Performance

- Industrial production growth and inflation are the most consistent predictors of commodity returns.

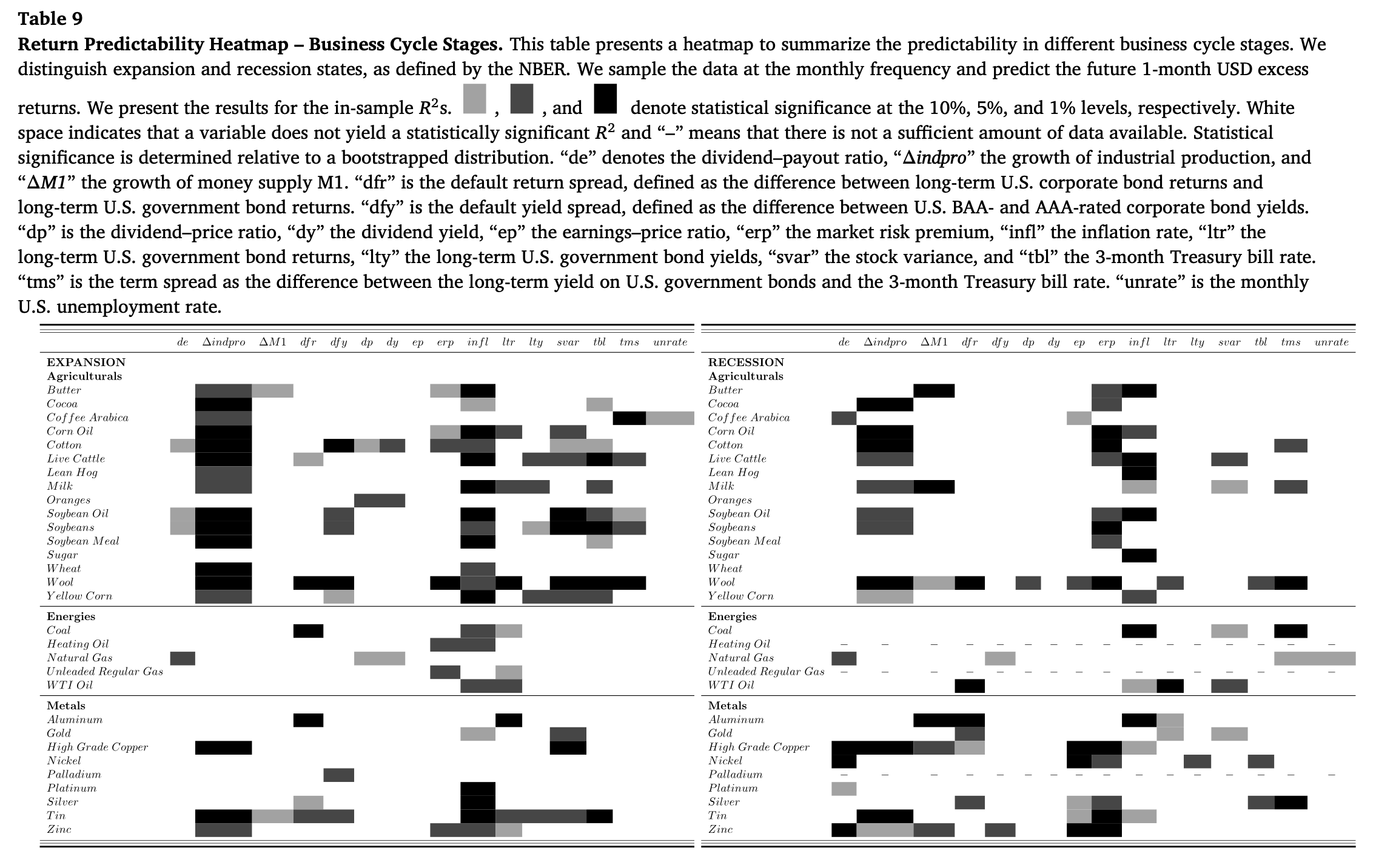

- Predictability is stronger in expansions than in recessions.

- Futures introduction reduces predictability in some markets but increases it in others.

- Commodity volatilities tend to rise after futures introduction and during crises.

Key Idea

This paper examines more than 140 years of commodity market data and finds that macroeconomic variables predict commodity returns and volatilities. Industrial production and inflation provide the strongest signals. The introduction of derivatives makes markets more efficient in some cases, but shifts price discovery to derivatives markets in others.

Economic Rationale

- Macroeconomic Drivers: Commodities are deeply linked to the business cycle, as demand changes in response to economic growth and inflationary pressures.

- Market Efficiency and Derivatives: Futures markets improve efficiency but may also alter return dynamics as price discovery moves away from spot markets.

- Predictability and Risk Premia: Returns and volatilities are more predictable after crises, possibly due to risk premia adjustments.

Practical Applications

- Macroeconomic-Based Trading: Use industrial production and inflation to time commodity investments.

- Volatility Strategies: Expect higher volatility after futures introductions and during crisis periods.

- Cross-Market Signals: Stock market returns predict commodity returns with a 1-month lag, especially in recessions.

- Business Cycle Awareness: Predictability is higher in expansions, suggesting timing strategies can be sector-specific.

How to Do It

Data

- 140+ years of commodity prices from Global Financial Database (1871-2015).

- Macroeconomic predictors: Industrial production, money supply, inflation, unemployment, interest rates.

- Equity-related factors: Dividend yields, earnings-price ratios, market risk premium.

Model/Methodology

- Fama-MacBeth regressions to assess return predictability.

- AR(1) models for volatility forecasting.

- Long-short portfolios based on macroeconomic signals.

- Structural break analysis to evaluate changes due to derivatives trading and financial crises.

Strategy

- Momentum Effect: Use equity market returns to predict commodity returns in recessions.

- Inflation Hedge: Favor commodities during rising inflation periods.

- Volatility Arbitrage: Expect higher volatility in post-crisis environments and after futures introductions.

Table or Figure

- Industrial production and inflation predict returns consistently across cycles.

- Stock market returns predict commodities more strongly in recessions.

- Predictability is generally stronger in expansions.

Paper Details

- Authors: Fabian Hollstein, Marcel Prokopczuk, Björn Tharann, Chardin Wese Simen

- Published: 2021

- Source: Journal of Commodity Markets

- DOI: 10.1016/j.jcomm.2021.100171