💡 Takeaway:

Return seasonalities are persistent, powerful, and pervasive. Strategies based on past same-calendar-month returns outperform significantly—and this applies across assets and time frequencies.

Key Idea: What Is This Paper About?

This paper reveals a powerful and intuitive anomaly: assets tend to perform well in the same calendar month(s) they have historically outperformed. The authors find this same-month seasonality in individual stocks, anomaly portfolios, country indices, and commodities, and at both monthly and daily frequencies. The strategy remains profitable even after accounting for risk factors and excluding January.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Seasonal Risk Premia: Time-varying risk premia linked to calendar months.

- Persistent Mispricing: Investors may underreact or overreact based on seasonal expectations.

- Behavioral Timing: Window dressing, tax loss harvesting, or sentiment cycles can contribute.

📌 Why It Matters:

This finding unifies seasonal and non-seasonal anomalies, showing that calendar effects amplify or dominate expected returns. It challenges traditional views of anomaly persistence and randomness.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Stocks: NYSE, AMEX, NASDAQ (1963–2011)

- Anomalies: 15 strategies incl. momentum, value, accruals, etc.

- Commodities: 24 futures contracts

- Countries: 15 MSCI country indices

- Returns: Monthly and daily

Model / Methodology

- Core Signal: Historical same-calendar-month return (20-year rolling window)

- Strategy Type: Long top-decile, short bottom-decile (based on same-month average)

- Control Sorts: Compared to other-month returns

- Tests: Fama-MacBeth regressions, time-series alphas, subperiod and asset-class robustness

Trading Strategy (Practical Approach)

- Stock-Level:

- Rank stocks on average same-month returns over past 20 years

- Go long top decile, short bottom

- Rebalance monthly

- Portfolio-Level:

- Apply same logic to industry, size, dividend, momentum, etc. portfolios

- Also works at anomaly, country, and commodity level

- Enhancements:

- Works even without January

- Outperforms random long-short strategies in volatility and alpha

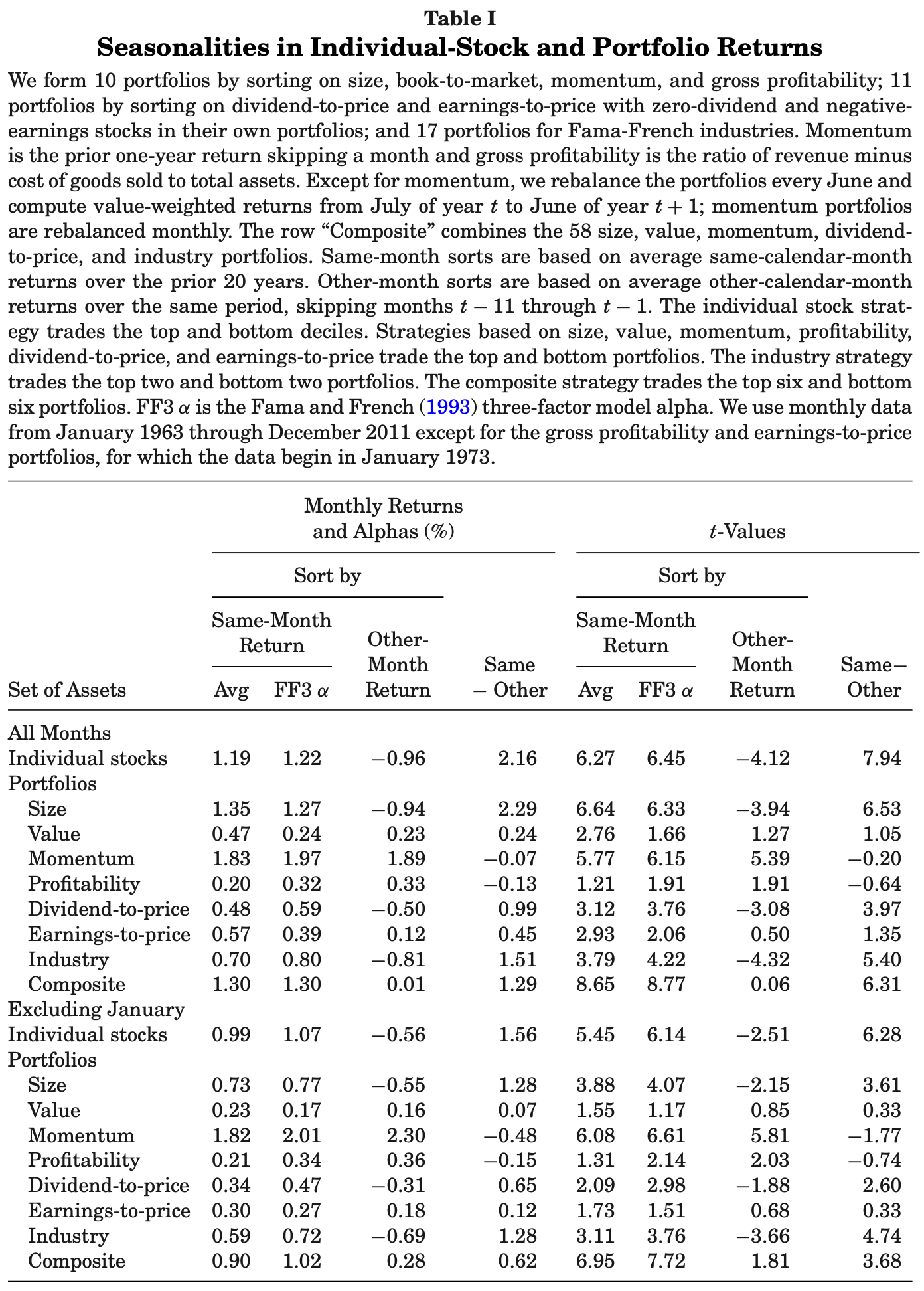

Key Table or Figure from the Paper

📌 Explanation:

- Shows that same-calendar-month strategies earn 1.19–1.83%/month across various portfolios

- Strategies based on other months underperform or even lose money

- Composite strategy earns 1.30%/month with a Sharpe higher than traditional momentum or size strategies

Final Thought

💡 Your best trades might depend more on the calendar than you think. 🚀

Paper Details (For Further Reading)

- Title: Return Seasonalities

- Authors: Matti Keloharju, Juhani T. Linnainmaa, Peter Nyberg

- Publication Year: 2016

- Journal/Source: Journal of Finance

- Link: https://doi.org/10.1111/jofi.12398