💡 Takeaway:

Standard sentiment signals are enhanced by measuring how unusual the news is. Rare but impactful language combined with negative tone forecasts sustained increases in volatility.

Key Idea: What Is This Paper About?

This paper introduces a novel method for quantifying the “unusualness” of financial news using entropy (from NLP) and shows that unusual negative news strongly forecasts future volatility. The key insight is that rare negative news is not only more informative—but also processed more slowly, especially at the macro level. This delay creates persistent volatility forecasting opportunities.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limited Attention: Investors can't process all news, especially macro-level news with rare phrasing.

- Rational Inattention Models: Information-processing constraints create delayed reactions.

- Samuelson's Dictum: Markets are more efficient at processing micro (firm-level) than macro news.

- Risk Aversion and Uncertainty: Investors demand a higher risk premium amid rare negative news.

📌 Why It Matters:

Unlike return predictability (which dissipates quickly), volatility reacts slowly and persistently to surprising news. This opens a multi-month volatility trading window.

Data, Model, and Strategy Implementation

Data Used

- Time Period: 1996–2014

- News: 367,000 Reuters articles tagged to top 50 global financial firms

- Market Data: CRSP (returns), Bloomberg (IV, RV, VIX), Reuters (news tagging)

- Coverage: Firm-level and aggregate S&P 500 (VIX, SPX RVOL)

Model / Methodology

- News Processing:

- Use 4-gram entropy to measure unusualness

- Classify n-grams as positive/negative via Loughran-McDonald dictionary

- Interaction:

ENT SENT NEG = ENT NEG × SENT NEG

- Volatility Forecasting Panel Regressions:

- Dependent variables: Implied volatility (IVOL), Realized volatility (RVOL)

- Controls: Lagged IVOL, RVOL, negative returns

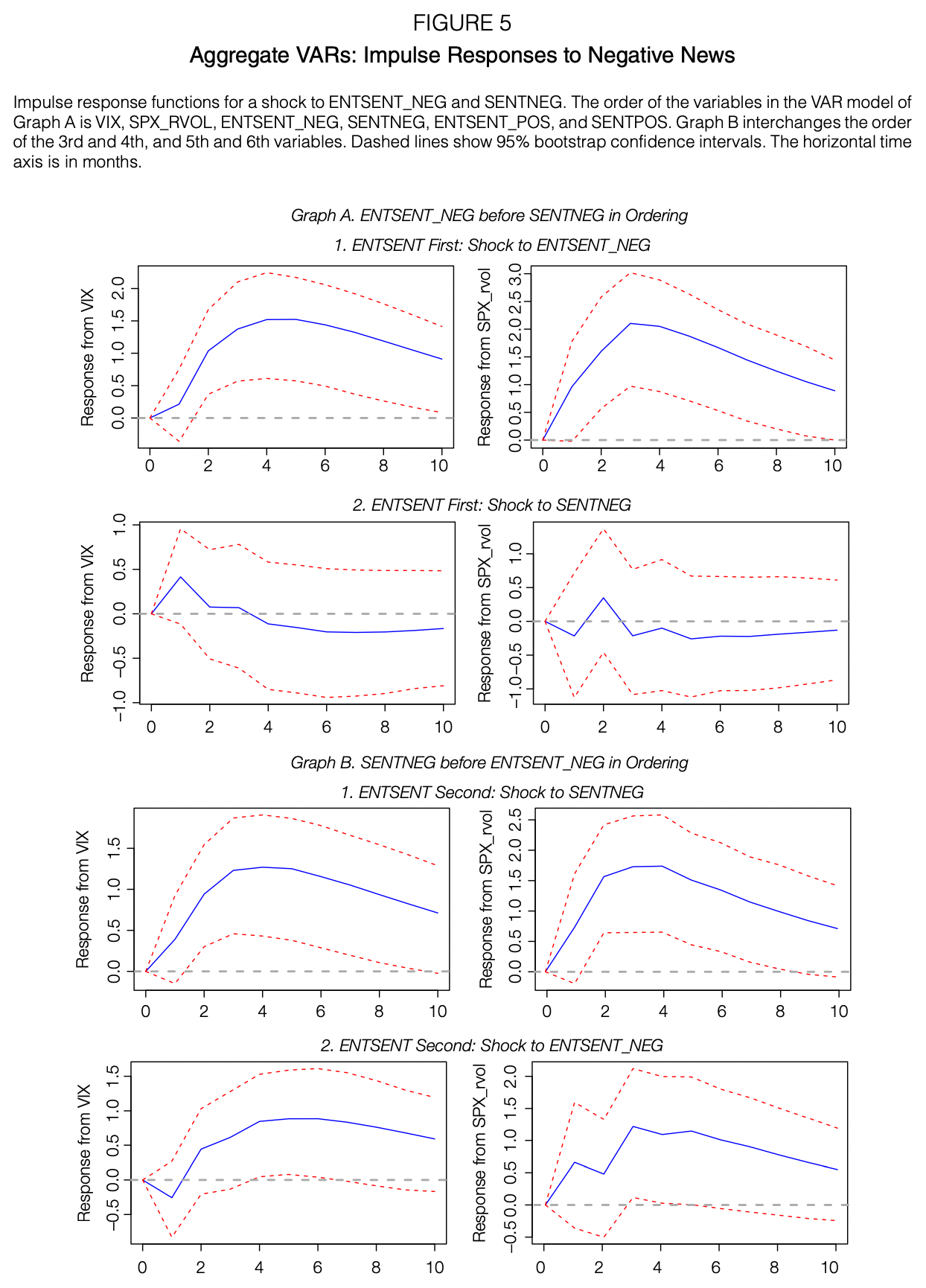

- Macro VAR (VIX/SPX RVOL):

- Impulse response analysis

- Horizon: 10 months

- Variables: VIX, SPX RVOL, ENT SENT NEG/POS, SENT NEG/POS

Trading Strategy (Volatility Forecasting)

- Signal Generation:

- Identify spikes in

ENT SENT NEGorENT SENT POSat firm or macro level

- Identify spikes in

- Execution (Ideas):

- Long VIX or variance swaps on macro signal

- Long single-name puts or straddles on firm-specific signal

- Fade volatility decay post-peak (timing based on response curves)

- Risk Management:

- Roll hedge monthly

- Avoid shorting vol until after hump-shaped response subsides

Key Table or Figure from the Paper

📌 Explanation:

- A shock to

ENT SENT NEGincreases both VIX and SPX RVOL for up to 10 months - Peak response at month 4

- Confirms slow absorption of surprising negative macro news

- Interaction term (ENT × SENT) performs better than sentiment alone

Final Thought

💡 When rare bad news hits, volatility doesn’t spike instantly—it simmers for months. 🚀

Paper Details (For Further Reading)

- Title: Does Unusual News Forecast Market Stress?

- Authors: Paul Glasserman, Harry Mamaysky

- Publication Year: 2019

- Journal/Source: Journal of Financial Economics

- Link: https://doi.org/10.1017/S0022109019000127