Key Performance Metrics

- Sharpe Ratio (Betting Against Winners - BAW): 1.12

- Monthly Alpha (FF3 + MOM + IVOL): 2.30%

- BAW Monthly Excess Return: 2.41%

- Return of Overpriced Winners Portfolio: -1.47%/month

- Persistence: Negative returns persist for 4+ years

💡 Takeaway:

High short interest and low institutional ownership among momentum winners are red flags. These stocks tend to crash as excessive optimism fades and disagreement resolves.

Key Idea: What Is This Paper About?

The paper identifies a subgroup of “momentum winners” that are actually overpriced due to investor over-optimism. These stocks have high past returns but are hard to short (low institutional ownership) and attract increasing short interest. This triad signals future underperformance, contrary to standard momentum expectations.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limits to Arbitrage: Short-sale constraints prevent rational investors from correcting mispricing.

- Disagreement & Sentiment: Optimists drive up prices in the absence of shorting pressure; prices reverse as beliefs converge.

- Earnings Resolution: Much of the negative returns occurs around earnings announcements, where disagreement resolves.

- Supply/Demand in Lending Market: Short-sale cost increases when institutional lending is scarce (low IO).

📌 Why It Matters:

Not all high-momentum stocks are good buys. Some are sentiment-driven bubbles. A deeper look into market microstructure (short interest + IO) helps avoid the trap.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Returns & Market Cap: CRSP

- Book Equity & Fundamentals: Compustat

- Short Interest: Exchange data (pre-2003) + Compustat (post-2003)

- Institutional Ownership (IO): Thomson Reuters 13F

- Earnings Forecast Dispersion: IBES

- Time Period: 1989–2016

Model / Methodology

- Sort stocks into “momentum winners” based on 12-month past returns (excluding the most recent month)

- Within winners, identify stocks:

- With high increase in short interest (top 20%)

- And low institutional ownership (bottom 20%)

- These are labeled Overpriced Winners

- Compare them to other winners, build Betting Against Winners (BAW) strategy:

- Long: Other winners

- Short: Overpriced winners

Trading Strategy (BAW)

- Signal Generation: High momentum + high ∆short interest + low IO

- Portfolio Construction: Value-weighted, monthly rebalanced

- Hedging: Market neutral (Mkt-RF, SMB, HML)

- Execution Enhancements:

- Monitor earnings calendar (most crashes occur near earnings)

- Use put-call parity deviation or SIRIO as short cost proxy

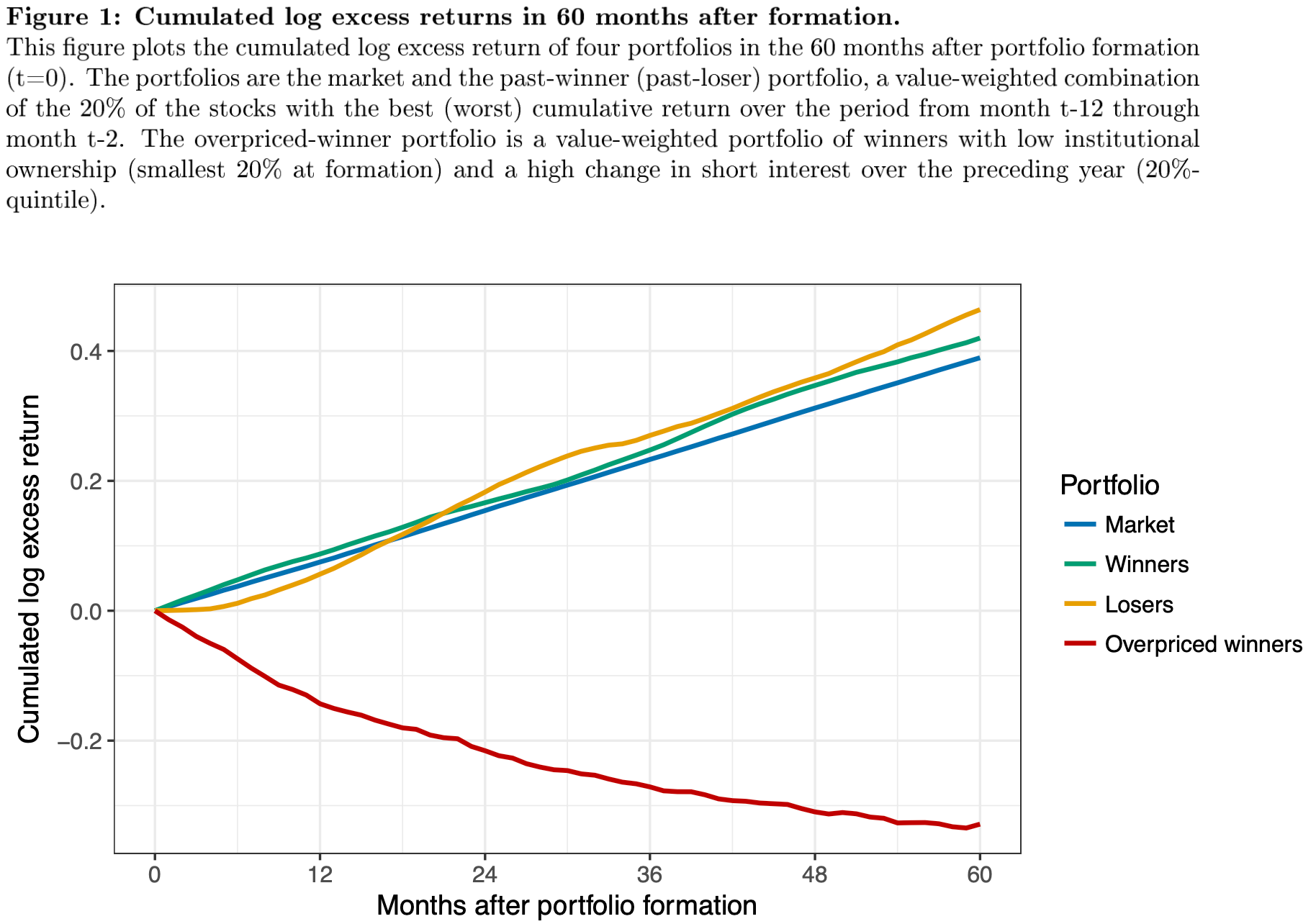

Key Table or Figure from the Paper

📌 Explanation:

- Overpriced winners outperform before portfolio formation (momentum effect), but underperform dramatically after.

- 5-year cumulative underperformance wipes out all prior gains.

- Confirms that their strong past performance was driven by mispricing, not fundamentals.

Final Thought

💡 Not all winners win—some are just overpriced hype waiting to crash. 🚀

Paper Details (For Further Reading)

- Title: Overpriced Winners

- Authors: Kent Daniel, Alexander Klos, Simon Rottke

- Publication Year: 2017

- Journal/Source: Working Paper

- Link: https://ssrn.com/abstract=2939174