💡 Takeaway:

Short-selling risk—especially the variance of future loan fees—is a strong return predictor and source of persistent mispricing. It’s a true limit to arbitrage, particularly when trades require long horizons.

Key Idea: What Is This Paper About?

This paper introduces and tests a dynamic measure of short-selling risk based on the forecasted variance of equity loan fees. Unlike static proxies (like current borrow fees), this forward-looking risk constrains arbitrage and limits short-seller participation. Stocks with higher short-selling risk have lower returns, higher pricing errors, and lower trading volume, even after controlling for short interest. The effect is stronger when trades take longer to resolve.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limits to Arbitrage (Shleifer & Vishny, 1997): Risk of being bought in or facing fee spikes deters arbitrage.

- Loan Recall and Fee Volatility: Borrow costs change unexpectedly, eroding profits.

- Holding Horizon Risk: Mispricing that requires long horizons is especially unattractive to short sellers.

- Price Efficiency Impairment: Higher short-selling risk leads to slower information incorporation.

📌 Why It Matters:

Explains why short interest remains a strong return predictor despite being public—because many can’t or won’t act on it due to dynamic borrowing risks.

Data, Model, and Strategy Implementation

Data Used

- Period: July 2006 – Dec 2011

- Equity Lending Data: Markit

- Market Data: CRSP, Compustat, OptionMetrics, TAQ

- Options Data: Used for put-call parity tests

- Sample Size: 220,000 firm-months, ~4,500 US stocks

Model / Methodology

- ShortRisk: Forecasted variance of loan fees using lagged lending + firm data

- Forecasting Inputs:

- Variance of new loan fees and utilization

- Tail risk proxies (99th percentile)

- Fails-to-deliver, IPO flag, option presence, volatility

- Portfolio Sorts: Quintiles on ShortRisk

- Tests:

- Fama-MacBeth regressions

- Five-factor alphas

- Price delay (Hou & Moskowitz, 2005)

- Put-call parity arbitrage (long horizon test)

Trading Strategy (From ShortRisk Signal)

- Long: Low ShortRisk stocks (more liquid to short)

- Short: High ShortRisk stocks (costlier/riskier to short)

- Rebalancing: Monthly

- Filters: Can overlay with short interest, size, or mispricing signals

- Enhancement: Focus on Micro/Small caps and long-horizon mispricings (e.g., put-call parity deviations)

Key Table or Figure from the Paper

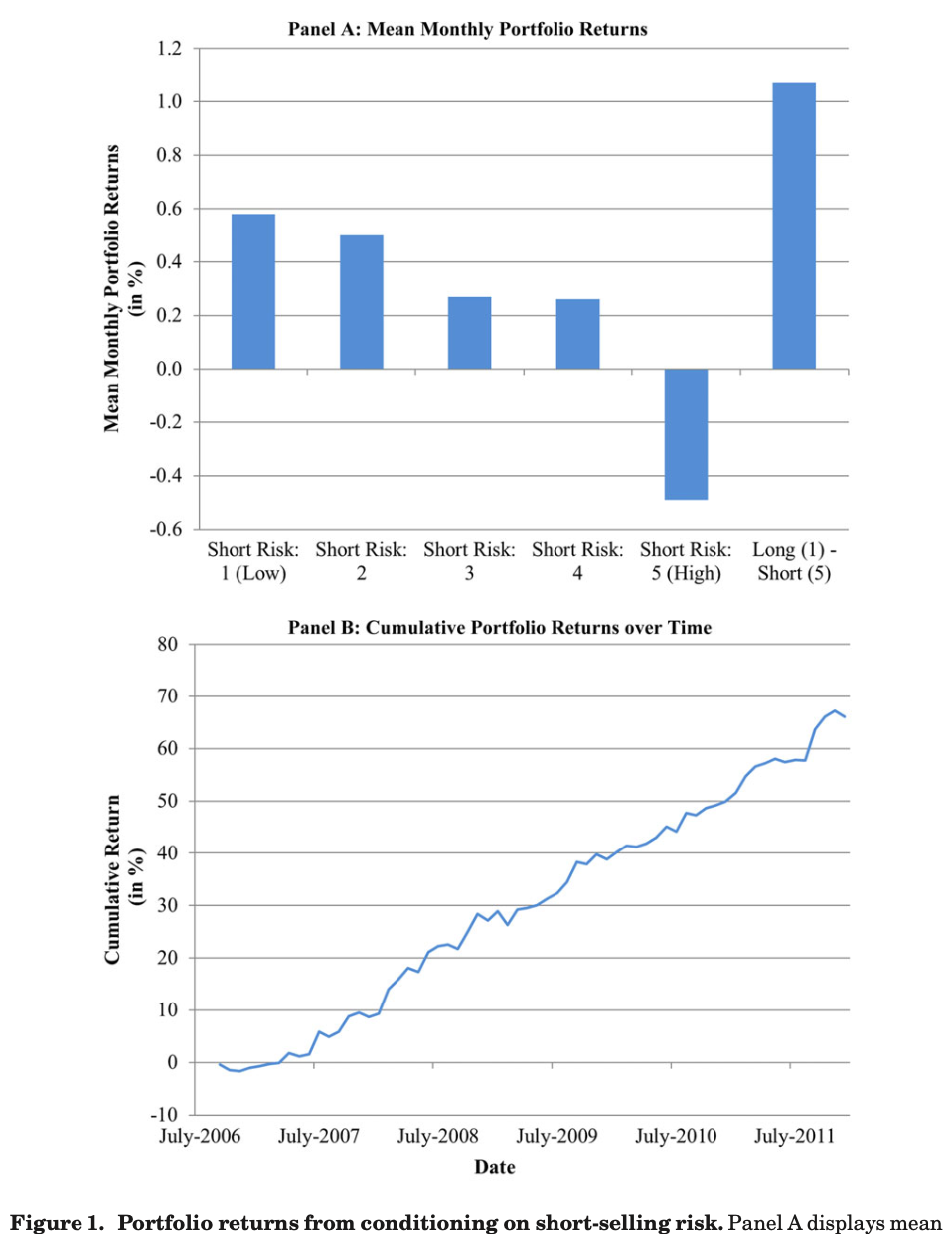

📊 Reference: [Figure 1] – Long-Short Portfolio Returns by Short-Selling Risk

📌 Explanation:

- Shows monthly and cumulative returns to a strategy that buys low ShortRisk stocks and shorts high ShortRisk ones.

- Annualized alpha: 9.6%

- FF5-adjusted alpha: 0.80%/month

- Effect is not subsumed by short interest

- Impact is strongest for small caps and long-duration arbitrage setups

Final Thought

💡 Short-selling risk is the friction that keeps mispricing alive—even when it’s visible to all. 🔍📉

Paper Details (For Further Reading)

- Title: Short-Selling Risk

- Authors: Joseph Engelberg, Adam Reed, Matthew Ringgenberg

- Publication Year: 2018

- Journal/Source: Journal of Finance

- Link: https://doi.org/10.1111/jofi.12601