💡 Takeaway:

Return predictability—and time-series momentum—is driven by spikes in investor disagreement, which are strongest in recessions and reverse during recoveries.

Key Idea: What Is This Paper About?

The paper develops a model where investors use different forecasting frameworks—some believe in smooth mean-reversion, others in regime shifts. This leads to disagreement, which spikes in bad times. These spikes make returns predictable: they cause underreaction to news (momentum) when pessimistic investors ignore good news. The model matches real data and shows that return momentum is strongest in recessions—and crashes after sharp rallies.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Heterogeneous Beliefs: Some investors react slowly to good news in bad states.

- Countercyclical Uncertainty: Bad times increase pessimism and belief dispersion.

- Risk Premium: Disagreement commands a premium, especially when sentiment is extreme.

- Behavioral Asymmetry: Good news isn't enough to flip pessimistic investors during recessions.

📌 Why It Matters:

This theory bridges behavioral finance and macro models—return anomalies persist due to disagreement dynamics that intensify in bad times.

Data, Model, and Strategy Implementation

Data Used

- Time Period: 1871–2013 (S&P dividends, earnings forecasts)

- Sentiment Proxy: Dispersion in analysts' EPS forecasts (I/B/E/S)

- Returns: S&P 500, macro fundamentals

- NBER Recession Flags: Used to define bad times

Model / Methodology

- Two investor types:

- Agent A: Believes in continuous-state, mean-reverting growth (Ornstein-Uhlenbeck)

- Agent B: Believes in discrete regimes (Markov switching between boom/bust)

- Disagreement = squared distance between forecasts (g²)

- Predictive regressions:

- Future returns ~ Dispersion + Fundamental + Interaction terms

- VAR and impulse response analysis for momentum dynamics

Trading Strategy (Momentum & Macro Overlay)

- Signal Generation:

- Use analyst forecast dispersion as proxy for disagreement

- Strong signal = high dispersion during NBER recessions

- Execution:

- Go long market after positive returns if dispersion is high

- Hold for 1–3 months

- Exit after strong rebounds or improving macro (to avoid crash risk)

- Enhancement:

- Cross asset: Apply to country indices or macro-sensitive sectors

- Crash protection: Reduce exposure during fast rebounds

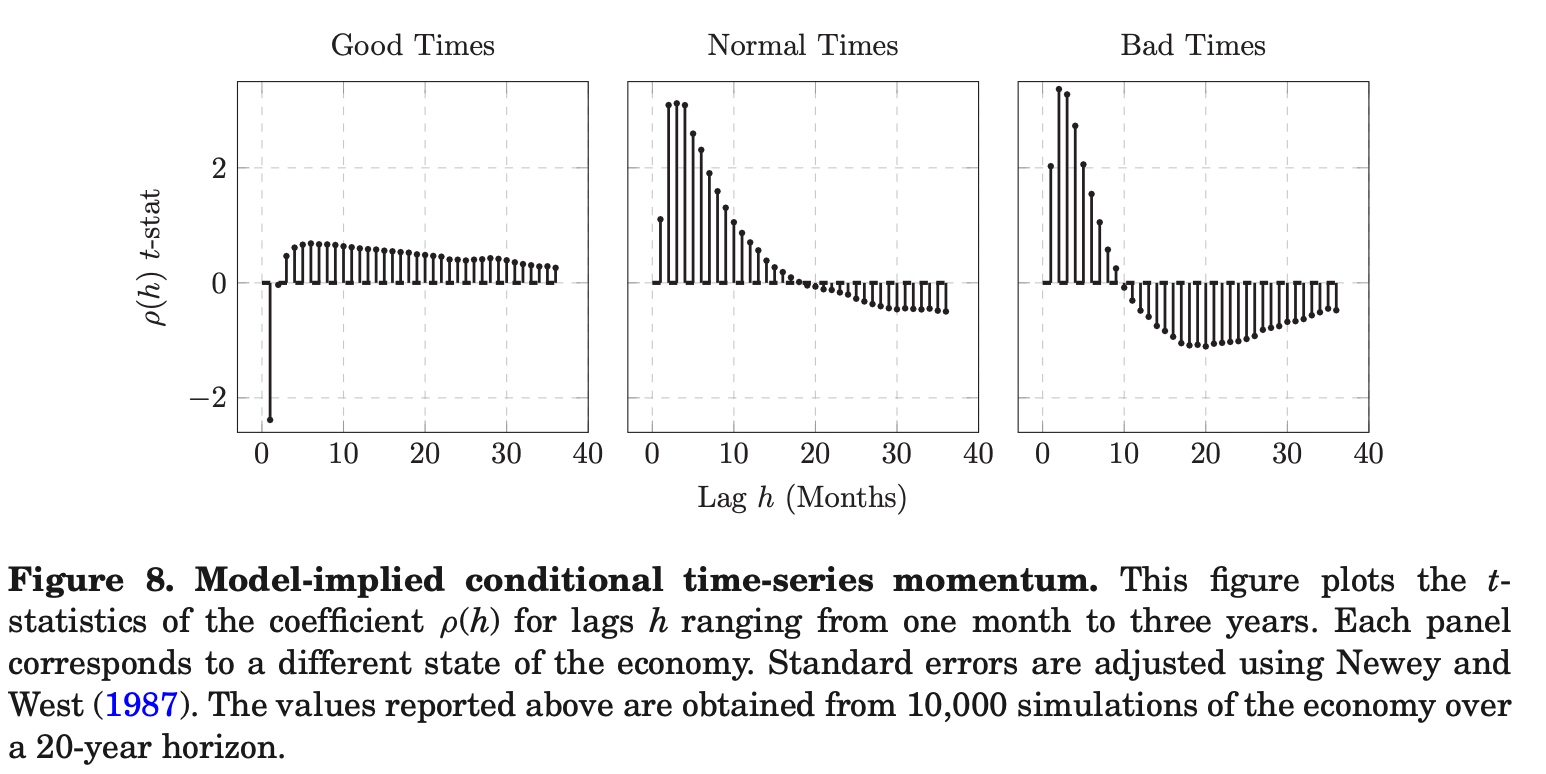

Key Table or Figure from the Paper

📌 Explanation:

- Momentum is strongest in recessions, weaker in normal times, and reverses in good times.

- One-month return autocorrelation is high and significant during NBER recessions.

- Sharp market rebounds lead to momentum crashes, consistent with 2009 data.

Final Thought

💡 Momentum is born from disagreement—and it dies in recoveries. 🚀

Paper Details (For Further Reading)

- Title: Why Does Return Predictability Concentrate in Bad Times?

- Authors: Julien Cujean, Michael Hasler

- Publication Year: 2017

- Journal/Source: Journal of Finance

- Link: https://doi.org/10.1111/jofi.12544