💡 Takeaway:

Holding stocks only during even weeks of the FOMC cycle earns superior returns and lower volatility than buy-and-hold. Odd weeks yield negative average returns.

Key Idea: What Is This Paper About?

The paper identifies a novel and powerful anomaly: stock returns follow a biweekly cycle tied to FOMC meetings. Since 1994, the entire equity premium has been earned during weeks 0, 2, 4, and 6 following scheduled FOMC meetings. The effect is linked to monetary policy communication, especially informal leaks and Fed “put” behavior (responding to market stress with accommodation).

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Fed Put: The Fed reacts to market declines with unexpected easing—driving positive stock returns in even weeks.

- Informal Communication Channel: Fed officials leak policy views via trusted journalists and private briefings—impacting markets before official releases.

- Uncertainty Reduction: The Fed lowers downside risk via promises to act, reducing the equity risk premium more than policy rates.

- Behavioral Inertia: Markets fail to fully price this calendar-based effect despite being tied to public information (FOMC calendar).

📌 Why It Matters:

This pattern transforms the equity premium puzzle into a monetary policy communication puzzle and provides a calendar-based trading strategy with strong theoretical and empirical support.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Period: 1994–2016

- Assets: U.S. equities (CRSP), Fed Funds futures, Treasury yields, global MSCI indices

- Fed Data: FOMC calendar, meeting transcripts, Board meetings, Fed speeches

- Returns: Daily and 5-day stock excess returns over T-bills

Model / Methodology

- Define FOMC cycle weeks:

- Week 0: days −1 to +3 relative to FOMC meeting

- Weeks 2, 4, 6: every second week post-meeting

- Regress returns on week dummies

- Test across time, market segments, and global indices

- Analyze Fed activity: intermeeting rate cuts, futures, board meetings, news leaks

- Estimate changes in the equity premium using Martin (2017)’s option-implied bound

Trading Strategy (FOMC Cycle Timing Strategy)

- Signal: Invest in equities during weeks 0, 2, 4, 6 of the FOMC cycle

- Hold Period: 5-day windows each even week

- Execution: Use SPY or S&P 500 futures for clean exposure

- Optional Enhancements:

- Scale exposure based on past week’s negative returns (Fed Put effect)

- Apply globally to MSCI World ex-US and EM indices

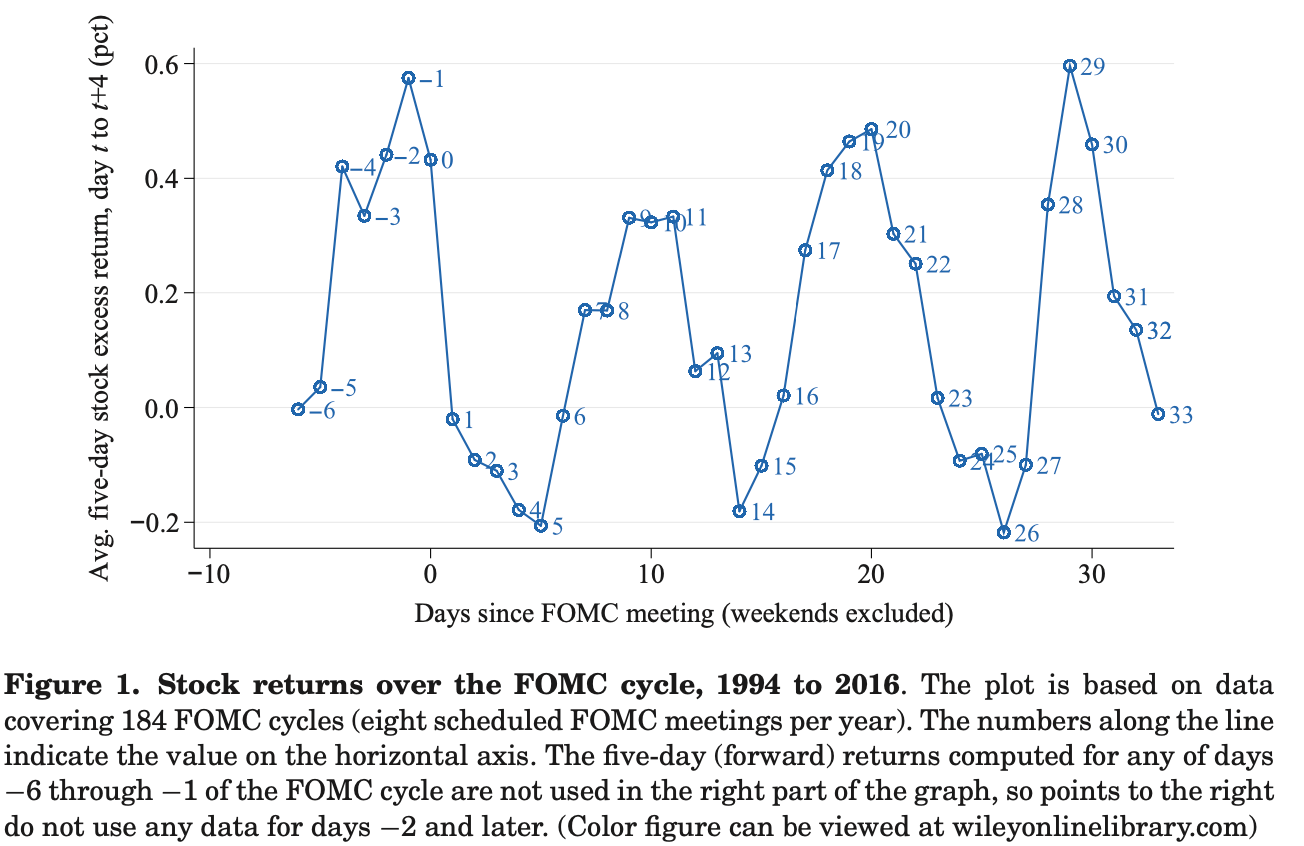

Key Table or Figure from the Paper

📌 Explanation:

- Plots 5-day rolling excess returns relative to the FOMC meeting.

- Sharp peaks occur in weeks 0, 2, 4, and 6, while returns in odd weeks are flat or negative.

- Entire equity premium is concentrated in these four weeks—a unique and replicable pattern.

Final Thought

💡 The Fed doesn’t just move markets on meeting days—it shapes the entire return cycle. 🚀

Paper Details (For Further Reading)

- Title: Stock Returns over the FOMC Cycle

- Authors: Anna Cieslak, Adair Morse, Annette Vissing-Jorgensen

- Publication Year: 2019

- Journal/Source: Journal of Finance

- Link: https://doi.org/10.1111/jofi.12818