Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- 6-Month Return R² (Tail Risk Premium): ~11%

- 1-Year Return R² (Tail Risk Premium): ~13%

- Predictive t-stats for Tail Risk Premium: Often >3.5

- Variance Risk Premium Alone: Much weaker unless decomposed

💡 Takeaway:

Left-tail risk (jump risk) explains most of the predictive power in variance risk premium. It performs better than VIX or traditional volatility metrics.

Key Idea: What Is This Paper About?

Bollerslev et al. (2015) decompose the variance risk premium into two components: one from normal price fluctuations and one from jump tail risk. They find that only the tail component (especially downside jumps) predicts future returns. This shows that markets price fear of rare, severe losses—not just volatility.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Investor Fear Pricing: Rare disasters and downside risk aversion command a premium.

- Risk-Neutral vs Real-World Jump Tails: Option prices embed fear of extreme moves not visible in realized volatility.

- Market Frictions: Jump risk isn’t hedgeable and affects risk-averse investors more than continuous risk.

📌 Why It Matters:

Traditional volatility measures (like VIX) mix diffusive and jump risks. This paper isolates what investors fear most—sudden crashes—and shows it’s the real driver of return predictability.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Sources: OptionMetrics, Tick Data (S&P 500 Futures), CRSP

- Period: Jan 1996 – Aug 2013

- Instruments: S&P 500 options (short-maturity, OTM), realized volatility, returns, dividend-price ratios

Model / Methodology

- Nonparametric estimation of left/right jump tail shapes (α) and levels (ϕ)

- Weekly and monthly decomposition of variance risk premium

- Regression analysis: Predict future returns (1 to 12 months) using:

- Left Jump Variation (LJV)

- VRP – LJV (normal risk)

- VIX² and dividend-price ratios

Trading Strategy (Built from Insights)

- Signal Generation:

- When left-tail jump risk (LJV) is high, expect higher future returns

- Ignore normal variance risk—it adds little

- Portfolio Tilt:

- Overweight market when LJV is high

- Tail-risk premia predict stronger for small caps, value, and momentum portfolios

- Rebalancing Frequency: Monthly

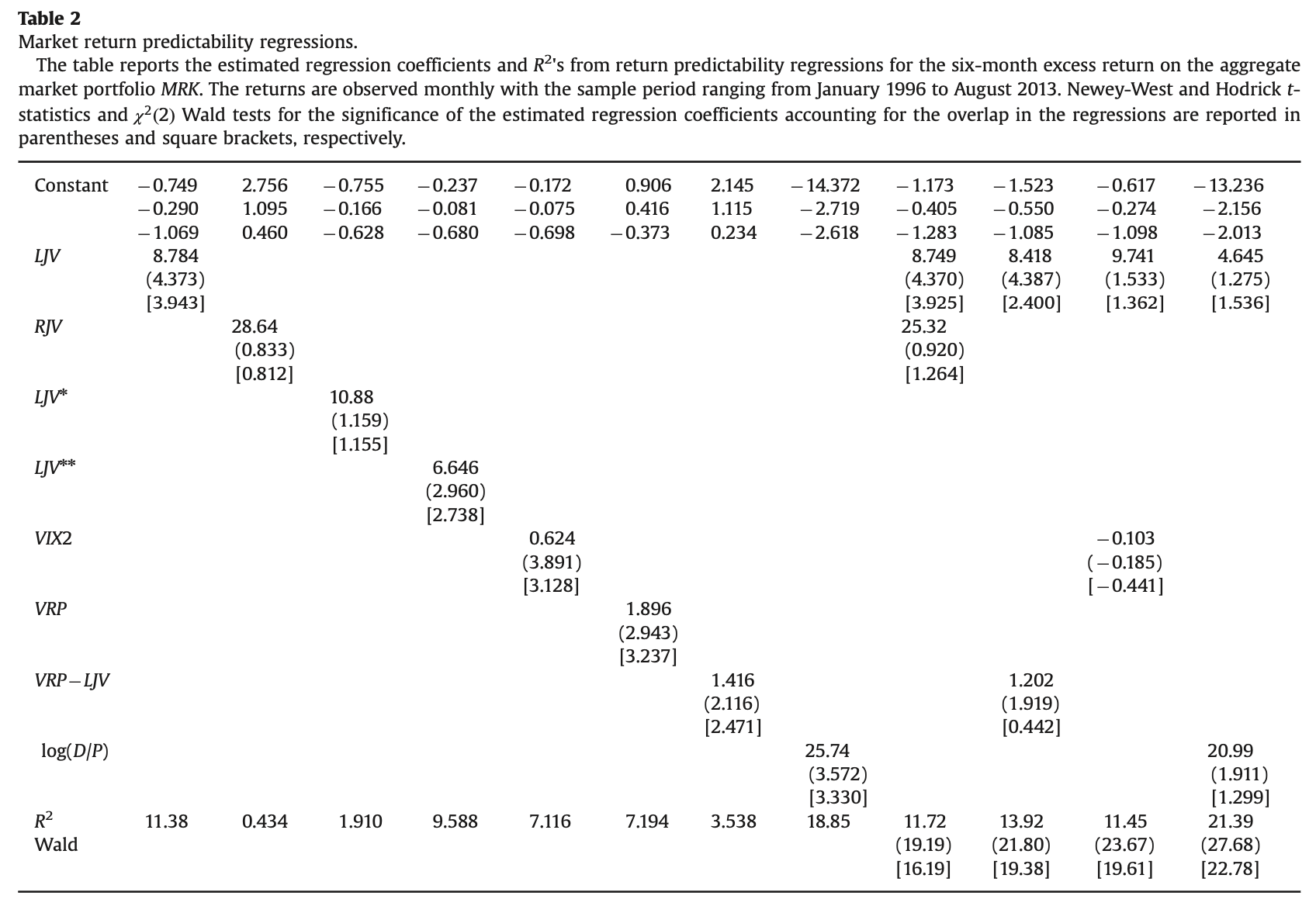

Key Table or Figure from the Paper

📌 Explanation:

- Shows that left jump variation (LJV) has a stronger and more consistent predictive relationship with market returns than the overall variance risk premium or VIX.

- Once you include LJV, the rest of the VRP adds almost nothing—LJV drives the predictability.

Final Thought

💡 Tail risk—not average volatility—is what investors fear, and it’s what predicts future returns. 🚀

Paper Details (For Further Reading)

- Title: Tail Risk Premia and Return Predictability

- Authors: Tim Bollerslev, Viktor Todorov, Lai Xu

- Publication Year: 2015

- Journal/Source: Journal of Financial Economics

- Link: https://doi.org/10.1016/j.jfineco.2015.02.010