Key Performance Metrics

📊 How Well Does This Strategy/Model Perform?

- Annualized Arbitrage Profit Potential:

- Korea vs US (Dec 2017–Jan 2018): ~$1.3B

- Japan vs US: ~$675M

- Europe vs US: ~$25M

💡 Takeaway:

During bull markets, cross-border crypto arbitrage opportunities can yield tens of millions per day due to fiat frictions and capital controls.

Key Idea: What Is This Paper About?

The paper documents large and recurrent arbitrage spreads in cryptocurrency prices across exchanges in different countries. These price gaps persist due to capital controls and fiat frictions. Crypto-to-crypto trades, however, show much tighter integration, pointing to fiat as the main bottleneck.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limits to Arbitrage (Shleifer & Vishny): Frictions like capital controls and fiat transfer delays prevent fast price equalization.

- Convenience Yield & Segmentation: Investors in countries with weak financial systems or restrictions value Bitcoin more, leading to persistent premiums.

- Order Flow Price Pressure: Net buying pushes prices higher; prices respond to demand shocks across regions.

📌 Why It Matters:

Arbitrage is not frictionless in crypto. Understanding regional demand shocks and frictions is essential to build geographic or cross-exchange trading strategies.

How to Do It: Data, Model, and Strategy Implementation

Data Used (If Applicable)

- Data Sources: Kaiko, Bitcoincharts.com, Bloomberg

- Time Period: Jan 2017 – Feb 2018

- Asset Universe: 34 exchanges across 19 countries; BTC, ETH, XRP

Model / Methodology (If Applicable)

- Arbitrage Index: Max/min price ratio across exchanges per minute

- Signed Volume Decomposition: Common vs. exchange-specific order flow

- Regression & VAR: Return predictability from volume; beta to global “buying pressure”

- Capital Control Intensity: Correlated with spread persistence

- Arbitrage Profit Estimation: Buy low / sell high with volume and spread thresholds

Trading Strategy (If Applicable)

- Execution: Simultaneously buy on low-price exchange, sell on high

- Hedging: Requires shorting (rare in Asia), holding BTC across venues, or hedging via futures

- Constraints: Capital controls, slow fiat transfer, KYC, short-sale restrictions, governance risk

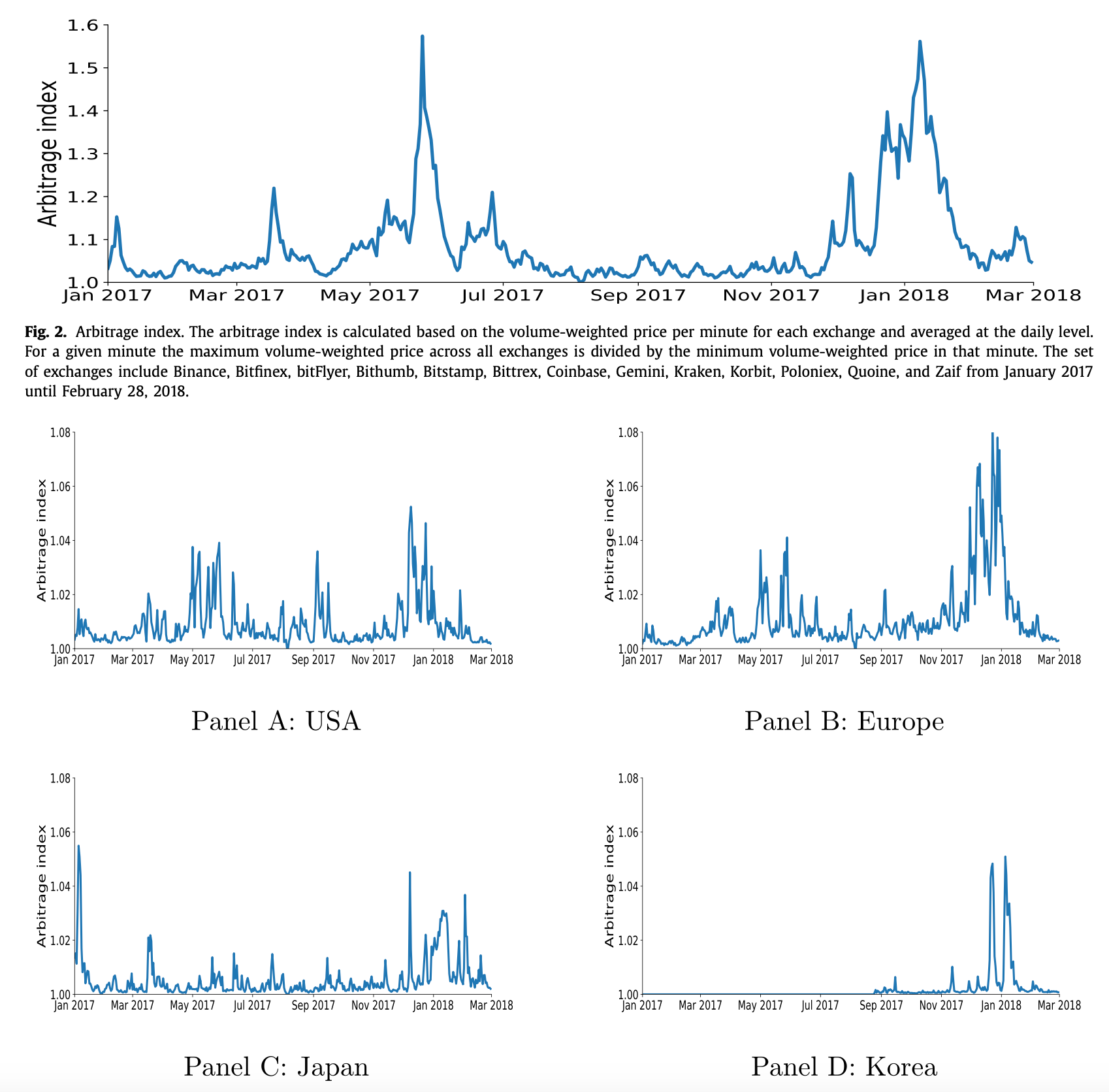

Key Table or Figure from the Paper

📊 Reference: [Figure 2] – Arbitrage Index

📌 Explanation:

- Shows the daily arbitrage index (max/min price across exchanges).

- During 2017–2018, the index spikes to 1.5+ in May, June, and Dec–Jan, meaning 50% price gaps across regions.

- Confirms persistent and systemic inefficiencies in cross-border BTC pricing.

Final Thought

💡 Crypto is globally liquid, but fiat frictions and capital controls break price parity. 🚀

Paper Details (For Further Reading)

- Title: Trading and Arbitrage in Cryptocurrency Markets

- Authors: Igor Makarov, Antoinette Schoar

- Publication Year: 2020

- Journal/Source: Journal of Financial Economics

- Link: https://doi.org/10.1016/j.jfineco.2019.07.001