Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Top HFT Daily Revenue: SEK 61,000+

- Median Sharpe Ratio: 1.61

- Top Sharpe Ratio: 11.14

- Latency Edge: Fastest firms earn ~5x more than slower peers

💡 Takeaway:

Speed is the key differentiator. Being milliseconds faster means you get more trades—without taking more risk. The return advantage comes from quantity, not quality.

Key Idea: What Is This Paper About?

The paper studies why some HFT firms earn more than others. It finds that small differences in latency (reaction speed) cause large gaps in performance. Faster firms get more trades (volume), not necessarily better trades, and dominate profits. The benefits of speed apply across strategies: market making, arbitrage, and momentum.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Relative Latency Models: Fastest firms capture entire trading opportunities before others arrive.

- Risk Management Advantage: Fast HFTs cancel bad quotes quicker, avoiding adverse selection.

- Arms Race Theory (Budish et al., 2015): Speed upgrades perpetuate dominance, reinforcing concentration.

- Trade Execution Timing: HFTs react faster to stale quotes, market events, and cross-venue price changes.

📌 Why It Matters:

Confirms that HFT profitability comes not just from skill or signal, but also from infrastructure. Regulatory focus on latency races is justified.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Source: Swedish market data from Finansinspektionen

- Period: 2010–2014

- Assets: 25 most liquid Swedish equities across all trading venues

- Unique Feature: Firm-level identifiers for HFT classification

Model / Methodology

- Latency Measure: Time from passive fill to aggressive reaction (DECISION_LATENCY)

- Performance Metrics: Revenues, returns, Sharpe ratio, alpha, spread capture

- Strategy Breakdown:

- Risk-adjusted market making (passive realized spread)

- Short-lived info trading (price impact from aggressive trades)

- Cross-market arbitrage (equity trades following futures moves)

- Causal Evidence: Two colocation upgrades used as natural experiments

Trading Strategy (Insights Derived)

- If you’re fast enough:

- Place “test” passive orders to signal flow

- React with aggressive trades on signal fill

- Use speed to cancel stale quotes and avoid toxic flow

- If you’re slower:

- Focus on longer holding strategies or trade less contested instruments

- Avoid competing in ultra-short-term latency games

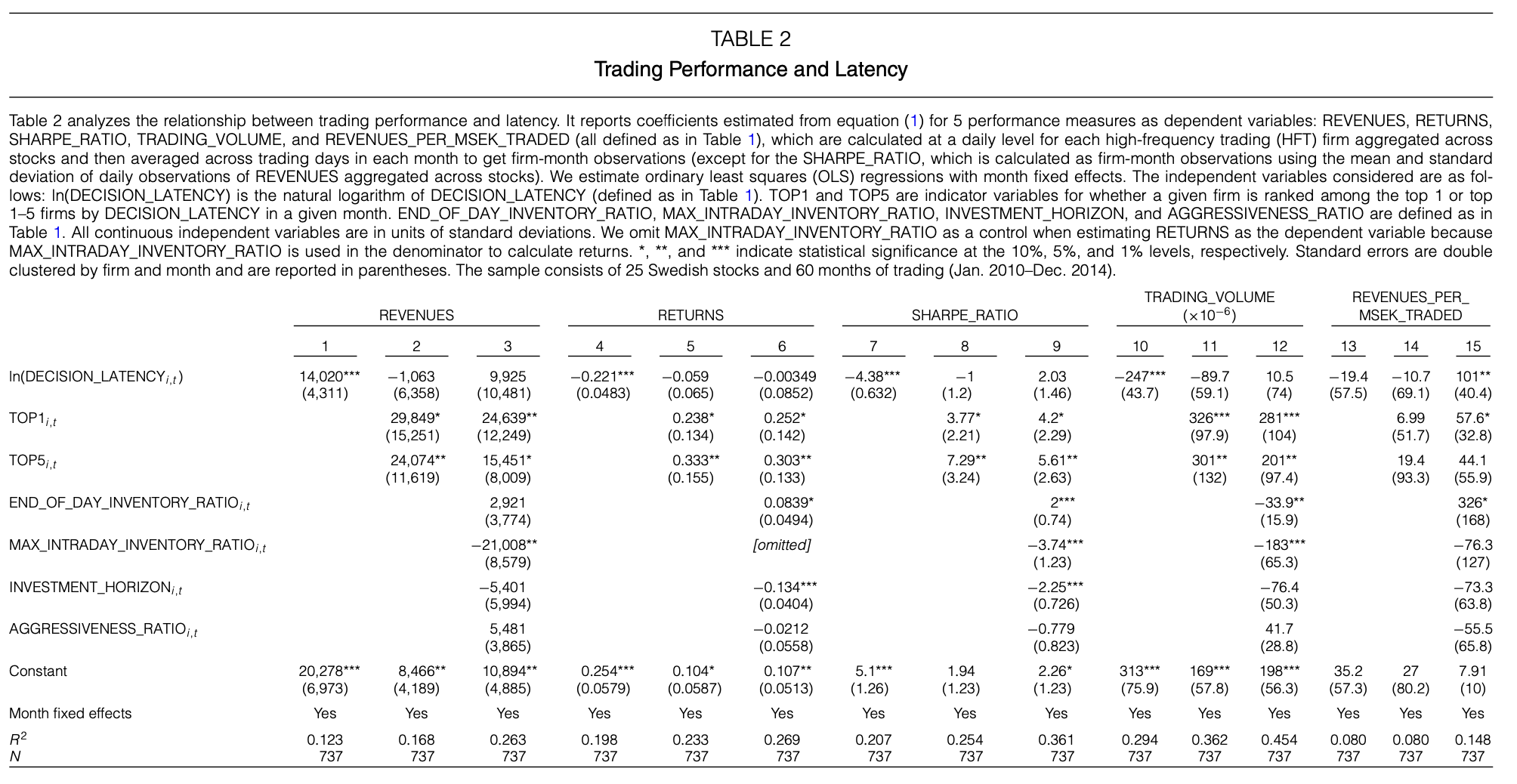

Key Table or Figure from the Paper

📌 Explanation:

- Being among the 5 fastest HFTs increases revenues by SEK 15,000/day

- Being the fastest adds ~SEK 25,000 more

- Fast firms don’t have better per-trade returns—but get more trades

- Strong monotonic relationship: lower latency = more money

Final Thought

💡 In HFT, you don’t have to be good—you just have to be faster than the other guy.

🚀

Paper Details (For Further Reading)

- Title: Risk and Return in High-Frequency Trading

- Authors: Matthew Baron, Jonathan Brogaard, Björn Hagströmer, Andrei Kirilenko

- Publication Year: 2019

- Journal/Source: Journal of Financial and Quantitative Analysis

- Link: https://doi.org/10.1017/S0022109018001096