Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Sharpe Ratio (Equal-Weighted L/S): 4.29

- Average Daily Return (L/S): 33 bps

- Risk-Adjusted Alpha (FF5+MOM): 4.3% per day (EW L/S)

- Outperformance vs RavenPack: SESTM earns 33 bps vs 18 bps/day

💡 Takeaway:

SESTM delivers strong predictive power and out-of-sample alpha. It outperforms both RavenPack and dictionary-based methods while using a transparent, white-box ML approach.

Key Idea: What Is This Paper About?

The paper introduces SESTM (Sentiment Extraction via Screening and Topic Modeling), a three-step supervised learning model to extract predictive sentiment from financial news. Instead of relying on pre-built dictionaries, SESTM learns which words matter for future returns and assigns them custom weights. It shows this model yields better predictions and more profitable trading strategies.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limited Attention: Investors process news with delay, especially for small or volatile stocks.

- Textual Complexity & Novelty: Fresh news and complex sentiment signals are assimilated into prices more slowly.

- Information Frictions: Differences in speed of assimilation suggest inefficiencies that can be exploited.

📌 Why It Matters:

SESTM shows how tailored sentiment extraction reveals information traditional methods miss, enabling consistent alpha generation using public news.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- News Source: Dow Jones Newswires (1989–2017)

- Price Data: CRSP, TAQ

- Training Sample: 1989–2012

- Out-of-Sample: 2004–2017

- Articles Processed: ~6.5 million single-stock articles

Model / Methodology

- Screening: Select sentiment-charged words using correlation with return direction.

- Topic Modeling: Assign word weights based on predictive ability using supervised topic modeling.

- Scoring: Aggregate to article-level sentiment with penalized likelihood.

- Key Tuning: Optimized using cross-validation on 5-year rolling windows.

- Portfolio Construction:

- Long top 50 sentiment stocks

- Short bottom 50

- Rebalanced daily, open-to-open returns

Trading Strategy (SESTM Long-Short)

- Weighting Schemes: Equal-weighted (preferred), and value-weighted

- Holding Period: 1 day (can be extended with decay-weighting)

- Transaction Costs: Handled via turnover-constrained variants (EWCT strategy)

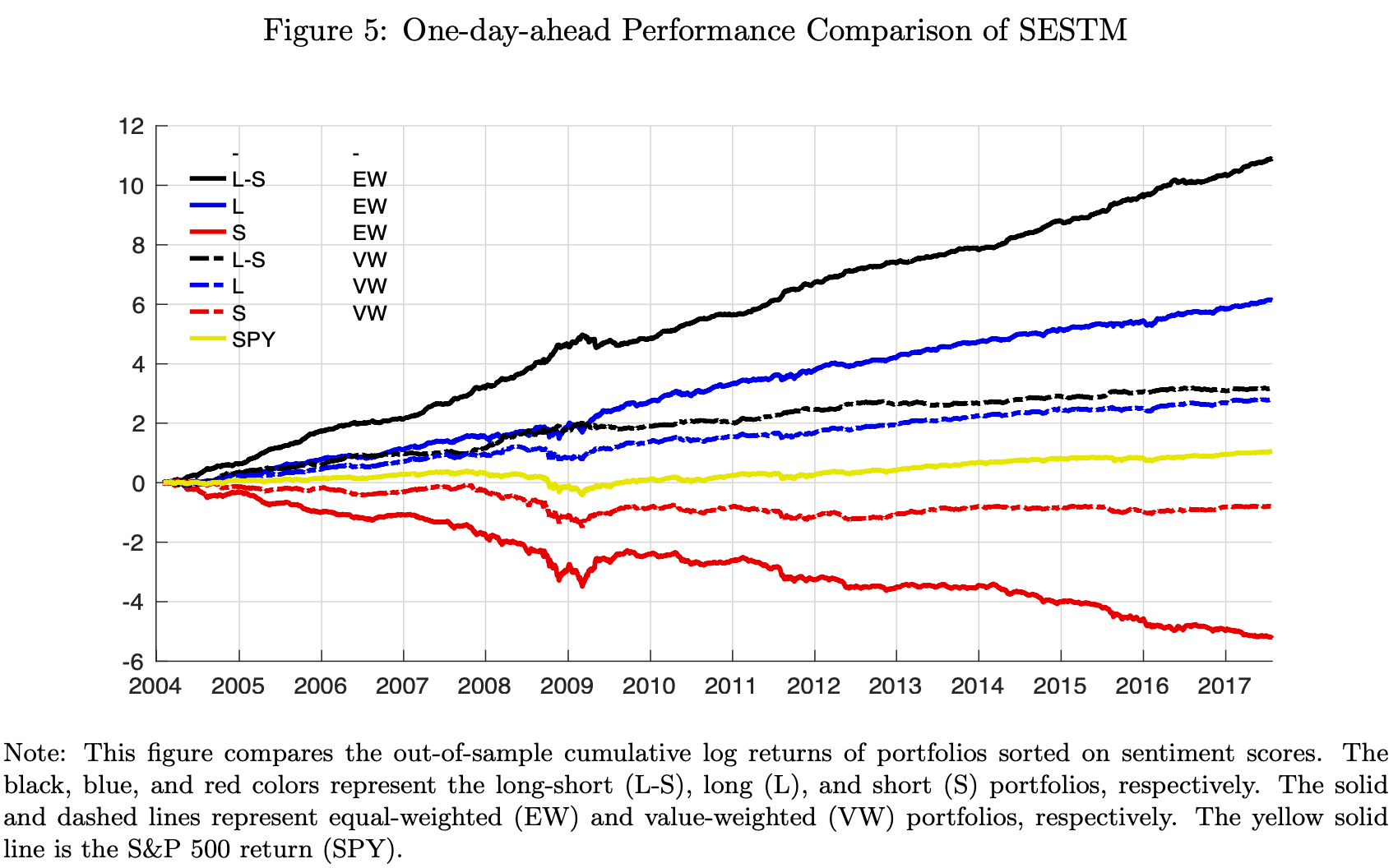

Key Table or Figure from the Paper

📌 Explanation:

- Shows performance of equal- and value-weighted long, short, and long-short portfolios using SESTM sentiment.

- The equal-weighted long-short portfolio consistently outperforms S&P 500 (SPY), including during crises.

- The strategy generates pure alpha: over 90% of return not explained by FF5+MOM factors.

Final Thought

💡 A machine that reads news and beats the market? SESTM proves it's possible—with transparency and theory to back it up. 🚀

Paper Details (For Further Reading)

- Title: Predicting Returns With Text Data

- Authors: Zheng Tracy Ke, Bryan T. Kelly, Dacheng Xiu

- Publication Year: 2019 (NBER Working Paper 26186)

- Journal/Source: NBER Working Paper

- Link: https://www.nber.org/papers/w26186