💡 Takeaway:

News momentum is strong and persistent. Trading on recent firm-specific news generates robust profits, especially using high-frequency data.

Key Idea: What Is This Paper About?

The paper decomposes daily returns into news-driven and non-news-driven components using 15-minute and overnight returns. It finds a strong, persistent drift following firm-specific news, consistent with underreaction. A simple trading strategy buying firms with high news returns and shorting those with low news returns generates abnormally high returns.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Investor Inattention: When attention is distracted (e.g., Fridays, macro uncertainty), underreaction is stronger.

- Analyst Delays: Analysts adjust forecasts slowly and partially, reinforcing price drifts.

- Sticky Beliefs: Forecast revisions lag news, creating prolonged adjustment.

- Underreaction, Not Overreaction: No reversal even after a year; it's true drift.

📌 Why It Matters:

This evidence challenges the belief in full price efficiency and shows how news-processing frictions and behavioral biases create predictable return patterns.

Data, Model, and Strategy Implementation

Data Used

- Period: 2000–2012 (main), 2013–2019 (out-of-sample)

- News Source: RavenPack (Dow Jones Newswire)

- Returns: Intraday (15-min) + Overnight (from TAQ)

- Other Data: CRSP, Compustat, IBES (analyst forecasts)

Model / Methodology

- Return Decomposition:

- Identify return intervals with firm news

- Define “news return” vs “non-news return”

- Portfolio Construction:

- Each day at 4 p.m., sort by same-day news return

- Long top decile, short bottom decile

- Hold for 1 week with overlapping positions

- Event Study & Regression:

- Cumulative returns by decile

- Fama-MacBeth regressions with controls

- Robustness: mid-quote returns, characteristic-adjusted returns, out-of-sample

Trading Strategy (News Momentum Strategy)

- Signal Generation:

- Use same-day intraday and overnight return triggered by firm news

- Execution:

- Enter trades at 4 p.m. market close

- Hold for 5 days (exit at next week’s close)

- Overlapping rebalance (20% daily turnover)

- Risk & Cost Control:

- Filter by price ($1+ or $5+)

- Estimate trading cost via proportional effective spread (~18–20 bps)

- Return robust after transaction and short-sale costs

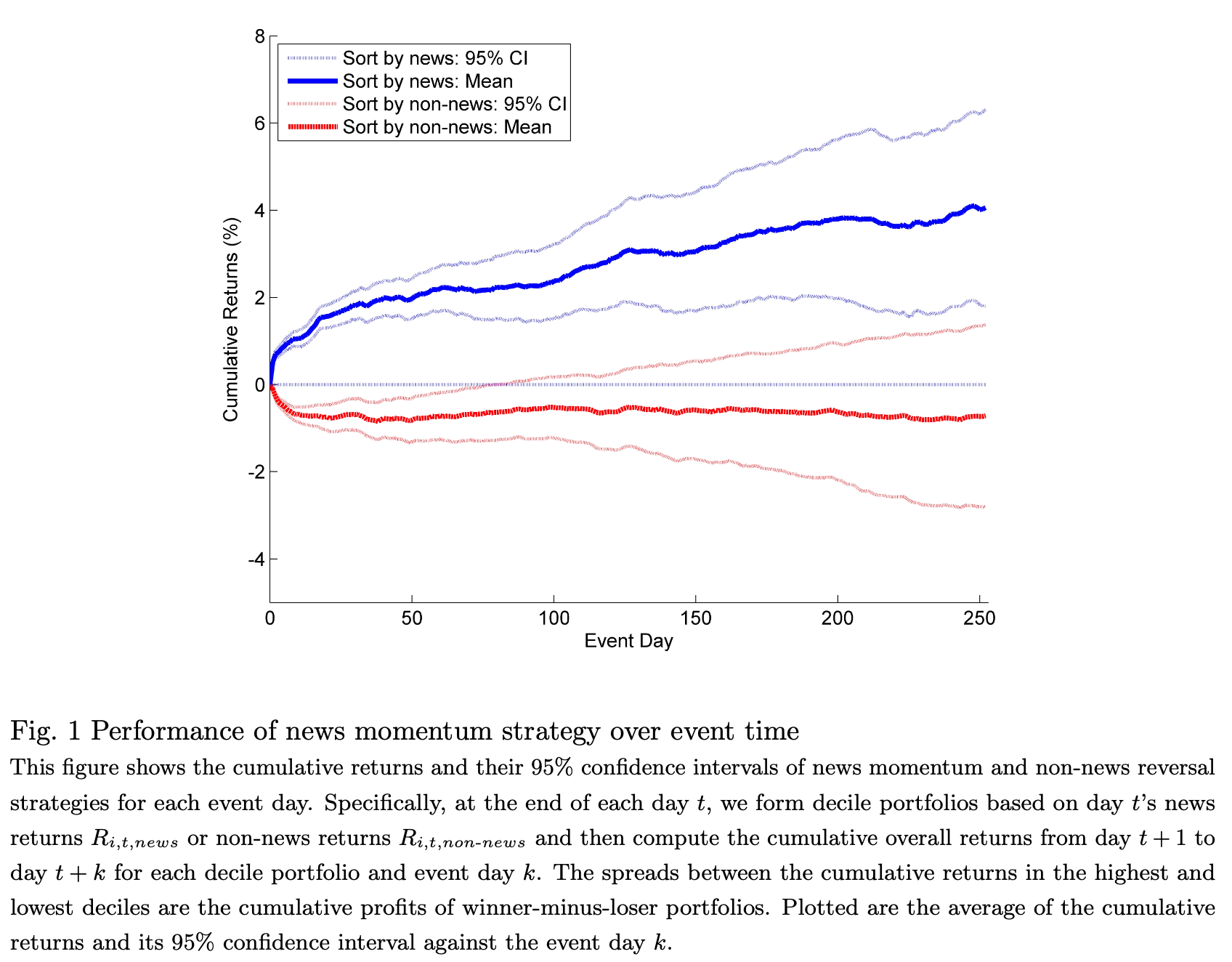

Key Table or Figure from the Paper

📌 Explanation:

- The figure plots cumulative returns of long-short portfolios based on news returns and non-news returns over 252 trading days after portfolio formation.

- The news-based strategy shows a clear and consistent upward drift with no reversal for over a year, highlighting sustained underreaction.

- In contrast, the non-news-based strategy quickly reverses, confirming the pattern is unique to firm-specific news.

- The return spread between top and bottom decile portfolios persists and grows over time—solid visual evidence of the news momentum effect.

Final Thought

💡 The market reads headlines—but not fast enough. High-frequency news creates a durable alpha. 🚀

Paper Details (For Further Reading)

- Title: Pervasive Underreaction: Evidence from High-Frequency Data

- Authors: Hao Jiang, Sophia Zhengzi Li, Hao Wang

- Publication Year: 2020

- Journal/Source: Journal of Financial Economics

- Link: https://ssrn.com/abstract=2679614