💡 Takeaway:

Mood-sensitive stocks generate high returns in upbeat periods and underperform in downbeat ones—creating predictable and profitable long-short opportunities.

Key Idea: What Is This Paper About?

The paper introduces the concept of Mood Beta—a measure of how sensitive a stock's return is to seasonal changes in investor mood. Investors are more optimistic during certain months (e.g., January, March, Fridays) and more pessimistic in others (e.g., September, October, Mondays). Stocks with higher exposure to this mood sensitivity tend to perform better in positive mood periods and worse in negative ones.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Investor Mood Cycles: Psychological literature shows predictable mood shifts (e.g., SAD effects, weekend mood lift).

- Affective Valence and Risk Preferences: Positive moods increase risk tolerance; negative moods reduce it.

- Mispricing of Factor Exposure: Mood shifts cause systematic over- and underpricing of assets based on mood sensitivity.

📌 Why It Matters:

This behaviorally driven risk premium is not captured by traditional factor models or sentiment measures. It explains a range of anomalies and seasonal patterns across assets.

Data, Model, and Strategy Implementation

Data Used

- Time Period: 1963–2016

- Assets: US stocks, 94 Baker-Wurgler portfolios, 79 KLN portfolios

- Mood Periods:

- High Mood: January, March, Friday

- Low Mood: September, October, Monday

Model / Methodology

-

Mood Beta Calculation:

- Regression of asset returns on market returns during high/low mood periods

- Rolling windows (monthly: 10 years, daily: 6 months)

- Composite Mood Beta = 1st PCA of monthly + daily mood betas

-

Key Hypotheses:

- Mood Recurrence: Performance repeats in same mood states

- Mood Reversal: Performance reverses across opposite mood states

- Mood Beta Effect: High mood beta = higher returns in high-mood periods, lower in low-mood ones

Trading Strategy (Mood-Beta Based)

-

Signal Generation:

- Sort assets by mood beta

- Go long top decile in high mood periods; short bottom

- Reverse positions in low mood periods

-

Portfolio Construction:

- Equal-weighted decile portfolios

- Monthly and weekly rebalancing

-

Risk Management:

- Use composite mood beta to diversify across daily and monthly signals

- Factor-adjusted performance evaluation (4- and 5-factor models)

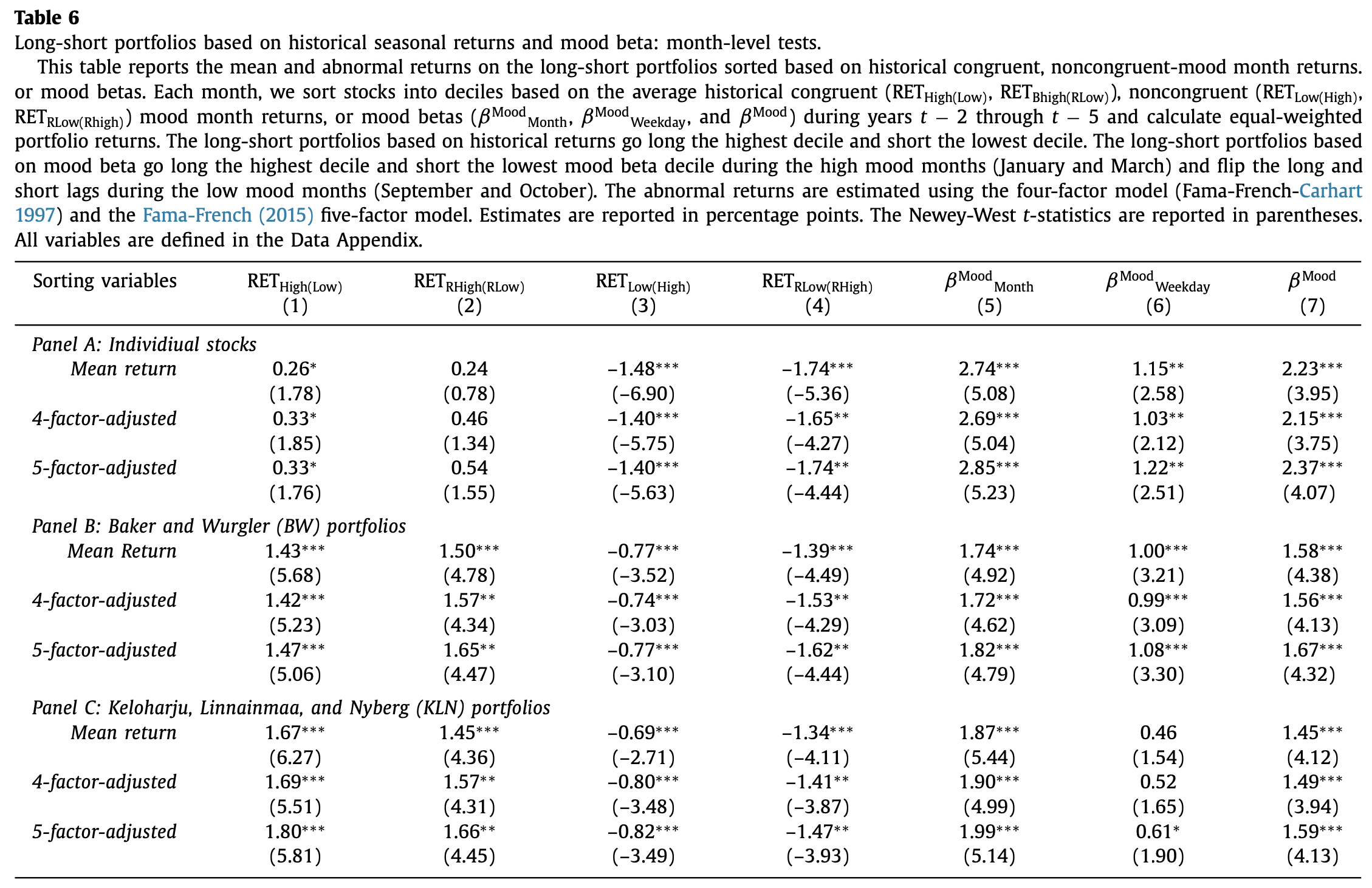

Key Table or Figure from the Paper

📌 Explanation:

- Shows monthly strategies using mood beta outperform those based on historical seasonal returns

- Composite mood beta portfolio earns 2.37% monthly alpha for individual stocks

- Alphas are stronger and more consistent than those from market or sentiment beta-based portfolios

Final Thought

💡 Mood beta captures real, recurring behavioral inefficiencies that can be turned into consistent alpha. 🚀

Paper Details (For Further Reading)

- Title: Mood Beta and Seasonalities in Stock Returns

- Authors: David Hirshleifer, Danling Jiang, Yuting Meng DiGiovanni

- Publication Year: 2020

- Journal/Source: Journal of Financial Economics

- Link: https://doi.org/10.1016/j.jfineco.2020.02.003