During the Flash Crash:

- HFTs accounted for ~29% of trading volume

- HFTs liquidated 2,000 contracts aggressively as the market fell

- Inventories stayed within tight limits (never exceeded 4,000 contracts)

💡 Takeaway:

HFTs remained active and quick but didn’t provide meaningful liquidity when markets needed it most. Their behavior was consistent with latency arbitrage, not stabilizing intermediation.

Key Idea: What Is This Paper About?

The paper investigates how HFTs and Market Makers traded during the Flash Crash. While both groups acted as intermediaries in normal times, HFTs continued their pattern of fast, inventory-light trading even during the crash. Instead of absorbing sell pressure, they turned over inventory quickly and even amplified the decline by aggressively selling during the drop.

Economic Rationale: Why Should This Work?

📌 Relevant Economic Theories and Justifications:

- Limited Risk-Bearing Capacity: Market participants can’t—or won’t—absorb large, sudden shocks unless prices adjust sharply.

- Latency Arbitrage and Quote Sniping: Fast traders profit by hitting stale quotes before others can adjust.

- Intermediation Without Obligation: HFTs are not designated market makers; they can withdraw at will, especially under stress.

📌 Why It Matters:

Understanding who really provides liquidity in stress events is critical. HFTs may improve day-to-day liquidity, but they’re unreliable in a crash. This has regulatory and design implications for automated markets.

How to Do It: Data, Model, and Strategy Implementation

Data Used

- Market: E-mini S&P 500 futures

- Date Range: May 3–6, 2010

- Source: CME audit trail transaction-level data

- Granularity: Account-level, second-by-second transactions

Model / Methodology

- Trader Classification:

- 16 top-volume traders labeled as High-Frequency Traders

- Others labeled Market Makers, Fundamental Traders, Opportunistic, and Small Traders

- Metrics:

- Inventory changes vs. price changes

- Aggressiveness ratios (passive vs. aggressive orders)

- Response time around price changes

Insights for Strategy or Market Design

- For Risk Control:

- Use real-time inventory and price response measures to detect fragile liquidity.

- For Strategy Building:

- HFTs engage in predictable inventory reversal behavior

- Quote-sniping behavior occurs just before price changes—this can be detected and modeled

- For Regulators/Exchanges:

- Relying on HFTs for crisis-time liquidity is risky

- Consider mechanisms that ensure liquidity obligations in extreme events (e.g., batch auctions, circuit breakers)

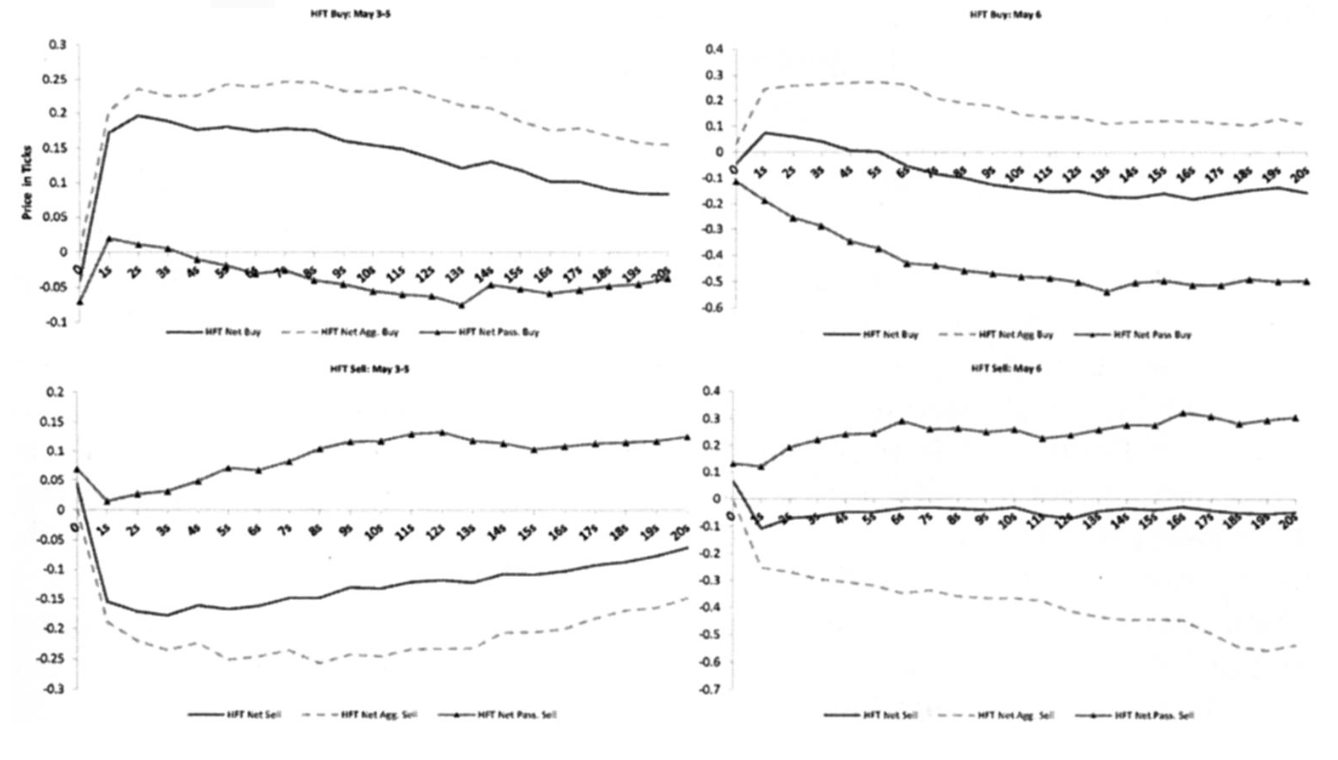

Key Table or Figure from the Paper

📌 Explanation:

- After HFTs buy, prices tend to rise in the next few seconds—supporting the idea they trade ahead of moves (not against them).

- Their passive trades have little impact, while aggressive trades align with short-term price momentum.

- Confirms quote-sniping behavior: HFTs profit by being the first to lift stale orders.

Final Thought

💡 HFTs didn’t cause the Flash Crash—but they sure didn’t stop it either. 🚀

Paper Details (For Further Reading)

- Title: The Flash Crash: High-Frequency Trading in an Electronic Market

- Authors: Andrei Kirilenko, Albert S. Kyle, Mehrdad Samadi, Tugkan Tuzun

- Publication Year: 2017

- Journal/Source: The Journal of Finance

- Link: https://www.jstor.org/stable/26652722