💡 Takeaway:

HFTs dominate profitable trading opportunities using speed, leaving slower traders disadvantaged—especially retail ones.

Key Idea: What Is This Paper About?

This paper analyzes how high-frequency trading (HFT) affects slower limit order traders using granular order book data. It finds that HFTs exploit fleeting information in depth imbalances to anticipate price moves, place orders on the "right" side, and cancel quickly when signals fade—leaving slower traders with adverse selection risk.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Queue Competition Theory (Li et al., 2021): Speed matters most when tick sizes are binding—HFTs gain execution priority.

- Adverse Selection Models (Hoffmann, 2014): Faster traders avoid bad trades, slower ones can't.

- Order Flow Anticipation (Yang & Zhu, 2019): HFTs piggyback on informed order flow from slower traders.

📌 Why It Matters:

Even if HFT improves short-term price efficiency, it harms the execution quality of institutional and retail traders, potentially discouraging informed participation and long-term market depth.

Data, Model, and Strategy Implementation

Data Used

- Exchange: Australian Securities Exchange (ASX)

- Period: Jan–June 2012 (pre/post ITCH protocol rollout)

- Instruments: Top 100 ASX stocks

- Granularity: Full limit order book with trader type (HFT, institutional, retail)

Model / Methodology

- Track every order submission, cancellation, and trade with broker IDs

- Define favorable fills as trades on the thick side of the order book

- Measure pre/post speed-up impact (ITCH introduction) using difference-in-difference regressions

- Analyze sensitivity to depth imbalance by trader type

Trading Strategy (Derived from Insights)

- Signal Generation:

- Trade with the direction of order book imbalance

- Monitor fleeting depth imbalances (<200 ms)

- Execution Tactics:

- Enter limit orders when imbalance is slightly favorable

- Cancel quickly if imbalance fades

- Advantage:

- Requires co-location or ultra-low latency feeds (e.g., ITCH)

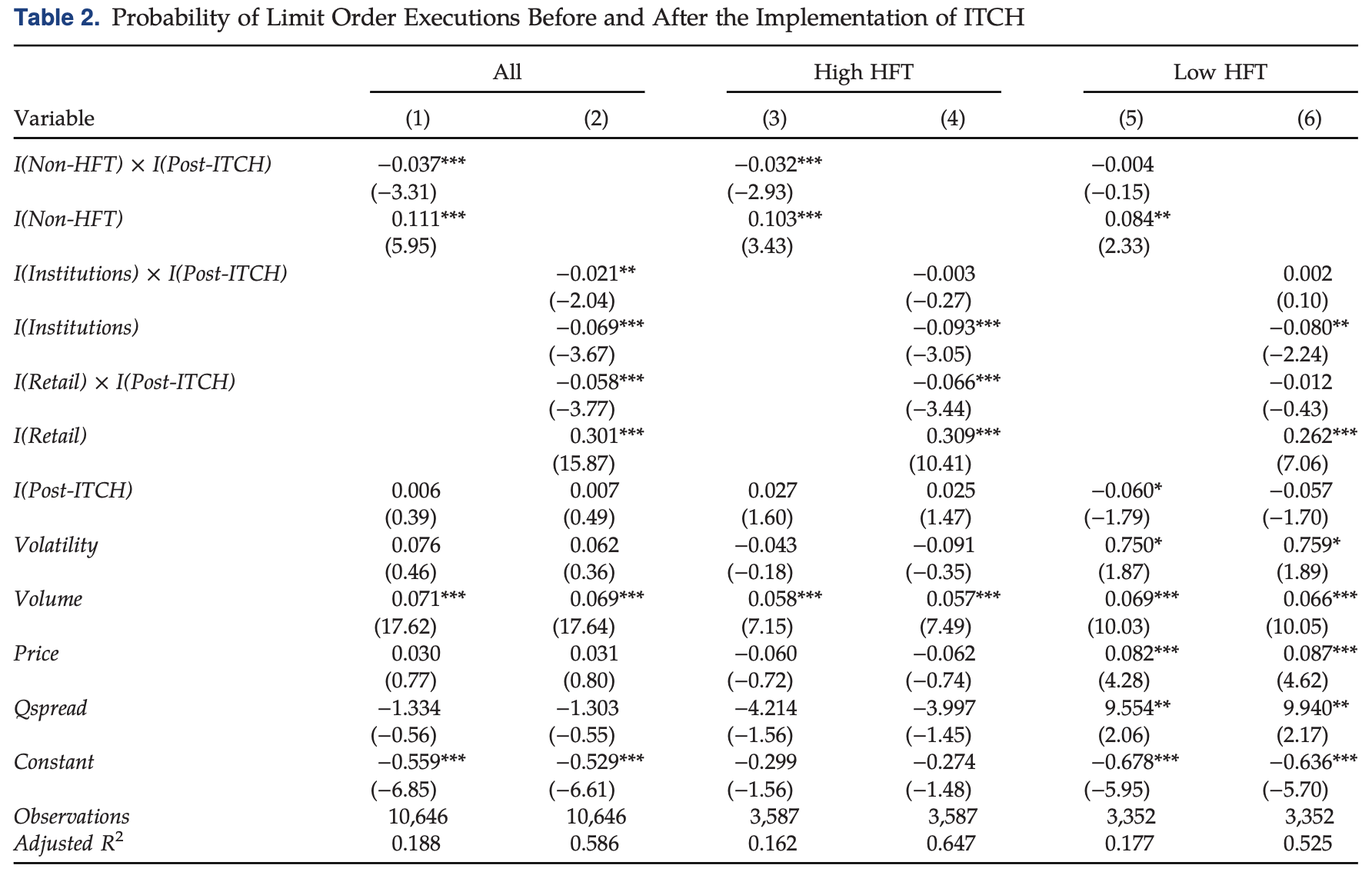

Key Table or Figure from the Paper

📌 Explanation:

- Shows that retail traders' execution probability drops significantly after HFTs gain speed (ITCH upgrade)

- The drop is more severe in tick-constrained and high-volatility stocks

- Retail traders lose out on favorable fills, while HFTs maintain or improve theirs

Final Thought

💡 HFTs aren't just faster—they’re smarter about order book info, and that changes the game for everyone else. 🚀

Paper Details (For Further Reading)

- Title: High-Frequency Trading Strategies

- Authors: Michael Goldstein, Amy Kwan, Richard Philip

- Publication Year: 2023

- Journal/Source: Management Science

- Link: https://doi.org/10.1287/mnsc.2022.4539