Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Pre-FOMC Return: 27.1 bps average per event

- Annualized Return from FOMC Days (1995–2017): 2.24%

- Contribution: ~25% of total annual equity return from ~8 days/year

💡 Takeaway:

A small number of days tied to scheduled macro events explain a large portion of annual equity returns—driven by the resolution of uncertainty.

Key Idea: What Is This Paper About?

The paper solves the “FOMC puzzle”: why does the stock market drift upward before Fed announcements without increased volatility? The answer: investors demand a premium for “heightened uncertainty,” which is slowly resolved as the announcement approaches. The result is outsized returns on those days.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Risk-Return Trade-off, Recast: Uncertainty—not volatility—is priced. Conventional risk measures like VIX or realized volatility fail to capture anticipation risk.

- Information Arrival & Risk Premia: Scheduled macro news triggers uncertainty; the resolution of that uncertainty commands a return.

- Behavioral Finance: Market participants delay action until uncertainty fades, causing predictable drift as announcements near.

📌 Why It Matters:

The findings reframe how we think about risk in macro-sensitive markets and show that standard risk metrics miss critical dimensions of anticipated uncertainty.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Instruments: S&P 500 index and futures, VIX index

- Period: 1986–2018

- Macro Events Tracked: FOMC, Nonfarm Payrolls, GDP, ISM, and unexpected VIX spikes

Model / Methodology

- Event study of pre-announcement windows (4 PM day-before to 5 minutes pre-release)

- Regression of returns on lagged VIX and changes in VIX

- Compare pre-event returns on macro days vs. non-event days

- Use VIX spikes as an out-of-sample test for "heightened uncertainty"

Trading Strategy (Constructed from Insights)

- Signal Generation:

- Long S&P 500 futures from 4 PM before FOMC, GDP, NFP, ISM announcements

- Also go long after large VIX spike days (>3% increase in VIX)

- Execution:

- Hold until just before the announcement or close the next day (for VIX spike days)

- Risk Management:

- Trade small size—these are rare, high-conviction trades (~8 per year)

- Avoid trading during overlapping macro news releases or conflicting signals

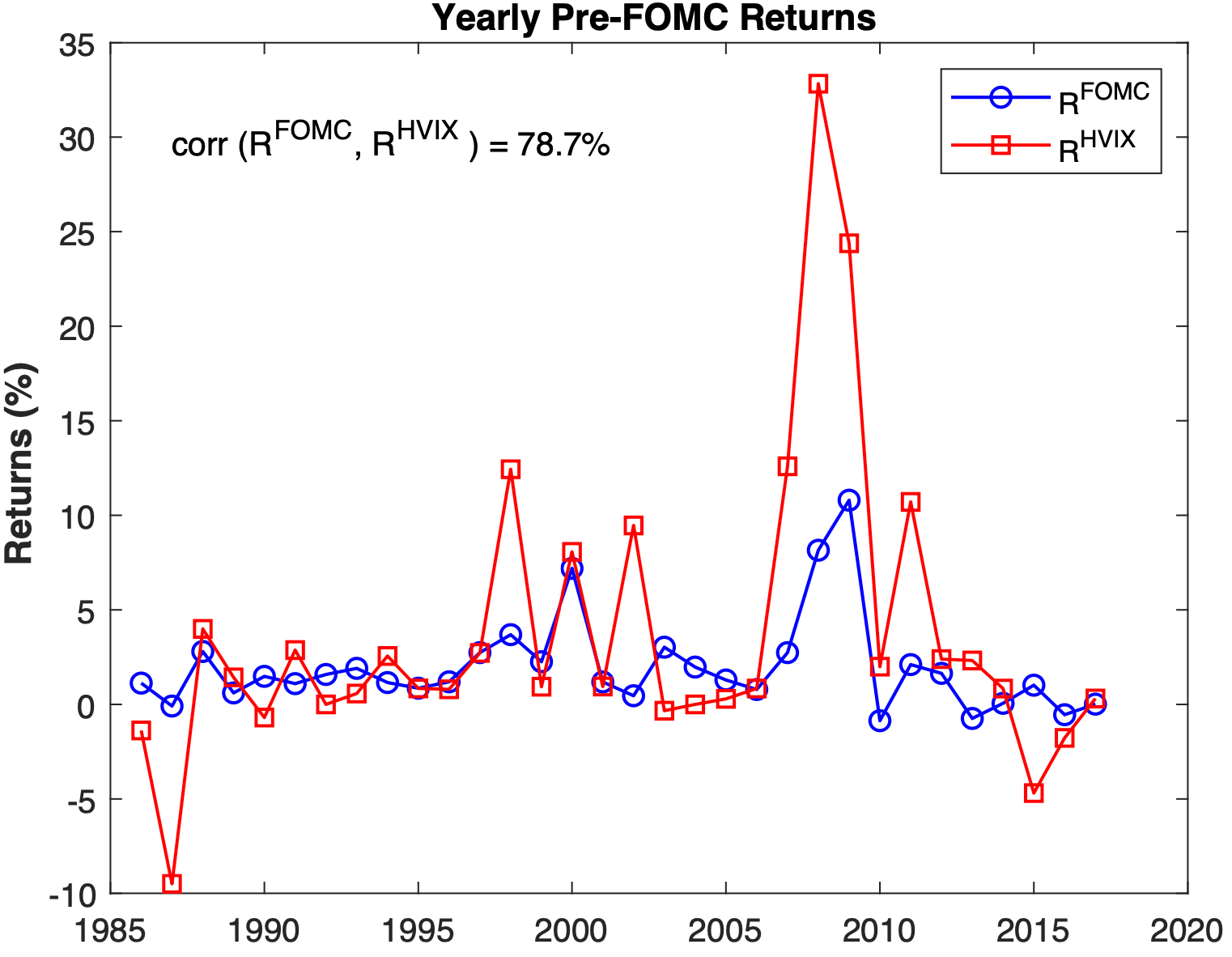

Key Table or Figure from the Paper

📌 Explanation:

- Shows that only 8 days per year (FOMC + HVIX days) deliver over 30% of the annual return.

- HVIX (Heightened VIX) days deliver even more return than FOMC days.

- Highlights clustering of return premiums around macro news—suggesting time-varying, event-specific risk premia.

Final Thought

💡 It’s not volatility, but the anticipation of risk that drives returns. This paper shows how timing macro events reveals the hidden premium of uncertainty. 🚀

Paper Details (For Further Reading)

- Title: Premium for Heightened Uncertainty: Solving the FOMC Puzzle

- Authors: Grace Xing Hu, Jun Pan, Jiang Wang, Haoxiang Zhu

- Publication Year: 2018

- Journal/Source: SSRN Electronic Journal

- Link: https://doi.org/10.2139/ssrn.3282195