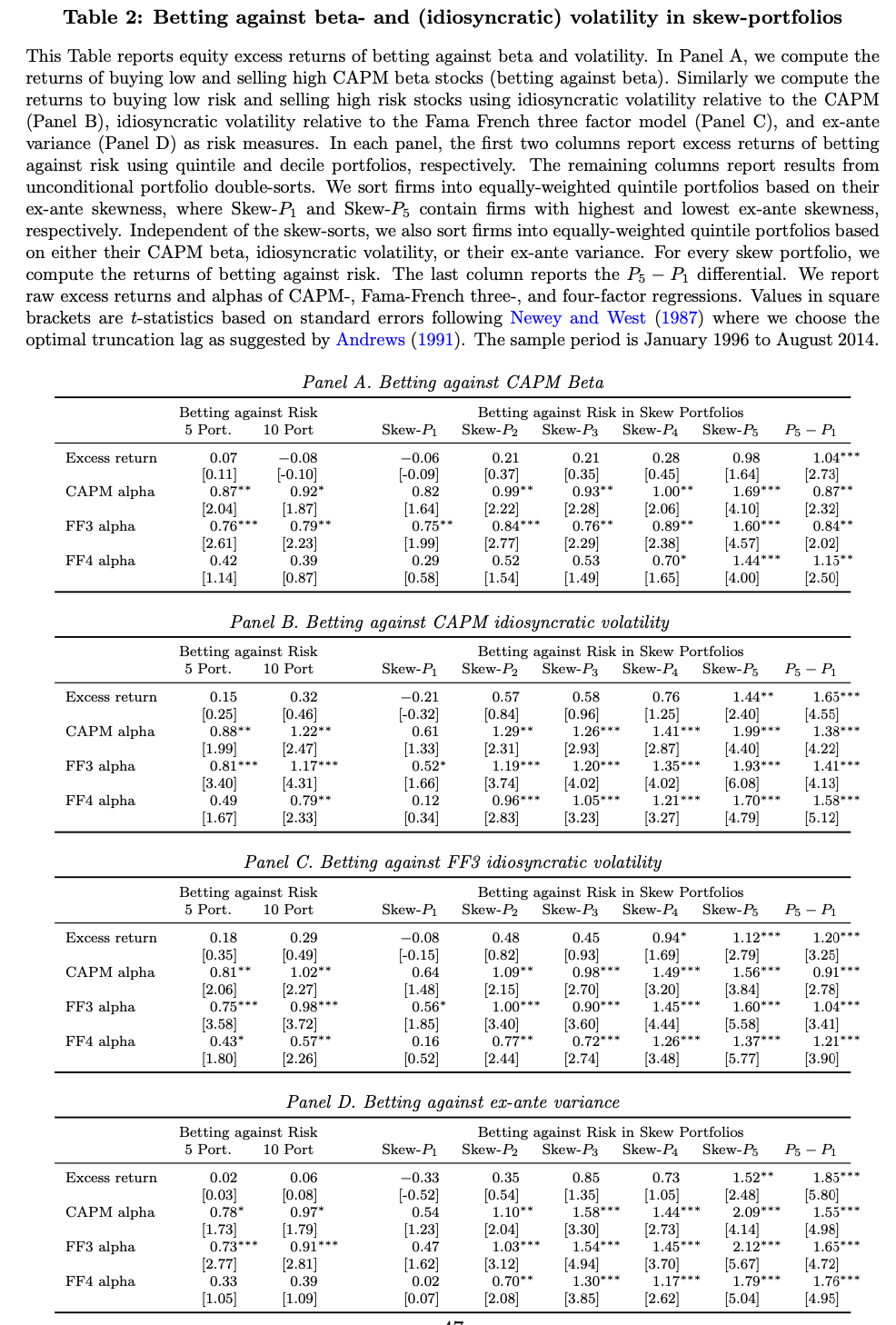

Key Table or Figure from the Paper

📌 Explanation:

- Shows that betting against beta yields highest returns among low-skew stocks (i.e., those most exposed to crash risk)

- FF4 alpha for low-skew group: up to 1.76% per month

- High-skew group: returns near zero

- Confirms that skewness explains when and why low-beta strategies work

Final Thought

💡 Low-risk anomalies aren’t wrong—they just reflect the cost of ignoring skew. 🚀

Paper Details (For Further Reading)

- Title: Low Risk Anomalies?

- Authors: Paul Schneider, Christian Wagner, Josef Zechner

- Publication Year: 2015

- Journal/Source: SSRN Working Paper

- Link: https://ssrn.com/abstract=2593519