Performance

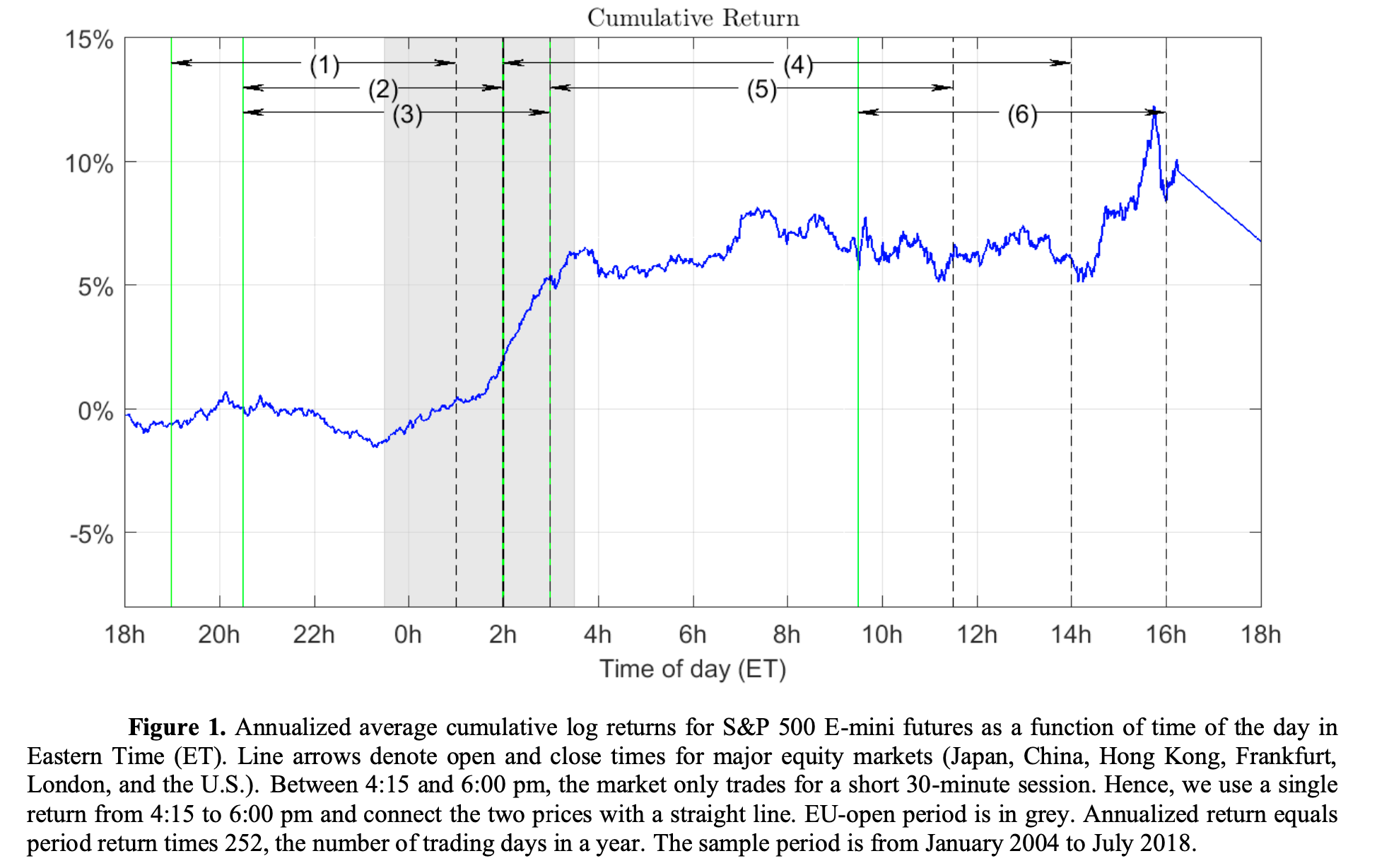

- Key Result: The entire average market return is concentrated in the four-hour window around the European market open (11:30 PM – 3:30 AM ET).

- Annualized Return: 7.6% during this window, while returns are nearly zero for the remaining 20 hours.

- Sharpe Ratio: 1.67 for this period, significantly higher than the full-day market Sharpe.

Key Idea

Stock market returns are not evenly distributed throughout the trading day. Instead, the majority of excess returns are generated during a specific four-hour window before European markets open. This return pattern is consistent across years, months, and weekdays.

Economic Rationale

- Uncertainty Resolution Hypothesis:

- Overnight, uncertainty accumulates as fewer investors are active.

- When European investors enter the market, they incorporate overnight information, resolving uncertainty.

- This causes price increases, explaining why returns cluster during this period.

- Supporting Evidence:

- VIX futures rise during the Asian session (reflecting increasing uncertainty).

- VIX futures drop sharply during the EU-open period, indicating uncertainty resolution.

Practical Applications

- Trading Strategy:

- Buy S&P 500 E-mini futures before 11:30 PM ET and close the position at 3:30 AM ET.

- The strategy is profitable even after transaction costs and has a Sharpe ratio higher than the buy-and-hold alternative.

- Market Timing for Institutions:

- Large institutional trades should be timed before EU-open to capture this return anomaly.

How to Do It

Data

- E-mini S&P 500 futures (ES)

- VIX futures

- Sample period: January 2004 – July 2018

- Intraday minute-by-minute price data from CME

Model/Methodology

- Identify high-return windows:

- Compute annualized returns by minute over 24-hour trading sessions.

- Compare cumulative returns for different time windows.

- Measure uncertainty resolution:

- Track overnight VIX movements and correlation with EU-open returns.

- Test robustness:

- Adjust for microstructure biases (bid-ask bounce, market impact).

- Control for external shocks (FOMC days, macroeconomic news).

Strategy Execution

- Enter Long Position: Buy S&P 500 E-mini futures at 11:30 PM ET.

- Exit Position: Close at 3:30 AM ET before London open.

- Risk Management:

- Avoid trading on European holidays (returns are lower).

- Use conditional trading based on overnight volatility and VIX movements to improve Sharpe ratio.

- Capacity Estimate:

- The strategy can scale up to $9 billion in exposure, generating $50 million in annualized after-cost profits.

Key Figure

Figure 1 shows cumulative market return across 24 hours.

- Returns remain flat throughout most of the day except for the EU-open period.

- No other trading window exhibits statistically significant positive returns.

Paper Details

- Authors: Oleg Bondarenko & Dmitriy Muravyev

- Publication: SSRN Electronic Journal, 2020

- Link: SSRN Abstract